Clarifications on submission of BIR Form 1709 (RPT Form)

05 May 2021In its Revenue Memorandum Circular (RMC) 54-2021 released on April 27, 2021, the Bureau of Internal Revenue (BIR) clarified the rules on the submission of BIR Form 1709 or the Related Party Transactions (RPT) Form pursuant to the provisions of RR 19-2020, as amended by RR 34-2020. Among the highlights in the said RMC are the following:

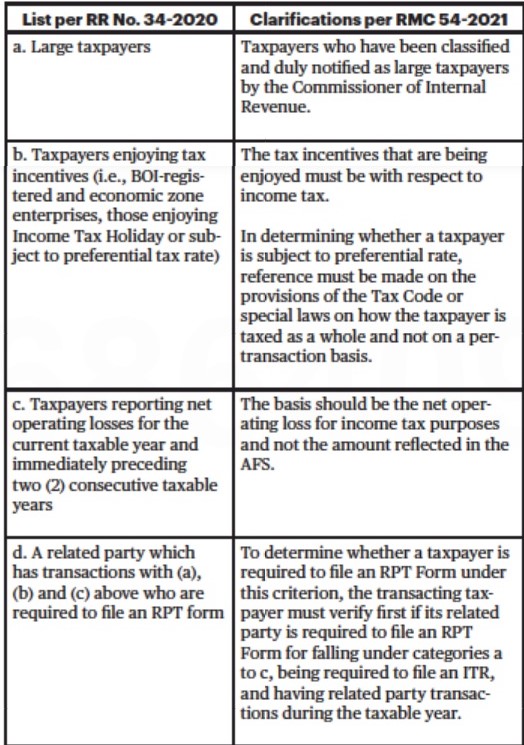

The taxpayers mandated to submit BIR Form 1709 are those required to file Annual Income Tax Returns (AITR) and those who have transactions with domestic or foreign related parties during the concerned taxable period. In addition, these taxpayers must also fall under any of these conditions:

The BIR also made it clear that all related party transactions must be disclosed irrespective of the amounts. Actual amounts and not estimates of the related party transactions shall be declared in the RPT Form.

Moreover, if several currencies were used for related party transactions, and it seems impractical to indicate all of them in the RPT Form, their equivalent in the local currency should instead be disclosed. However, the exchange rates to be used should be the rate at the transaction date in all cases.

Lastly, if the taxpayer fails to provide any material information (e.g. details of the related parties and related party transactions etc.), the RPT Form will be disregarded, and the penalty for failure to file such information return will be imposed.

Source:

P&A Grant Thornton

As published in SunStar Cebu, dated 05 May 2021