Welcoming 2018 with TRAIN

02 Jan 2018THE TRAIN stayed on track and reached its destination in time to take effect yesterday, Jan. 1, as targeted.

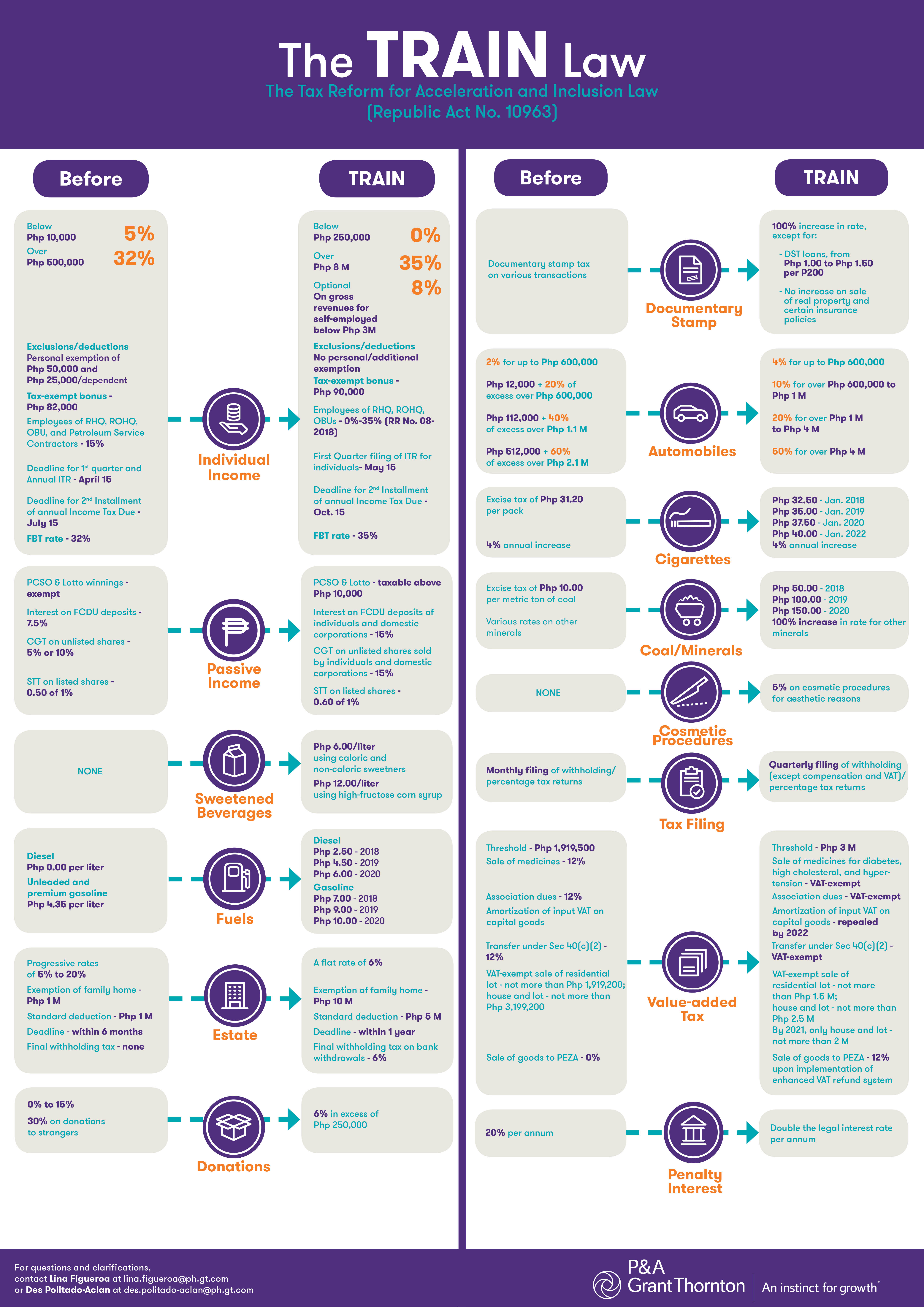

Republic Act (RA) 10963, otherwise known as the Tax Reform for Acceleration and Inclusion (TRAIN) was signed by the President on Dec. 19, 2017, while vetoing certain provisions. As provided in the RA, the new law takes effect on Jan. 1, following its complete publication in the Official Gazette. It was published on Dec. 27.

Hence, on the next payday this January, many employees will take home their salaries in full, without tax deduction. Pursuant to the revised withholding tax table issued by the Bureau of Internal Revenue (BIR) through Revenue Memorandum Circular (RMC) No. 105-2017, there is no withholding for those receiving P685 daily wage; P4,808 weekly wage; P10,417 semi-monthly wages; or P20,833 monthly wage. We must credit the BIR for preparing the Table well in advance even while the legislation has not yet been approved. You can access the withholding tax table through this link.

The Department of Energy (DoE) has likewise issued clarifications that, although the higher petroleum excise taxes take effect on Jan. 1, the higher taxes do not apply to old stocks which have been imported or released from the refineries earlier and excise taxes for which has already been paid at the old rates.

Several provisions of the TRAIN will require further interpretation which should be addressed in the implementing regulations to be issued by the BIR.

Among others, the veto message of the President opted to prioritize fairness and declared that employees of RHOs, ROHQs, OBUs and petroleum service contractors should follow the regular rates applicable to other individuals. However, the remaining provisions after the veto still suggest that employees of existing RHQs, ROHQs, OBUs and petroleum service contractors can continue to enjoy the 15% preferential income tax rate.

The new provisions for VAT zero-rating of services to the Philippine Economic Zone Authority (PEZA) and TIEZA entities were likewise vetoed. However, I note that, even prior to TRAIN and without these new provisions, there is a legal basis for the zero-rating of the services under the PEZA law (RA 7916), which was not repealed.

We will eagerly wait on how the BIR will interpret the Presidential veto on these provisions.

I am sharing the highlights of the TRAIN as prepared by our firm, P&A Grant Thornton. This summary is based on our interpretation of the provisions of the law. Please note that some of these may change, particularly on the gray areas discussed above, depending on the implementing regulations that will be issued by the BIR.

Lina P. Figueroa is a principal with the Tax Advisory and Compliance division of P&A Grant Thornton.

As published in BusinessWorld, dated 02 January 2018