In its Revenue Memorandum Circular 94-2021, dated July 21, 2021, the Bureau of Internal Revenue clarified the proper computation of Donor’s Tax in case there is a partial renunciation of inheritance. This happens when an heir waives his/her share in an identified property but not to the entire set of properties of the decedent. Such scenario will result to an unequal share of heirs in the decedent’s property. Hence, donor’s tax should be computed based on the value of the share the heir has foregone in favor of other heirs.

Illustration:

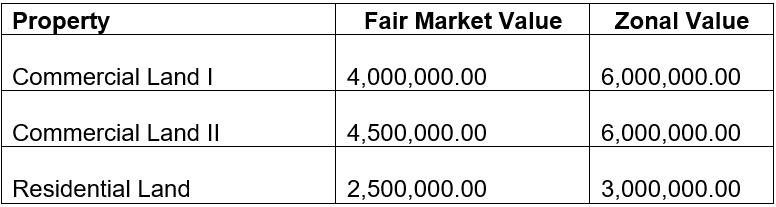

Decedent P left the following properties with its Fair Market and Zonal Value as follows:

![]()

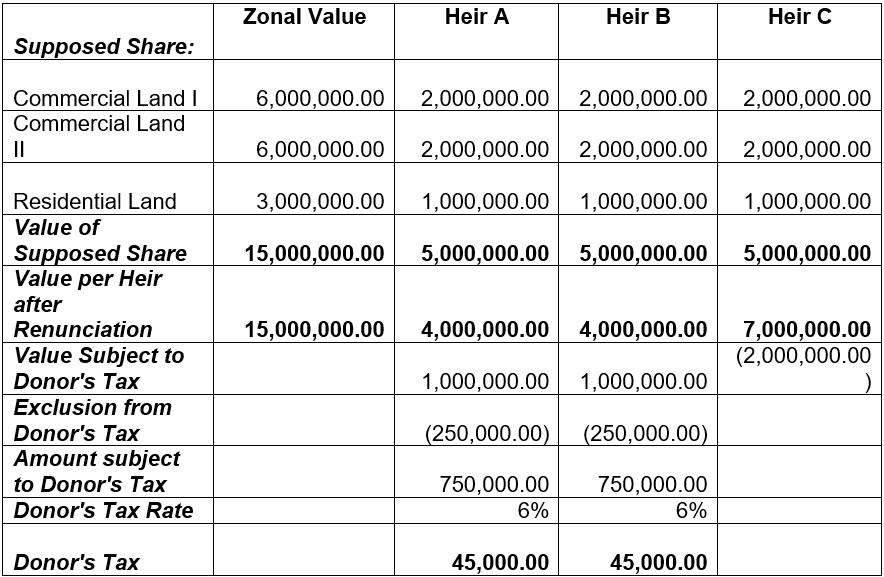

Heir A, B, and C executed an Extrajudicial Settlement stating that A and B will forego their respective shares on the residential land.

Please see computation below:

![]()

The above computation should be applied consistently throughout all offices processing one-time transactions involving the decedent’s estate.

Source:

P&A Grant Thornton

Certified Public Accountants

P&A Grant Thornton is the Philippine member firm of Grant Thornton International Ltd.

As published in SunStar Cebu, dated 07 October 2021