Helping our nation through voluntary tax compliance

15 Sep 2020The world we are living in right now is very different from the one we were used to. Whenever I hear news about the rising number of COVID-19 cases, employees losing their jobs, and businesses shutting down their operations, which were all brought about by the COVID-19 pandemic, I find myself helpless.

Thankfully, my mood is lifted by random acts of kindness, such as stories about helping those in need, even in their own little way. These stories always give me hope that if we work together, we can get past this crisis.

We, as a nation, should be helping each other out.

In an effort to help ease the suffering of our countrymen and to respond to the needs of those gravely impacted industries heavily affected by the pandemic, the government has given its taxpayers an opportunity to help defray its expenses by letting its taxpayers avail of the Voluntary Assessment and Payment Program (VAPP).

To implement this, the Bureau of Internal Revenue (BIR) issued Revenue Regulations (RR) No. 21-2020, which sets down the policies and procedures for VAPP, which applies to all internal revenue taxes covering the taxable year ending Dec. 31, 2018, and the fiscal year 2018 ending on the last day of the months of July 2018 to June 2019. Qualified taxpayers can avail of the benefits of the VAPP starting from Sept. 21 until the end of this year unless extended by the Secretary of Finance.

Any taxpayers, who inadvertently or otherwise, erroneously paid their internal revenue tax liabilities or failed to file tax returns/pay taxes, may avail of the benefits under the VAPP, except for the following:

• Taxpayers who have already been issued a Final Assessment Notice (FAN) that have become final and executory, on or before the effectivity of this RR;

• Persons under investigation as a result of verified information filed by a Tax Informer under Section 282 of the NIRC of 1997, as amended, with respect to the deficiency taxes that may be due out of such verified information;

• Those with cases involving tax fraud filed and pending in the Department of Justice or in the courts; and

• Those with pending cases involving tax evasion and other criminal offenses under Chapter II of Title X of the NIRC of 1997, as amended.

Considering the adverse effects of the COVID-19 on the business operations of taxpayers, what is in it for them should they avail of the VAPP?

1. Exemption from tax audit

Qualified taxpayers who were able to comply with the conditions set forth in the RR, which is a requirement for the application to be considered valid for the availment of the VAPP and be entitled to its privilege, shall have the benefit of having their books exempted from audit of the BIR for the taxable year 2018.

If in case the taxpayer has already an on-going assessment for the taxable year 2018, the audit being conducted shall be suspended. The issued Letter of Authority, Tax Verification Notice, Discrepancy Notice, Notice of Informal Conference, Preliminary Assessment Notice, Final Assessment Notice for pending cases covering the taxable year 2018 shall be withdrawn and canceled.

2. Limited contact between the taxpayer and the BIR

Since the taxpayer will no longer be subject to a regular audit of the BIR for that taxable year, it will limit the face-to-face interaction between the taxpayers and the BIR personnel as compared to if the taxpayers undergo the normal tax audit process.

This will also lessen the risk of possible transmission of the COVID-19 virus between the taxpayer and BIR’s personnel, while at the same time, complying with the Inter-Agency Task Force’s (IATF) health and safety protocols.

But before availing of the program, taxpayers should perform a tax compliance check with the existing tax rules and regulations. The taxpayer should compare the amount of tax exposure, among others, based on its tax compliance review against the amount of tax to be paid for availment of VAPP.

