Corporations and individual taxpayers engaged in business or practice of profession who sustained losses wrought by the recent monsoon rains may claim the loss as deduction for the taxable year in which the loss was sustained.

In claiming the deduction for losses, the affected taxpayer must comply with the following requirements imposed under existing regulations.

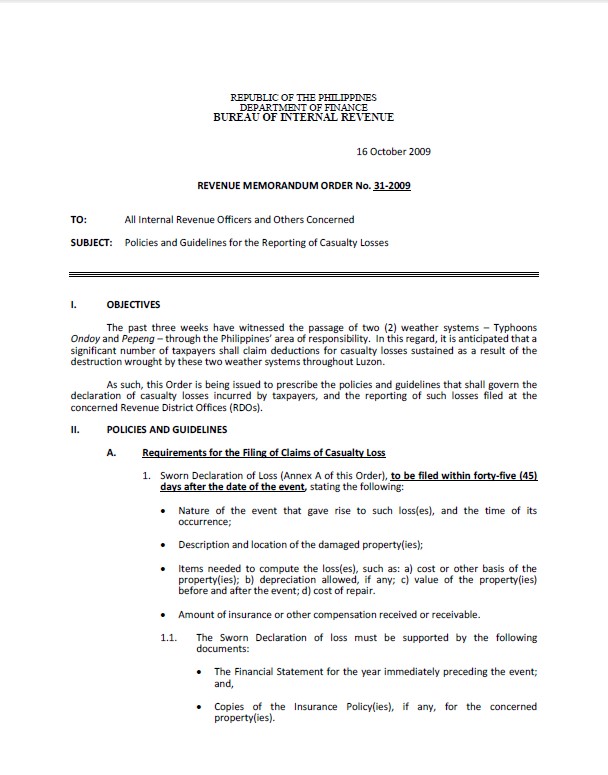

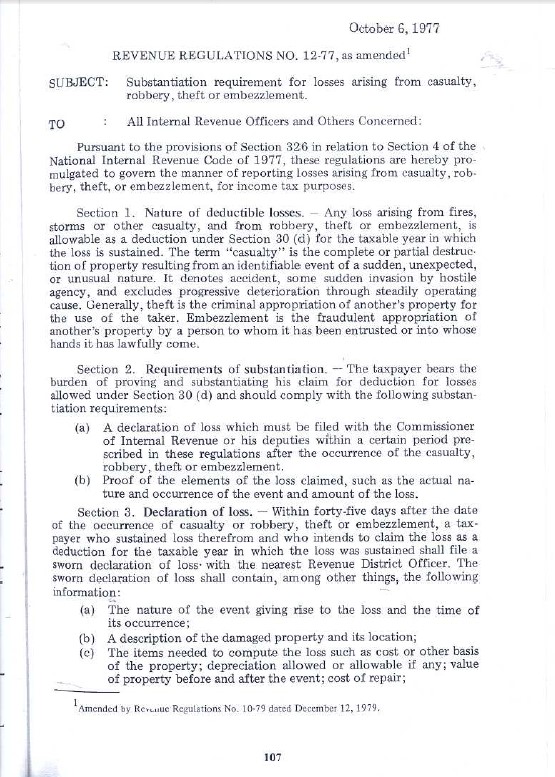

A. Declaration of loss. Taxpayers who intend to claim their losses as a deduction should file within 45 days after the event, a sworn declaration of loss with the Revenue District Officer (RDO) which has jurisdiction over the taxpayer’s place of business. The sworn declaration of loss shall contain, among other things, the following information:

1. Nature of the event that gave rise to the loss and time of its occurrence

2. Description and location of the damaged properties.

3. Items needed to compute the losses such as: (a) cost or other basis of the properties; (b) depreciation, if any; (c) value of the properties before and after the event; and (d) cost of repair; and

4. Amount of insurance or other compensation received or receivable.

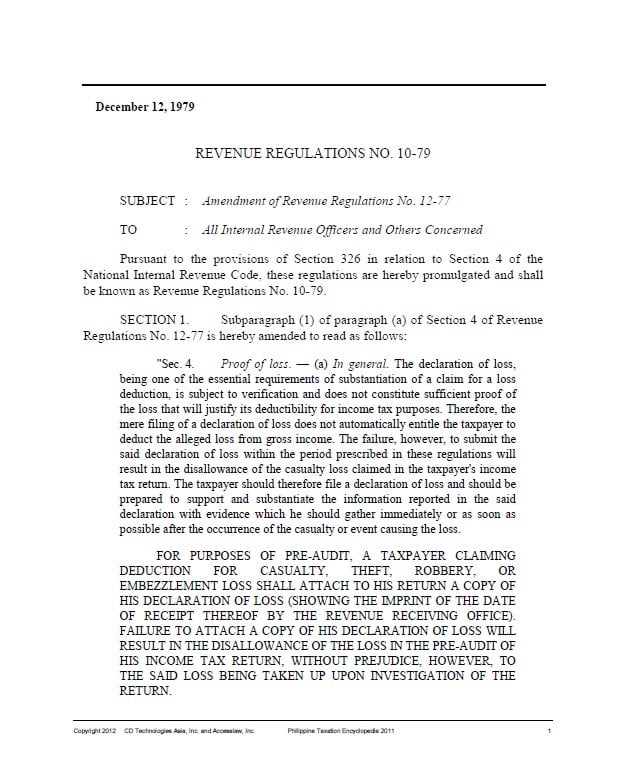

B. Proof of loss. The declaration of loss should be substantiated with evidence which the taxpayer should gather immediately after the occurrence of the casualty or event causing the loss. These include the following documents which should be kept by the taxpayer for BIR verification.

1. Photographs of the property taken before and after the monsoon rains showing the extent of the damage sustained.

2. Documentary evidence for determining the cost of valuation of the damaged properties such as purchase contracts and deeds, receipt bills for improvements, competent appraisals of the property before and after the casualty, cancelled checks, vouchers, receipts and other evidence of cost.

3. Insurance policy for insured properties.

4. Police report, in case of robbery/theft during the typhoon and/or as a consequence of looting.

For purposes of pre-audit, the taxpayer claiming the loss shall attach to his return a copy of his declaration of loss (showing the imprint of the date of receipt by the receiving office. Failure to attach a copy of his declaration of loss will result in the disallowance of loss in the pre-audit of his income tax return.

C. Conditions for deductibility of losses

1. Taxpayer must be engaged in trade or business.

2. The properties must be actually used in the business and are reported in the appropriate declaration filed with the BIR.

3. Damaged properties should be properly reported as part of the assets in the accounting records and financial statements in the year immediately preceding the loss, with the cost of acquisition clearly established and recorded.

4. Amount of loss compensated by insurance cannot be claimed as a deductible loss. Recovery of casualty through insurance claims shall be governed by RR 12-77.

5. The deduction of assets as capital losses must be properly recorded in the accounting reports.

Please see attached copy of existing regulations on losses (Revenue Regulations No. 12-77 as amended by RR 10-79 and Revenue Memorandum Order No. 31-09).