Accounting and taxation of short-term leases and lease for low-value assets

Nikkolai F. Canceran

29 Oct 2019

Nikkolai F. Canceran

29 Oct 2019

Philippine Financial Reporting Standard (PFRS) 16 is the new accounting standard for lease of assets or arrangements that contain a lease. It became effective on Jan. 1. It replaces Philippine Accounting Standard (PAS) 17, which means that entities reporting under PFRS shall apply this new standard in their lease transactions starting on the effectivity date.

On the other hand, taxation for leases generally remains unchanged since the issuance of Revenue Regulations (RR) No. 19-86 on Jan. 1, 1987 which prescribes the rules to govern the tax treatment of lease agreements.

As we all know, accounting standards and tax rules differ in many instances, and PFRS 16 is no exception. The purpose of this article is to provide a useful reference for taxpayers in knowing and dealing with the differences of accounting and tax rules for leases.

SHORT-TERM LEASE AND LEASE FOR LOW VALUE ASSETS

PFRS 16 defines short-term lease as a lease with a lease term of 12 months or less but taking into consideration the renewal options. On the other hand, lease for low-value assets is a lease for which the underlying asset is of low value (i.e., $5,000 or equivalent for a new similar asset).

ACCOUNTING TREATMENT FOR LESSEE AND LESSOR

Leases of these kind are accounted for in a way that is similar to current operating lease accounting — which means that payments are recognized by the lessee as an expense or cost and revenue by the lessor on a straight-line basis or another systematic basis that is more representative of the pattern of the benefits. Simply put, lease expense or revenue is generally reported equally over the lease term. However, for short-term lease, the lessee has the option to recognize right-of-use asset (ROUA) and a corresponding lease liability instead of the straight-line basis. The discussion on accounting and tax treatment for ROUA and lease liability will be tackled in part 2 of this article.

When the lessee pays advance rental and security deposit, the lessee shall account these as asset at the time of payment. These shall be reported as lease expense/cost in the period when applied to lease. On the part of the lessor, the advance/prepaid rental and security deposit shall be recorded as liability in the period of receipt and shall be reported as lease income in the period when applied to lease.

TAX RULES

RR No. 19-86 defines a lease as an agreement between a lessor and a lessee giving the lessee possession and use of a specific property upon payment of rentals over a period of time (which may be definite or indefinite). The equivalent of short-term lease or lease for low value assets for tax purposes is an operating lease.

Operating lease is defined in RR No. 19-86 as a contract under which the asset is not wholly amortized during the primary period of the lease, and where the lessor does not rely solely on the rentals during the primary period for his profits but looks for the recovery of the balance of his costs and for the rest of his profits from the sale or re-lease of the returned asset of the primary lease period.

LESSEE TAXATION

In an operating lease, the lessee may deduct the amount of rental actually due under the lease agreement during the year. This is subject to 5% expanded withholding tax (EWT).

In addition to the rent actually paid or payable to the lessor, the lessee should also report all the expenses/costs which under the terms of the agreement the lessee is required to pay or for the account of the lessor, as additional rental expense/cost which is also subject to 5% EWT. An example is the real property tax on the leased property if paid by the lessee should be claimed by the lessee as rental expense/cost and not as tax expense.

In case the lessee pays advance/prepaid rentals, if the lessee adopts the accrual basis of accounting, according to tax rules, the lessee should treat the advance/prepaid rentals as an asset subject to 5% EWT at the time of payment. These shall be claimed as deductible at the time of its application to the lease.

If the lessee, on the other hand, adopts the cash basis of accounting, the advance/prepaid rentals are deductible items at the time of payment provided the advance/prepaid rentals do not extend beyond 12 months. Otherwise, advance rentals/prepaid rentals corresponding to the period beyond 12 months shall be accounted for as an asset and will be claimed as deductible items at the time of its application to the lease. For withholding tax purposes, the entire advance/prepaid rentals including those for the period beyond 12 months shall be subject to 5% EWT at the time of payment.

With respect to security deposit for the faithful performance of certain obligations of the lessee, the lessee, whether adopting accrual or cash basis of accounting, should treat the same as an asset and not subject to 5% EWT at the time of payment because of its being in the nature of a conditional deposit. These deposits shall be claimed deductions subject to 5% EWT at the time of its application to the lease.

LESSOR TAXATION

Generally, the taxation of the lessor in operating lease is similar to that of the lessee but with opposite effects.

The lessor should report as taxable income only the rental payments that it is entitled to receive for the year, as provided under the lease agreement. For VAT purposes, the lessor shall report the lease income based on gross receipts or on collection basis.

Costs/expenses related to the leased property that are the responsibility of the lessor, if paid by the lessee, are deemed additional rental income of the lessor which is also subject to VAT (e.g., real property taxed on leased property that are paid by the lessee is reported as part of the lessor’s taxable rental income).

For advance/prepaid rentals, lessor taxation is different from the lessee because these are reported as taxable income of the lessor and also for VAT purposes in the year when received whether the lessor is using the accrual or the cash method of accounting.

Security deposit when received by the lessor, whether the lessor is using the accrual or the cash method of accounting, should be treated as a liability at the time of receipt and will be recognized as income which is subject to VAT at the time of application to lease.

DEALING WITH THE DIFFERENCES

For accounting purposes, the lease income/expense will be averaged on a straight-line basis over the lease term such that the monthly or annual lease income/expense is the same for the entire period of the lease including the rent-free period. For tax purposes, the actual lease income/expense for each period indicated in the lease contract should be reported as lease income/expense for that period. The difference between accounting and tax usually happens when there is escalation of the lease amount over the lease term or when a rent-free period is present.

The monthly/annual difference of lease income/expense shall be accounted for by the lessee and lessor as a temporary difference with the recognition of either deferred tax asset or liability as the case maybe. The reason why the difference is just temporary is that at the end of the lease term the total lease income/expense is equal under accounting and tax purposes.

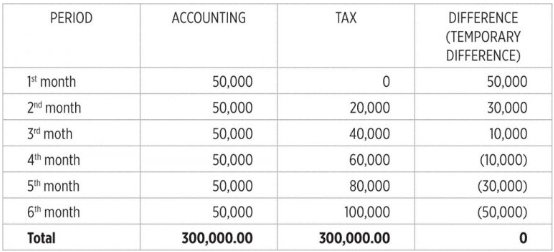

To illustrate, say for example the lease agreement states that the lease term is for six months, the first month of the term is free, the second month’s lease is P20,000 and shall increase by P20,000 every month.

Shown in the table below the monthly lease income/expense for accounting and tax purposes.

The difference in lease income/expense should be reported in the schedule of reconciliation of net income per accounting books against taxable income of the income tax return.

In the same vein, the difference in the accounting and tax treatment of advance/prepaid rentals for both lessee and lessor is considered a temporary difference with the recognition of either deferred tax asset of liability as the case maybe and the difference shall be reported in the reconciliation schedule of the income tax return.

The study of difference on lease contracts other than short-term leases and low value asset particularly the accounting of ROUA and lease liability and its equivalent tax treatment will be discussed in part 2 of this article next week.

Let’s Talk Tax is a weekly newspaper column of P&A Grant Thornton that aims to keep the public informed of various developments in taxation. This article is not intended to be a substitute for competent professional advice.

Nikkolai F. Canceran is a director from the Tax Advisory & Compliance division of P&A Grant Thornton, the Philippine member firm of Grant Thornton International Ltd.

As published in BusinessWorld, dated 29 October 2019