Reiteration of the alternative modes of issuance of receipts/invoices during modified en.....

07 Oct 2020

THE Bureau of Internal Revenue (BIR) has recently issued Revenue Memorandum Circular (RMC) 96-2020 to reiterate the alternative modes of issuance of receipts/invoices applicable during the period of modified enhanced community quarantine (MECQ).

Under RMC 47-2020, as amended by RMC 59-2020, taxpayers located in areas covered under MECQ are allowed to adopt workaround procedures on the issuance of receipts/invoices to be able to continue their business operations.

In compliance with existing revenue issuances, business taxpayers must issue receipts/invoices with Authority to Print (ATP) for manually bound or loose-leaf receipts or invoices, while system generated receipts/invoices must have a duly approved Permit to Use (PTU) or acknowledgment certificate, whichever is applicable.

However, in case the duly authorized or approved receipts/invoices shall be inaccessible or unavailable due to quarantine measures, the business taxpayers may opt to use any of the following:

a. BIR printed receipts/invoices

b. Scanned copy of receipt/invoice with ATP and electronically transmitted JPEG, PDF or any equivalent format to the customer

c. Computer-aided receipt/invoice in excel format not covered by an ATP and similarly transmitted electronically in JPEG, PDF or any equivalent format to the customer

d. Supplementary receipts/invoices issued (i.e., delivery receipts, acknowledgement receipts, etc.) in lieu of the principal receipts/invoices (i.e., official receipts and sales invoice)

e. Receipt/invoice using the existing Computerized Accounting System (CAS) or its components with approved PTU or acknowledgment certificate; however, the said receipt/invoice is being sent electronically in JPEG, PDF or any equivalent format to the customer

f. Receipt/invoice generated from a newly developed receipting/invoicing software or CAS or its components without duly approved PTU or acknowledgment certificate, which was used to temporarily generate/issue the receipts/invoices and the receipt/invoice is being sent electronically in in JPEG, PDF or any equivalent format to the customer.

Once the MECQ is lifted, the taxpayer/seller must immediately provide or issue the duly authorized receipts/invoices to their clients/customers to cover all sales transactions that were issued temporary receipts/invoices during the MECQ period.

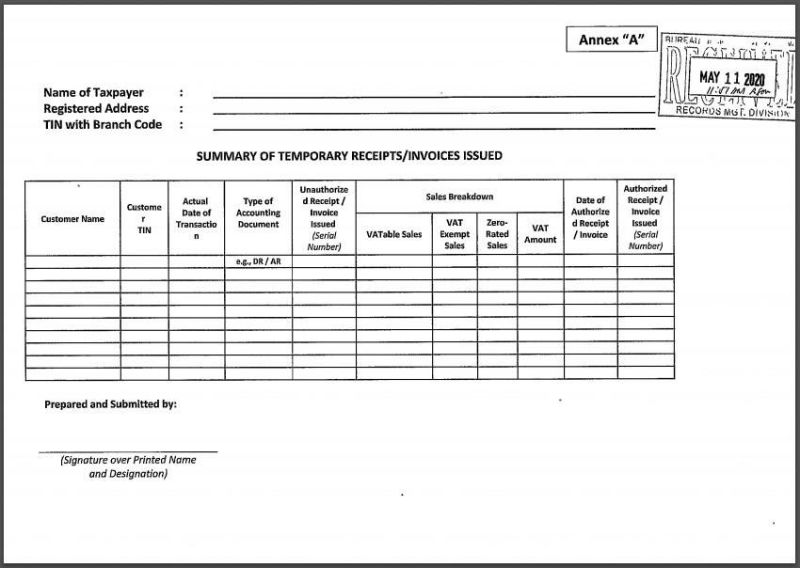

Taxpayers, who opted to adopt the workaround procedures during the period of MECQ from Aug. 4 to 18, 2020, are reminded to submit the required summary of temporary receipts/ invoices issued , following the format prescribed by Annex “A” of the RMC 47-2020 attached below, to their respective revenue district offices within 90 days from the date of the lifting of MECQ, among other requirements.

Please be guided accordingly.

Source:

P&A Grant Thornton

Certified Public Accountants

As published in SunStar Cebu, dated 07 October 2020