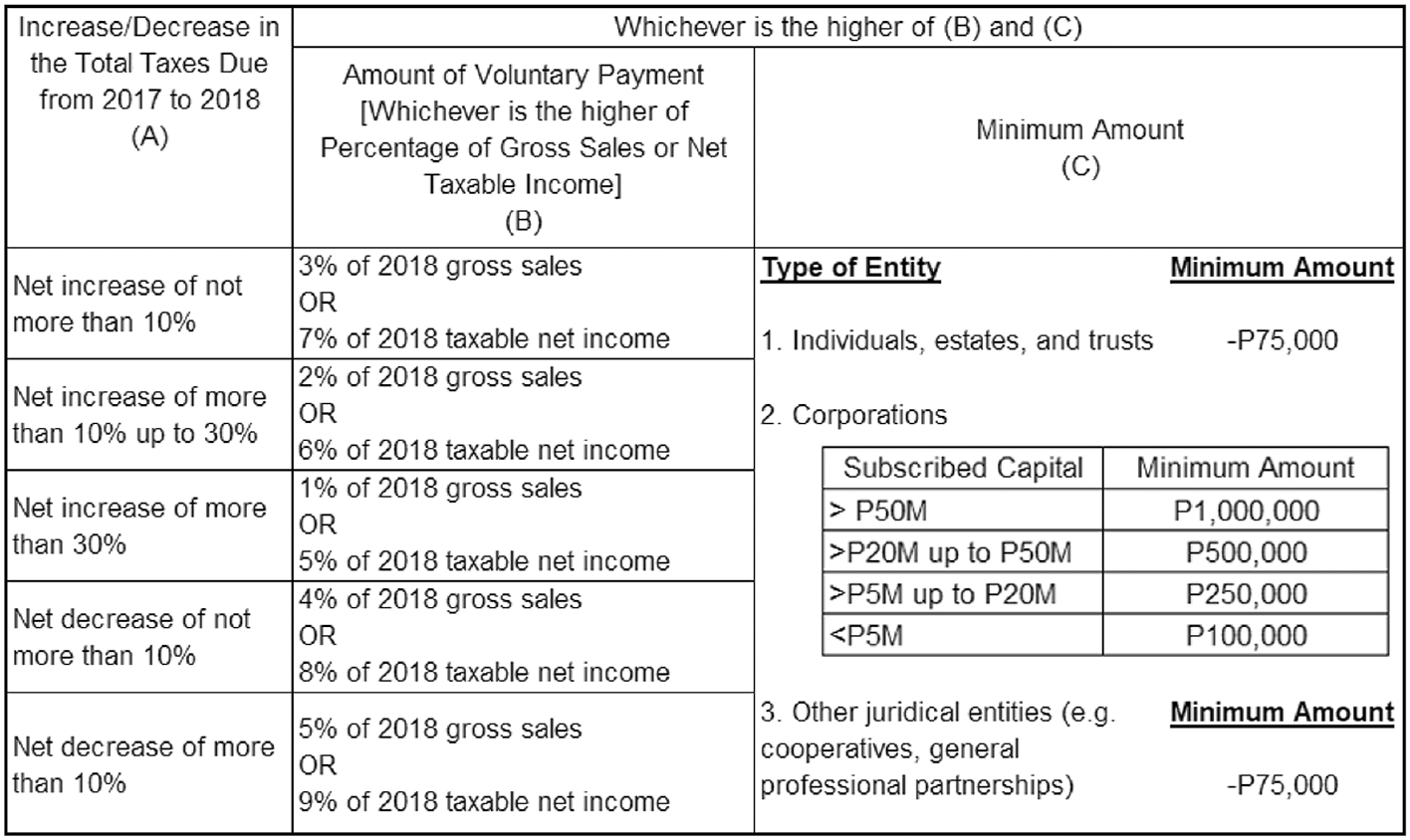

The amount of voluntary payment, which should be paid in cash, shall depend on the tax type as follows:

a. For Income Tax (IT), Value-Added Tax (VAT), Percentage Tax (PT), Excise Tax (ET), and Documentary Stamp Tax (DST) other than DST on One-Time Transaction (ONETT);

b. For Final Withholding Taxes (on Compensation, Fringe Benefits, etc.) and Creditable Withholding Taxes (CWT) other than CWT on ONETT, the amount to be paid shall be 5% of the total basic withholding tax remittance for the taxable year 2018; and

c. For taxes on ONETT, such as Estate Tax, Donor’s Tax, CGT, ONETT-related CWT/Expanded Withholding Tax, and DST, the amount to be paid shall be the basic tax due of the unfiled tax return/unpaid tax due plus 5%.

Moreover, here are the other factors that taxpayers should pay attention should it avail of VAPP:

1. For items a and b of the preceding section, taxpayers must apply all registered taxes indicated therein for the privilege under VAPP be availed;

2. For taxpayers with claims for tax credit/refund, such excess input VAT and excess tax credit for income tax, the taxpayer’s right to apply such claim shall be waived, unless they exclude the specific tax type for which they are pursuing the claim for tax credit/refund; and

3. Taxpayers availing of the VAPP should faithfully comply with all the requirements, such as the submission of a complete set of documentary requirements, and the filing and voluntary payment of taxes in the proper venue, and all other conditions in the RR. Otherwise, the taxpayer shall not be entitled to the privilege under VAPP. In this case, the voluntary payments may be applied against any deficiency tax liability for the taxable year 2018, in case of audit/investigation.

To encourage the taxpayers to avail of the program, the BIR should be proactive in reviewing the applications and communicating with the taxpayers should they find any defects in the applications so that taxpayers can act on the additional requirements.

As provided under regulations, the Revenue Officer assigned should evaluate the documents submitted for application within 30 working days from receipt of the application, and endorse the same to the Assistant Chief, LT Office/Assistant Revenue District Officer (ARDO) for review, and to the Chief, LT Office/Revenue District Officer (RDO) for signature. However, the RR did not specify if the 30 days cover the whole review process up to the approval of the Chief/RDO.

What happens after the 30 days lapse? Can the taxpayers assume that their application is already approved? For the guidance of the taxpayers, the BIR should issue a clarification so that the taxpayers are not left in the dark.

On the other hand, a Certificate of Availment shall be issued by the LT Office/RDO within three working days once the application has been approved. The certificate shall serve as proof of the taxpayer’s availment of the VAPP, compliance with the requirements, and entitlement to the privilege granted under the RR.

While it is true that we should not expect anything in return for acts of kindness, it is good to know that our government appreciates the help and contributions of its taxpayers, and rewards them for it. I can really say that if we keep the spirit of Bayanihan alive in our hearts, we will heal as one.

Let’s Talk Tax is a weekly newspaper column of P&A Grant Thornton that aims to keep the public informed of various developments in taxation. This article is not intended to be a substitute for competent professional advice.

Christian Derick Villafranca is a senior in charge from the Tax Advisory & Compliance division of P&A Grant Thornton, the Philippine member firm of Grant Thornton International Ltd.

As published in BusinessWorld, dated 15 September 2020