Taking a bypass to a tax reform

18 Oct 2016With the Duterte government’s aggressive pursuit of reforms to bring about a simpler, more equitable and more efficient tax system that can encourage investment, job creation and poverty reduction, the Department of Finance (DoF) recently presented its proposed Tax Policy Reform Program as of Sept. 28. The proposed tax policy packages cover several areas of the tax system such as the personal income, consumption, corporate income, property and capital income taxes.

From these tax policy propositions, it is apparent that the administration is thinking about extensively revamping the Philippine tax system. This big move is highly commendable. However, the question is, can this tax reform be really accomplished within a span of the President’s term? Or are we becoming too idealistic about it that we overlook the setbacks that the country may encounter along the way? In short, what is the best possible way to do it?

One of the leading proponents of tax reform since the previous administration, Marikina Rep. Miro Quimbo has re-filed his proposal in the 17th Congress to index the individual income tax brackets to inflation based on the Consumer Price Index (CPI). Rep. Quimbo’s House Bill 20 proposes a simpler, more efficient, and equitable tax system that primarily aims to reduce the tax burden of more than six million Filipino workers. Further, his proposal to execute the tax reform in stages in order not to risk the country’s fiscal position should be given ample consideration. In fact, the government has recognized the proposal and made it a part of its 10-point economic agenda.

However, although DoF’s proposed Tax Policy Reform Program is structured to initially have six packages, with each package to constitute a separate house bill, it may still take a great amount of time, and not to say, numerous legislative deliberations and revisions before a single house bill can be passed into law. Considering that each package involves modifying several areas of the existing tax laws in order to balance the trade-offs of implementing revenue-eroding measures, the Congress will have to carefully scrutinize and evaluate each package, and this will clearly take time.

Let’s take as an example the first package in the program. This comprises the personal income tax and the consumption tax. In this package, the income tax brackets will be adjusted; the personal income tax maximum rate will be increased from 32% to 35% but you have to earn an annual income of more than P11 million before you feel a higher tax hit; and there will be a shift to a modified gross system to simplify the personal income tax. However, in order to offset the possible revenue loss on the part of the government, the package is integrated with some measures to mitigate the effects of the proposed adjustments. These offsetting measures include expanding the VAT base by limiting exemptions to raw food and other necessities; increasing the excise on all petroleum products; and increasing excise on automobiles. Considering that these various measures will be incorporated in a single house bill, it is doubtful that the same will be passed into law in the near future.

So how can the Duterte administration immediately implement a tax reform?

According to Mr. Quimbo, while his initial proposal was to overhaul the entire income tax system, the indexing of the income tax brackets to inflation is the most urgent step in the quest for genuine reform. He further explained that once the tax brackets have been adjusted, a Teacher I earning P241,137 per annum who currently pays P14,231 in taxes will only be taxed P9,935. The additional take home pay of P4,296 can be used to increase his family’s budget for education and savings. The savings become even more significant for those who have higher salaries.

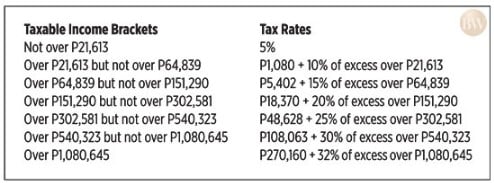

The proposed indexation of the income tax brackets is shown below.

This particular modification in the income tax brackets will greatly improve the spending capacity of every Filipino worker, especially the low to middle income earners.

Moreover, it is more likely Congress will enact tax reform if the house bill only covers the adjustments in the income tax brackets. This might be the most urgent step that the government may take in order to achieve a tax reform. The amendments in the other areas of the tax system may then be pursued afterwards.

One of the challenges for this proposition to amend the income tax table is the reduction in the revenue of the government. But this may be addressed through a more effective and efficient collection system of the tax administrations of the government such as the Bureau of Internal Revenue (BIR) and Bureau of Customs (BoC). At present, we have other sources of revenue that the government may exploit to minimize the adverse effects of the adjustments in the income tax brackets.

Regardless of the revenue loss that the government might possibly suffer upon implementing these proposed income tax brackets, the Congress should always be mindful of the Constitution’s mandate that taxation be uniform and equitable and that Congress promote a progressive system of taxation.

Besides, it is about time that we revisit our existing income tax table. This has been in our tax system since 1997. Economic and financial conditions way back then were entirely different from today. Nevertheless, all the amendments and improvements in the DoF’s proposed Tax Policy Reform Program are something worthy of our attention and, more importantly, of our support. This most-awaited tax reform may take time, but we hope it will happen in the near future.

Doris Moriel B. Tampis is an associate of the Tax Advisory and Compliance Division of Punongbayan & Araullo.

As published in Business World, dated 18 October 2016.