Last-minute reminders before the holidays

22 Dec 2020As one of the young professionals working and living away from their families, December is definitely one of the months I look forward to. Booking a flight, buying gifts, and planning for a vacation give me a different but good kind of rush. December is also usually the month when I re-evaluate the visions I have set for myself, look back on the decisions I made, and assess if I still get fulfillment from the things I do. However, this year was extremely different. I have to remind myself that surviving difficult times is a success in itself, that taking a break does not necessarily mean abandoning your dreams. That it is fine to rest, keep the faith, and just strike later.

Just like how this year changed an aspect of our lives and forced us to recalibrate our mindsets, several regulations were also issued by the Bureau of Internal Revenue (BIR) to help taxpayers cope with the difficult times that faced us. Listed below are the deadlines that we need to look out for as they come due after getting extended.

Related Party Transactions Return (BIR Form 1709)

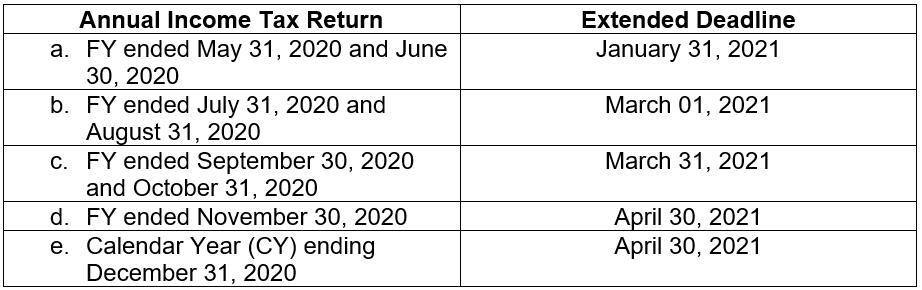

The first deadline for the submission of Information Return on Related Party Transactions (BIR Form 1709) and supporting documents as attachments to Annual Income Tax Return is already on December 29, 2020. This deadline is for companies with accounting periods ended Fiscal Year (FY) March 31, 2020 and April 30, 2020. Deadlines for submission by companies with periods ending on other than the above dates are as follows:

These deadlines were a further extension pursuant to Revenue Memorandum Circular (RMC) No. 98-2020 to give taxpayers ample time to prepare and file. This is considering that the effectivity of the submission requirement was only on July 25, 2020 pursuant to Revenue Regulations (RR) No. 19-2020.

As clarified in RMC No. 76-2020, BIR Form 1709 shall be manually filed at the Large Taxpayers (LT) Division/ Revenue District Office (RDO) where the taxpayer is registered. A penalty of not less than P1,000 but not more than P25,000 shall be imposed for failure to file BIR Form 1709 and its required attachments due to reasonable cause and not willful neglect. In case of repetitive offense, the maximum penalty of P25,000 shall be imposed. If after receiving valid summons and the taxpayer still fails and neglects to produce the form and attachments, the responsible officer shall be punished by a fine of not less than P5,000 but not more than P10,000 and suffer imprisonment of not less than one year but not more than two years*.

Filing for VAT refund claims

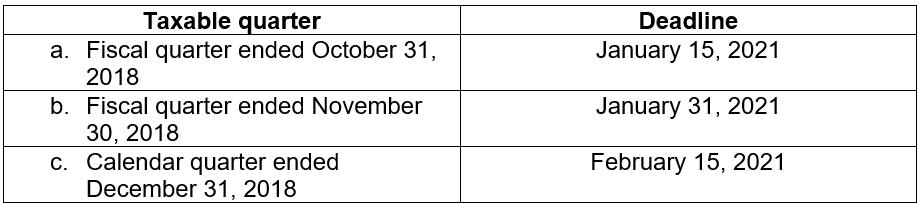

The application for VAT refund claims covering calendar quarter ended September 30, 2018 will be due on December 31, 2020. Deadlines for the application for VAT refund claims covering other taxable quarters are as follows:

Pursuant to RR No. 28-2020, areas with enforced Enhanced Community Quarantine (ECQ) or the Modified Enhanced Community Quarantine (MECQ) after December 29, 2020 shall be given an additional 30 days after the lifting of the ECQ or MECQ to apply for VAT refund claims. The 90-day period of processing of VAT refund claims shall likewise be suspended and shall only resume after 30 days from the lifting of ECQ or MECQ.

