The Social Security System (SSS) has recently issued Circular 2021-005 to clarify the meaning and coverage of earnings declared of self-employed members in accordance with the implementation and intent of Section 19-A of the Social Security Act of 2018, otherwise known as Republic Act 11199.

Earnings declared shall mean the monthly compensation of self-employed members. On the other hand, monthly compensation is the actual remuneration for employment, including the mandated cost-of-living allowance and the cash value of any remuneration paid in any medium other than cash, except that part of remuneration received during the month in excess of the maximum salary credit. The amount determined as earnings declared will be used as the basis in computing monthly SSS contributions.

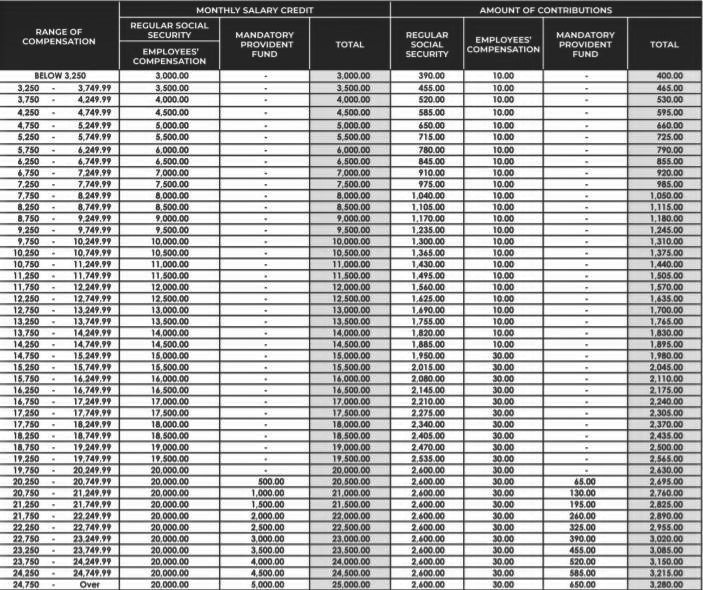

To illustrate, if a self-employed member is receiving a monthly income of P30,000, such amount is compared to the maximum salary credit under SSS rules, which is P25,000. The excess of P5,000 will not be included in determining the earnings declared. This means that the maximum salary credit of P25,000 will be used as the basis in computing the monthly SSS contributions.

The schedule of contributions for all self-employed members effective January 2021 is shown as follows:

![]()

Please be guided accordingly.

Source:

P&A Grant Thornton

Certified Public Accountants

As published in SunStar Cebu, dated 19 May 2021