Taxation of ‘passed-on’ GRT

20 Dec 2016The principles of a sound tax system are fiscal adequacy, administrative feasibility, and theoretical justice. Fiscal adequacy means the sources of revenue must be sufficient to meet government expenditures and other public needs. Administrative feasibility means tax laws and regulations must be capable of being effectively enforced with the least inconvenience to the taxpayer. And theoretical justice means that a sound tax system must be based on the taxpayers’ ability to pay.

On June 13, the Bureau of Internal Revenue (BIR) issued Revenue Memorandum Circular (RMC) No. 62-2016, wherein the BIR ruled that banks and non-bank financial intermediaries (NBFI) performing quasi-banking functions may shift to their clients/borrowers the Gross Receipts Tax (GRT) due on transactions subject to certain tax payment on the passed-on amount.

However, with the change in the government in July, the new Commissioner of the BIR, issued Revenue Memorandum Circular (RMC) No. 69-2016, which suspends until further notice the issuances of his predecessor in the period covering June 1 to 30, 2016. As such, RMC No. 62-2016 was suspended until Dec. 2, 2016, when the BIR issued RMC No. 127-2016, which lifted the suspension of the said regulation. Hence, the RMC on passed-on GRT is now effective.

In the said memorandum circular, the BIR emphasized that all banks, NBFIs performing quasi-banking functions, financing companies and other financial intermediaries not performing quasi-banking functions doing business in the Philippines are directly liable for GRT. Hence, the GRT “passed-on” to customers/clients/borrowers shall form part of the tax base for gross receipt tax purposes given that “gross receipts” is defined as “actual or constructive receipt” of income. Since the entities mentioned above are directly liable for GRT on gross receipts derived by them from business operations, the “passed-on” GRT shall be considered as receipt of gross income. In short, the “passed-on” GRT is an additional gross receipts subject to GRT as “other fees and charges.”

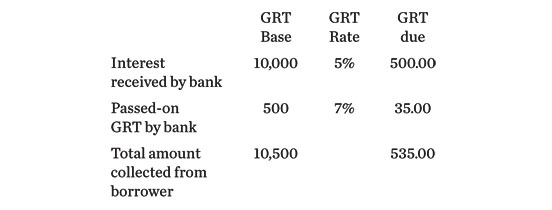

Effectively, banks and NBFIs performing quasi-banking functions lending funds will have to settle two levies: one, on the actual loan interest which is taxed at 5% pursuant to Section 121 (a) of the NIRC, and another on the income they supposedly generated for passing the GRT first to borrowers, which is taxed at 7% pursuant to Section 121 (c) of the NIRC. In case the recipient of the “passed-on” GRT is a NBFIs not performing quasi-banking functions, the “passed-on” GRT shall form part of the tax base subject to 5% GRT.

To illustrate:

As stated above, the passed-on GRT is considered as other fees and charges consistent with Section 2 of the Bangko Sentral ng Pilipinas Circular No. 370 (Updated Rules Implementing the Truth in Lending Act to Enhance Loan Transaction Transparency).

Under the memorandum circular, borrowers may claim as tax deduction the GRT passed to them by banks once they file their income taxes provided the appropriate tax has been withheld. For banks and NBFIs, it can claim the GRT paid as deductible expense for income tax purposes subject to the actual remittance of the GRT.

Evidently, the GRT on the “passed-on” GRT is an additional burden on the banks and NBFIs, and also to the borrowers. For the banks and the NBFIs, this is an additional tax that they will be subject to. Naturally, they will find ways to recover the additional tax from their borrowers/lenders/clients. As such, it will ultimately increase the cost of borrowing.

Also, charging different levies on interest income and passed-on GRT means more accounting work for the banks. For borrowers, it will likewise complicate accounting/reporting if the interest and passed-on GRT has to be in different accounts. Also, even withholding taxes will have to be accounted for separately for it to be properly deductible pursuant to the requirements set by the regulations.

Along with the various tax reform programs of this administration, it is also equally important to find ways to simplify our tax system instead of further complicating it. A simplified tax system encourages compliance among the taxpayers and improves collection efficiency of the tax authorities. Considering the various projects of this administration, both taxpayers and tax authorities must work together to improve collection efficiency while at the same time maintaining a sound tax system in the country.

Ed Warren L. Balauag is a senior tax associate of the Tax Advisory and Compliance Division of Punongbayan & Araullo.

As published in Business World, dated 20 December 2016