How to apply tax amnesty on tax delinquencies

16 Apr 2019The Bureau of Internal Revenue (BIR) has issued Revenue Regulations (RR) No. 4-2019 last April 5, 2019 to provide guidelines for processing tax amnesty on tax delinquencies.

Who can avail?

Any person with tax liabilities covering taxable year 2017 and prior years may avail of Tax Amnesty on Delinquencies under the following cases:

- Delinquent accounts as of the effectivity of RR No. 4-2019, including the following:

- Delinquent accounts with application for compromise settlement either on the basis of (a) doubtful validity of the assessment, or (b) financial incapacity of the taxpayer, whether the same was denied by or still pending with the Regional Evaluation Board (REB) or the National Evaluation Board (NEB), as the case may be, on or before the effectivity of RR No. 4-2019;

- Delinquent withholding tax liabilities arising from non-withholding of tax; and

- Delinquent estate tax liabilities.

- With pending criminal cases with the Department of Justice (DOJ)/Prosecutor’s Office or the courts for tax evasion and other criminal offenses under Chapter II of Title X and Section 275 of the Tax Code, as amended, with or without assessments duly issued;

- With final and executory judgment by the courts on or before the effectivity of RR no. 4-2019; and

- Withholding tax liabilities of withholding agents arising from their failure to remit withheld taxes.

When to avail?

Applications for tax amnesty on delinquencies shall be filed within one year from April 24, 2019.

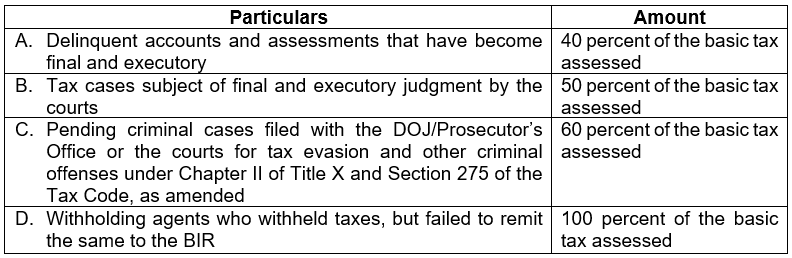

How much is the cost?

The following amnesty rates shall apply:

In cases where the delinquent taxes have been the subject of application for compromise settlement, whether denied or pending, the amount of payment shall be based on the net basic tax as certified by the concerned BIR office.

How and where to file?

Applicants need to submit the following documents:

- Tax Amnesty Return (TAR);

- Duly validated Acceptance Payment Form (APF);

- Certificate of Tax Delinquencies/Tax Liabilities issued by the concerned BIR offices; and

- Copy of the assessments found in the Final Assessment Notice/Final Decision on Disputed Assessment, if applicable.

As published in SunStar Cebu, dated 16 April 2019