Voluntary Assessment and Payment Program (VAPP)

To gain additional tax revenues to fund government expenditures during the pandemic, the BIR implemented VAPP for the calendar year ended December 31, 2018 and fiscal years ended July 2018 to June 2019. The last day to avail of the program, which started last September 21, 2020, is on December 31, 2020**.

Covered taxpayers may either be individual or juridical entities, including estates and trust who erroneously paid or failed to pay the covered taxes for the covered periods due to inadvertence or otherwise.

An availing taxpayer may file personally or through a courier service. Payments shall be made in cash to any BIR Authorized Agent Bank (AAB) under the LT office/ RDO having jurisdiction over the taxpayer, except for one-time transactions (ONETTs) involving the sale of property which must be filed or paid with AABs/ Revenue Collection Officers (RCOs) under the RDO covering the location of the property.

Availment of Tax Amnesty on Delinquencies (TAD)

TAD can only be availed until December 31, 2020*** by those taxpayers with internal revenue liabilities for taxable year 2017 and prior years. Any person, whether natural or juridical may avail of the said TAD.

The availment of TAD shall be considered fully complied with upon completion of all the steps provided in RR No. 15-2020 on or before December 31, 2020. The December deadline is a further extension provided under RMC No. 61-2020 pursuant to Republic Act (RA) No. 11213 or the Bayanihan to Heal as One Act which directed government offices to suspend deadlines for the duration of the community quarantine.

Suspension of BIR audit and field operations

Starting December 15, 2020 until January 27, 2021, no field audit, field operations, or any form of business visitation in execution of Letters of Authority (LOAs)/ Audit Notices or Mission Orders should be conducted. During this period, taxpayers may enjoy the holidays as no written orders to audit and/ or investigate their internal revenue tax liabilities shall be served, unless of course to those that are enumerated in RMC No. 127-2020 who may still be subjected to audit.

Service of notices to avail the TAD, Estate Tax Amnesty (ETA) and VAPP are not covered by the suspension. Also, taxpayers may still voluntarily pay their known deficiency taxes without the need to secure authority from concerned revenue officials.

It is important for taxpayers to note that after January 27, 2021, BIR audit and field operations will resume and preparations during the suspension will surely come handy.

As we prepare ourselves for the holidays by closing our year with peace of mind for a fruitful upcoming year, it is the same for our dues and obligations to the government. Before we embark on to merry making and making fond memories with our loved ones, it is best that we keep abreast of what is to come since reality dictates that after an end comes a new beginning. May we have a fruitful 2021.

Note:

On December 22, 2020, BIR published RRs to extend deadlines and clarify issues as follows:

a. *BIR Form 1709 : Preparation and submission of TPD is only required for taxpayers who are covered by the submission of BIR Form 1709 and who meet the threshold requirements as provided in RR No. 34-2020

b. **VAPP : Deadline to avail of the VAPP is extended until June 30, 2021. Taxpayers with a duly issued Certificate of Availment shall not be audited for 2018 for the tax types covered by the availment. Hence, taxpayers who availed of the VAPP on withholding taxes shall be allowed to claim deduction on the corresponding income payment pursuant to RR No. 6-2018

c. ***TAD : TAD can be availed until June 30, 2021.

Let's Talk Tax is a weekly newspaper column of P&A Grant Thornton that aims to keep the public informed of various developments in taxation. This article is not intended to be a substitute for competent professional advice.

Paul Vinces C. Leorna is a senior in-charge of Tax Advisory & Compliance division of P&A Grant Thornton, the Philippine member firm of Grant Thornton International Ltd. For comments and inquiries, please email pagrantthornton@ph.gt.com.

As published in BusinessWorld, dated 22 December 2020