The Commissioner of Internal Revenue has issued Revenue Memorandum Circular (RMC) No. 21-2022 to provide guidance on the work-around procedures in claiming input VAT on purchased or imported capital goods starting January 1, 2022.

The work-around procedures and guidelines prescribed by the RMC are summarized below:

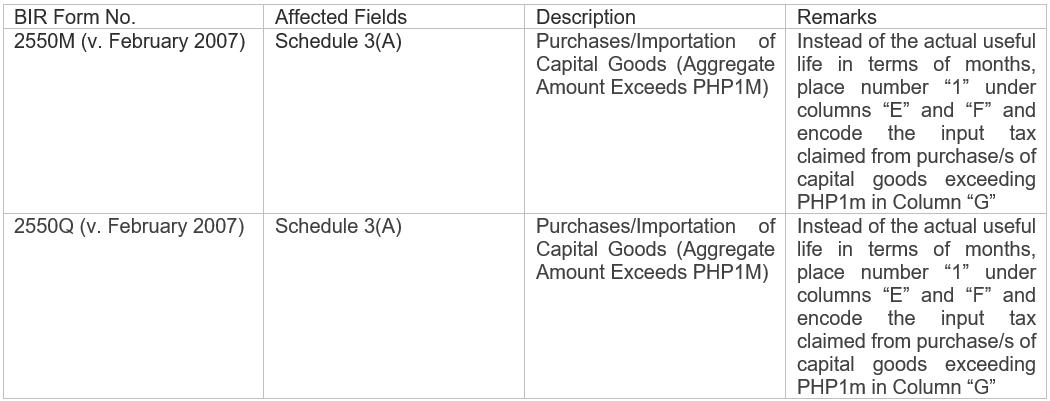

![]()

The RMC further clarified that under eFPS and eBIRForms, the balance of input tax to be carried over to a succeeding period is computed automatically by these systems. Hence, for purposes of implementing the provisions in the Tax Code of 1997, as amended, effective January 1, 2022, all input tax on purchases of capital goods shall already be allowed upon purchase/payment and shall no longer be deferred. The taxpayer shall indicate Roman numeral "1" as the estimated useful and recognized useful life and encode the total input taxes claimed from purchase/s of capital goods exceeding PIM under Column "G" in order to show a nil amount of "Balance of Input Tax to be Carried to Next Period" under Column “H" of the monthly and quarterly VAT returns.

However, for taxpayers with unutilized input VAT on capital goods purchased or imported prior to January 1, 2022, they shall be allowed to amortize the same as scheduled until fully utilized. Hence. Schedule 3(B) shall still be filled out. However, if the depreciable capital good is sold/transferred within the period of five (5) years or prior to the exhaustion of the amortizable input tax thereon, the entire unamortized input tax on the capital goods sold/transferred can be claimed as input tax credit during the month/quarter when the sale or transfer was made.

Please be guided accordingly.

Source:

P&A Grant Thornton

Certified Public Accountants

As published in SunStar Cebu, dated 14 March 2022