The Fiscal Incentives Review Board (FIRB) has issued FIRB Advisory No. 3-2023 regarding the correct basis of the penalty imposed on Registered Business Enterprises (RBEs) engaged in Information Technology and Business Process Management (IT-BPM) for non-compliance with the work-from-home (WFH) threshold.

The penalty should be based on 100% or the whole amount of Regular Corporate Income Tax (RCIT) due for the month/s of non-compliance, and not merely based on the excess of the 30% WFH threshold. The corresponding penalty shall be paid using BIR Form No. 0605 and shall be determined by computing the difference between the RCIT and the 5% Gross Income Tax (GIT) or the 5% Special Corporate Income Tax (SCIT).

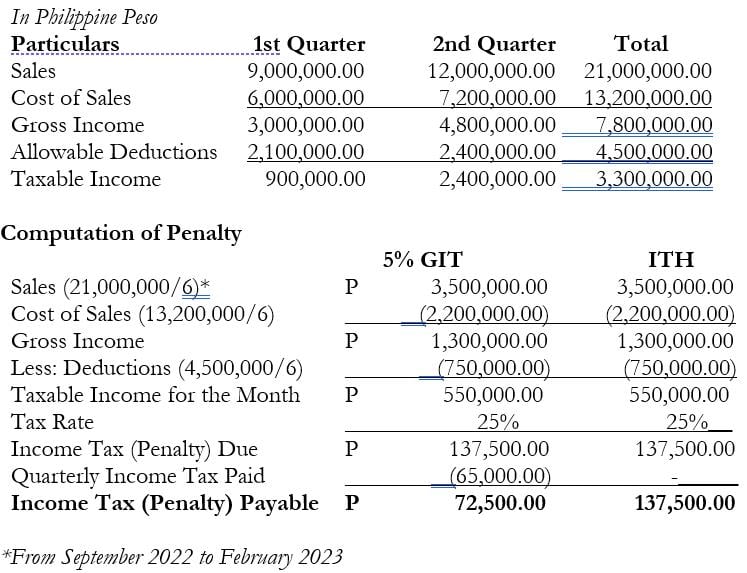

Sample Computation

Income summary of RBE with a fiscal year end of August 31, 2023, whose income is derived solely from its registered activity. The RBE committed a WFH violation for the month of February 2023.

![]()

WFH arrangements were allowed starting March 2020. However, RBEs in the IT-BPM sector in the economic or freeport zone may no longer adopt WFH arrangements beginning January 1, 2023 unless it has already completed its registration with the Board of Investments (BOI) not later than January 31, 2023. Hence, only those registered with the BOI on or before January 31, 2023 may adopt up to a 100% WFH arrangement without adversely affecting their incentives.

Source:

P&A Grant Thornton

Certified Public Accountants

P&A Grant Thornton is the Philippine member firm of Grant Thornton International Ltd.

As published in SunStar Cebu, dated 15 March 2023