THE submission of a Certificate of Residence for Tax Treaty Relief (CORTT) Form for dividends, interest and royalties has been officially discontinued. In place is a set of streamlined guidelines on how to avail of the tax treaty benefit, pursuant to Revenue Memorandum Order 14-2021 and Revenue Memorandum Circular 77-2021.

Generally, a request for confirmation or tax treaty relief application shall apply to all income derived by nonresidents from Philippine sources that may be entitled to relief from double taxation under relevant tax treaties.

The following rules shall be observed:

a. A nonresident taxpayer shall submit an Application Form for Treaty Purposes (BIR Form 0901), together with a Tax Residency Certificate (TRC) or a duly issued certificate by the foreign tax authority to each withholding agent prior to the payment of income. The withholding agent may apply the provisions of the applicable treaty, provided that all the conditions for the availment thereof under the treaty have been satisfied. Otherwise, the regular rates imposed under the Tax Code should be applied by the withholding agent.

b. When the treaty rates have been applied by the withholding agent on the income earned by the nonresident, the former shall file with the International Tax Affairs Division (ITAD) a Request for Confirmation (RFC) on the propriety of the withholding tax rates applied on that item of income. On the other hand, if the regular tax rates have been imposed on the said income, the nonresident shall file a Tax Treaty Relief Application (TTRA) with ITAD. In either case, each request for confirmation and TTRA shall be supported by the documentary requirements set out hereunder.

c. If the treaty rate was applied on the non-resident’s income, the income payor, domestic or foreign, should be the one to file the request for confirmation with the ITAD. The income payor is not prevented, however, from authorizing the nonresident or any other person to file such a request for and on its behalf, provided that the latter is equipped with a special power of attorney.

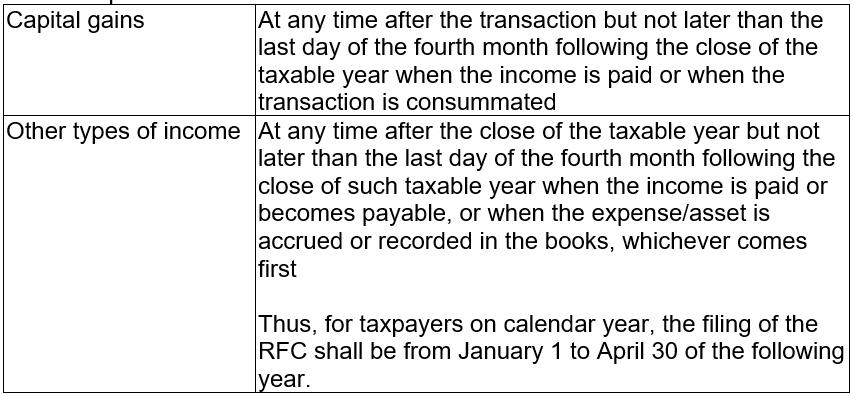

d. The RFC, with complete documentary requirements, shall be filed on or before the dates prescribed below:

![]()

e. One consolidated RFC per nonresident income recipient, regardless of the number and type of income payments made during the year, shall be filed.

f. For long-term contracts involving the payment of interests and royalties and other types of income where the condition for entitlement to treaty benefits is not dependent on time threshold, annual updating is not mandatory. However, the withholding agent should ensure that the nonresident continues to be a resident of the same country for the whole duration of the contract by requiring the nonresident an updated TRC.

g. If there would be material changes in the facts or circumstances upon which the previous ruling was based in the succeeding year, an RFC shall again be filed by the withholding agent.

h. In the case of long-term contract of services where the existence of a permanent establishment in the Philippines is dependent on time threshold, the annual updating is mandatory.

i. If the RFC or TTRA is approved, the BIR will issue a Certificate of Entitlement instead of the usual BIR Ruling. The COE will still contain the material facts of the case and a ruling confirming the non-resident’s entitlement to treaty benefit.

Furthermore, the memorandum provides that there will be no automatic denial for failure to file the RFC/TTRA within the prescribed period.

However, a penalty for late filing shall be imposed. For a nonresident who has income in 2020 wherein the prior years were subjected to treaty rates, but no TTRA or CORTT Form was filed therefore, the withholding agent has until the last working day of this year to file an RFC with complete documentary requirements. Failure to file the same within the prescribed deadline would be subject to administrative penalties under Sections 250 and 255 of the Tax Code. Moreover, a penalty of P1,000 per failure to file a CORTT Form for dividends, interests and royalties paid after the effectivity of RMO 8-2017 until Dec. 31, 2020 shall be imposed.

Lastly, all taxpayers with pending TTRAs will still receive a “Final Notice to Submit Additional Documents” and will be given three months from receipt thereof to submit the required documents. Those who have been notified that their applications have been archived will no longer receive a Final Notice but are obliged to submit the required documents indicated in the previous notice/s within four months from the effectivity of the new RMO.

Source:

P&A Grant Thornton

Certified Public Accountants

As published in SunStar Cebu, dated 16 July 2021