The Bureau of Internal Revenue (BIR) recently issued Revenue Memorandum Circular No. 107-2021 on October 18, 2021 providing taxation guidelines on the imposition of taxes on POGOs pursuant to Republic Act (RA) No. 11590 entitled “An Act Taxing Philippine Offshore Gaming Operations.”

Offshore gaming licensee refers to an offshore gaming operator, whether organized abroad or in the Philippines, duly licensed and authorized, through a gaming license, by the Philippine Amusement and Gaming Corporation (PAGCOR), any special economic zone authority, tourism zone authority, or freeport authority to conduct offshore gaming operations, including the acceptance of bets from offshore customers, as provided for in their respective charters.

Whereas a service provider is any juridical person, duly created or organized within or outside the Philippines, or a natural person, regardless of citizenship or residence, which provides ancillary services to an offshore gaming licensee, or any gaming licensee, or operator with licenses from other jurisdictions. These ancillary services may include customer and technical relations and support, information technology, gaming software, data provision, payment solutions, and live studio and streaming services.

All offshore gaming licensees and service providers shall submit to the BIR original copies of notarized contracts of employment clearly stating the annual salary and other benefits and entitlements of concerned aliens. In addition, all foreign employees of offshore gaming licensees and their service providers, regardless of nature of employment, shall have a Tax Identification Number (TIN). Failure to procure this will subject the POGOs to a fine for every foreign national without such TIN and, in proper instances, revocation of their primary and other licenses obtained from government agencies and prohibition in employing foreign nationals for their operations.

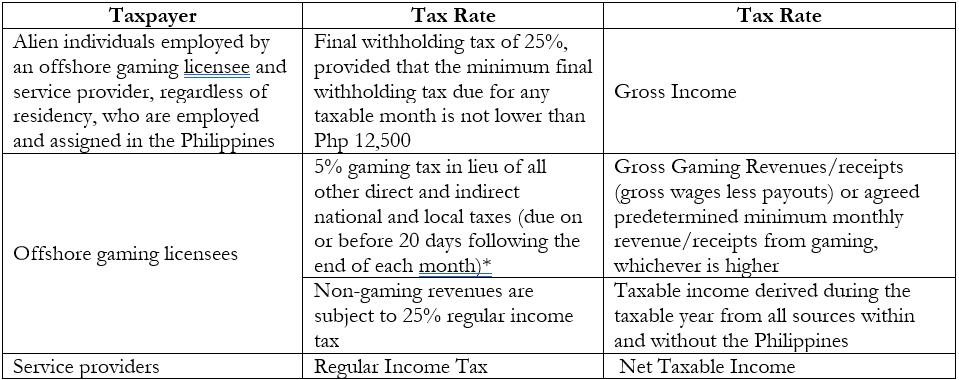

The table below summarizes the different tax treatments for various affected taxpayers:

![]()

* PAGCOR or any special economic zone, tourism, or freeport authority may also impose regulatory fees not exceeding 2%

Please be guided accordingly.

Source:

P&A Grant Thornton

Certified Public Accountants

As published in SunStar Cebu, dated 03 November 2021