Last Sept. 22, 2021, President Rodrigo Duterte signed into law Republic Act (RA) 11590 or an “Act Taxing Philippine Offshore Gaming Operations (POGO),” which amends certain provisions in the National Internal Revenue Code to clarify taxes imposed on POGOs. This will provide clearer taxation guidelines and will strengthen the power of the Bureau of Internal Revenue (BIR) to collect taxes from POGOs.

Offshore gaming licensee, as defined by law, refers to an offshore gaming operator, whether organized abroad or in the Philippines, duly licensed and authorized, through a gaming license, by the Philippine Amusement and Gaming Corp. (PAGCOR) or any special economic zone authority, tourism zone authority, or freeport authority to conduct offshore gaming operations, including the acceptance of bets from offshore customers.

Whereas a service provider is any juridical person, duly created or organized within or outside the Philippines, or a natural person, regardless of citizenship or residence, which provides ancillary services to an offshore gaming licensee, or any gaming licensee or operator with licenses from other jurisdictions. These ancillary services may include customer and technical relations and support, information technology, gaming software, data provision, payment solutions, and live studio and streaming services.

All foreign employees of offshore gaming licensees shall have a Tax Identification Number (TIN). If caught violating this provision, they are liable for penalties of P20,000 for every foreign national without a TIN. In proper instances, revocation of licenses obtained from government agencies and prohibition from employing foreign nationals for their operations may also be imposed.

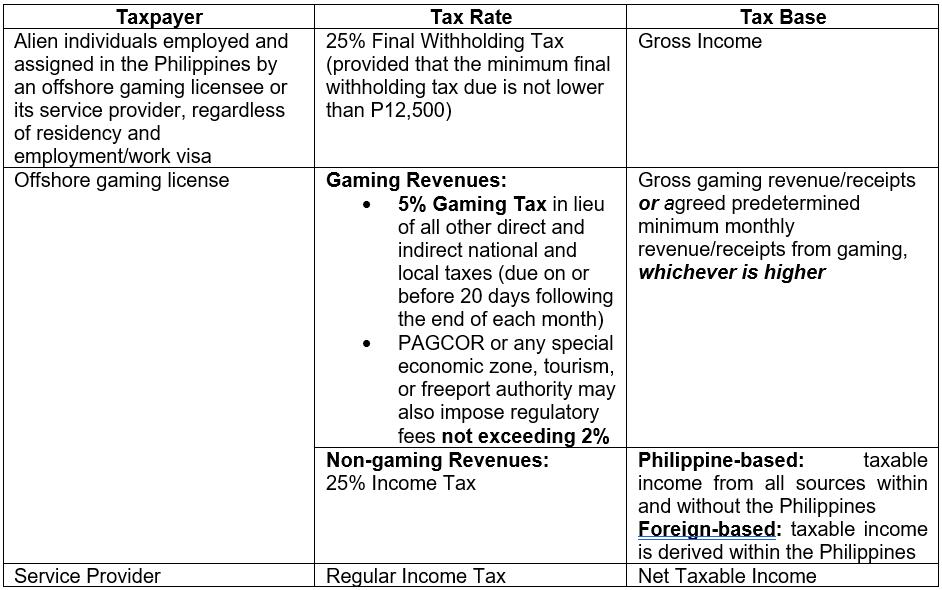

Summarized below are the tax treatments of various taxpayers affected:

![]()

The following transactions are subject to zero percent VAT:

- Sales of goods and properties to offshore gaming licensees subject to gaming tax

- Services rendered to offshore gaming licensees subject to gaming tax by service providers, including accredited service providers

The PAGCOR or other implementing agency shall engage the services of a third-party audit platform to determine the gross gaming revenues/receipts of each offshore gaming licensee for submission to the BIR.

Source:

P&A Grant Thornton

Certified Public Accountants

As published in SunStar Cebu, dated 13 October 2021