Forgetting the past and moving forward for taxpayers

21 May 2019Last Saturday, I had my monthly checkup with my gynecologist. Unfortunately, on our way to the hospital, I slipped off the last stair in our condominium lobby. With my right foot sprained, I thought of rescheduling my checkup, as it was so difficult to walk. With a baby inside me, however, I needed to push through. I needed to ensure that she (Yes, it’s a girl!) is fine and was not harmed due to my carelessness. Thankfully, I was able to proceed with my checkup, and the baby is fine.

Recalling this fearful experience while writing this article, I thought of what Philippine taxpayers go through during a Bureau of Internal Revenue (BIR) audit or assessment. To most Philippine taxpayers, tax assessments are a bad experience that they just want to forget, so that they can move forward with their business.

What are the remedies in order to avoid or at least minimize tax assessments? Is there any remedy if the BIR assessment has become final and executory? How can the taxpayer move forward?

On April 9, while every taxpayer was busy preparing for the filing of their 2018 annual income tax return, the BIR published Revenue Regulations No. 04-2019, providing the much-awaited implementing rules and regulations for the Tax Amnesty on Delinquencies (Revenue Regulations (RR) No. 04-2019).

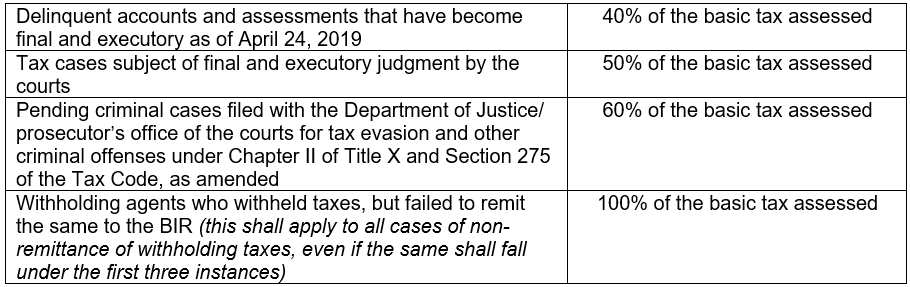

Under the Tax Amnesty on Delinquencies, a taxpayer with final and executory assessments can now opt to close and forget the assessment by paying only a certain percentage of the basic tax assessed.

The table shows the instances when the taxpayer can avail of tax amnesty on delinquencies, and the applicable tax amnesty rates:

If the delinquencies consist only of unpaid penalties due to late filing or payment, and there is no basic tax assessed, the taxpayer may avail of tax amnesty on delinquencies without any payment due.

Tax amnesty on delinquencies may be availed of by qualified taxpayers until April 24, 2020.

To provide further guidelines on and procedures for the processing of applications for a tax amnesty on delinquencies, the BIR also issued Revenue Memorandum Order (RMO) No. 23-2019 on May 8.

To avail of the tax amnesty on delinquencies, a Certificate of Tax Delinquencies/Tax Liabilities (CTD) must be secured from the appropriate BIR office. Under RMO No. 23-2019, the issuance of a CTD shall be based on the list of Accounts Receivable/Delinquent Accounts to be issued by the Accounts Receivable Management Division of the BIR. Such a list shall, however, not include tax liabilities arising from the taxpayer’s own declaration. Does this mean that the former, even if covered by assessment notices that have become final and executory, cannot be covered by tax amnesty?

If the taxpayer validly protested a Final Assessment Notice/Final Letter of Demand, RMO No. 23-2019 explicitly allows the withdrawal of the protest letter. The withdrawal, however, should have been done prior to the effectivity of RR No. 04-2019. Such an option to withdraw is not specifically provided in RR No. 04-2019. Since RR No. 04-2019 took effect on April 24, but RMO No. 23-2019 was issued on May 8, the option to withdraw may no longer be availed of by taxpayers. Many could have benefited from this option had it been specifically provided in the earlier implementing rules and regulations.

As cited in various fora, the tax amnesty on delinquencies is a welcome development for taxpayers who want to move forward from tax assessments that have become final and executory. Moving forward, however, we hope that the BIR will be more transparent on its implementing rules and regulations. Ample time must be given to taxpayers to avail of the options available.

My sprained foot is now slowly healing with the help of an ice pack. The most important lesson that I learned, though, is that I should always be careful for my baby and myself, just like a taxpayer must always be careful about their tax compliance. Tax compliance must be reviewed quarterly or at least annually to minimize issues in case of a tax assessment. Personnel must always stay updated on the latest rules, options, and updates to minimize compliance costs.

With this, P&A Grant Thornton is offering a half-day seminar on Updates on the IRR of the Tax Amnesty Act, The Revised Corporation Code, and Recent Tax Issuances at Holiday Inn and Suites on June 20.

Let’s Talk Tax is a weekly newspaper column of P&A Grant Thornton that aims to keep the public informed of various developments in taxation. This article is not intended to be a substitute for competent professional advice.

Ma. Lourdes Politado-Aclan is a director from the Tax Advisory & Compliance division of P&A Grant Thornton, the Philippine member firm of Grant Thornton International Ltd.

As published in BusinessWorld, dated 21 May 2019