Filing final tax and percentage tax returns

23 Jan 2018

AMONG the changes brought about by the implementation of Republic Act No. 10963 or the TRAIN Law are the revised tax rates for final tax and percentage tax. However, the tax returns/forms for these taxes have not yet been updated and reflected in the electronic Filing and Payment System (eFPS) and electronic BIR (eBIR) forms. Pending the revision or enhancement of the returns/forms, the Bureau of Internal Revenue (BIR) issued Revenue Memorandum Circular (RMC) No. 2-2018 on Jan. 8.

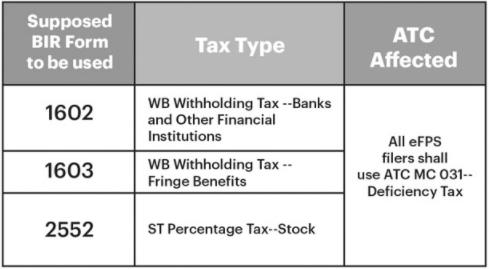

The issuance provides the transition procedures for filing the monthly remittance return of final income taxes withheld (BIR Form 1602), quarterly remittance return of final income taxes withheld (BIR Form 1603), and percentage tax return for transactions involving shares of stocks listed and traded through the local stock exchange or through initial and/or secondary public offering (BIR Form 2552). The workaround procedures are as follows:

eFPS filers must:

File online using the existing BIR Form in the EFPS, and then pay online the corresponding taxes due thereon by proceeding to payment. The result of this transaction is a deficiency tax;

To cover the deficiency tax, eFPS filers must likewise file and pay online the deficiency tax using BIR Form No. 0605 and fill in the corresponding information in the tax type and ATC fields stated below, in lieu of the correct BIR form that should have been used.

Once the enhanced versions of the forms are available in eFPS, there will be a notification/announcement through an RMC. Guidelines will be issued if there is a need to amend the previously filed returns in eFPS.

eBIR forms users/filers must:

File online using the existing BIR form in the eBIR Forms Package, and then pay the corresponding taxes due thereon via:

Online payment through GCash, Landbank Electronic Payment Service (LBEPS), or BIR-Development Bank of the Philippines PayTax Online (BDPTO); or

Manual payment via over-the-counter (OTC) of authorized agent banks (AABs) under the jurisdiction of the revenue district office (RDO) where the taxpayer is registered.

The transactions above will result in deficiency tax and, to cover the deficiency tax, eBIR Forms users/filers must file online and pay online, through GCash, LBEPS, or BDPTO, or pay manually via OTC of AABs under the jurisdiction of the RDO where the taxpayer is registered, the deficiency tax using BIR Form No. 0605, and fill in the corresponding information in the Tax Type and ATC fields shown in the previous table, in lieu of the correct BIR form that should have been used.

Manual filers must:

Fill out the applicable BIR Form, preprinted or downloaded from the BIR website, using the new tax rates, and then compute the tax due.

File and pay manually via OTC of AABs under the jurisdiction of the RDO where the taxpayer is registered.

Please be guided accordingly.

Source: P&A GRANT THORNTON

Certified Public Accountants

As published in SunStar Cebu dated 23 January 2018.