Republic Act (RA) No. 10963 or the TRAIN Law introduced several major revisions to the National Internal Revenue Code (Tax Code) of 1997. While the law became effective 01 January 2018, some changes were made effective through staggered implementation.

One of the notable changes that will be implemented this year is the removal of the monthly filing of Value-Added Tax (VAT) returns. Section 37 of the TRAIN Law, amending provisions of Section 114(A) of the Tax Code of 1997, as amended, and as implemented under Section 4-114-1(A) of Revenue Regulations (RR) No. 13-2018, states that “beginning January 1, 2023, the filing and payment required under this subsection shall be done within twenty-five (25) days following the close of each taxable quarter”. Thus, VAT-registered taxpayers are no longer required to file the Monthly VAT Declaration (BIR Form No. 2550M) for transactions starting January 1, 2023. Instead, they will file the corresponding Quarterly VAT Return (BIR Form No. 2550Q) within twenty-five (25) days following the close of each taxable quarter.

TRANSITORY PROVISION FOR THE YEAR 2023

VAT-registered taxpayers felt a sense of relief when the year 2022 ended, given that they no longer need to file and pay their VAT payable monthly. However, there was a confusion during the initial implementation of the said provision, particularly for taxpayers that are under a fiscal period of accounting. To clarify the rules, the BIR issued Revenue Memorandum Circular (RMC) No. 5-2023 providing transitory rules for the implementation of the quarterly filing of VAT returns.

![]()

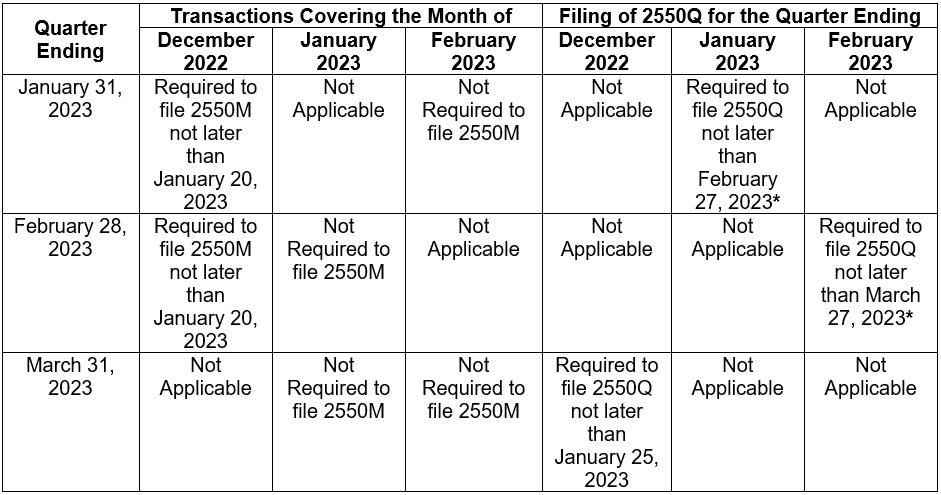

Note: *The 25th day deadline falls on a Saturday

The RMC provides that for taxpayers with quarter ending January 31, 2023, they are still required to file BIR Form No. 2550M for the month ending December 31, 2022 and BIR Form No. 2550Q for the quarter ending January 31, 2023.

For taxpayers with quarter ending February 28, 2023, they are still required to file BIR Form No. 2550M for the month ending December 31, 2022 and BIR Form No. 2550Q for the quarter ending February 28, 2023.

For taxpayers with quarter ending March 31, 2023, they are required to file BIR Form No. 2550Q for the quarters ending December 31, 2022 and March 31, 2023.

With the revised rules, beginning April 2023, all taxpayers who are required to file VAT return shall file the BIR Form No. 2550Q on a quarterly basis.

WHAT TO EXPECT FROM THE BIR

Taxation, in simple terms, “is the act of levying a tax to apportion the cost of government among those who, in some measure, are privileged to enjoy its benefits and must therefore bear its burden”. The three phases of the power of taxation are levying, assessment, and collection. Given that the BIR is the national agency in charge of collecting internal revenue taxes, the collection of funds to implement the government’s projects and objectives is their top priority. Different methods have been enforced to collect taxes and to reach their monthly, quarterly, and annual budget.

When the Tax Code removed the requirement for monthly filing and payment of Expanded Withholding Tax and Final Withholding Tax in 2018, the BIR still mandated the withholding agents to file a remittance form on a month basis for the first two months of the quarter. The BIR reasoned that taxes withheld by the withholding agents are held in trust for the government and its availability is an imperious necessity to ensure sufficient cash inflow to the National Treasury.

Although this may not be the same case with VAT, by the end of 2022, some taxpayers were anxiously awaiting news if the BIR will also require the filing of a monthly remittance return for VAT. Fortunately, RMC 5-2023 was issued on 13 January 2023, allaying the apprehensions of taxpayers and clarifying the rules.

REVISION OF THE BIR FORM NO. 2550Q

After the transitory provision under the RMC 5-2023, taxpayers who are required to file the VAT returns will no longer need to use BIR Form No. 2550M. Moreover, the current version of BIR Form No. 2550Q may be revised in the near future, removing item no. 26A - Monthly VAT Payments - previous two months in line with the provision under Section 37 of the TRAIN Law.

MOVING FORWARD

The removal of the monthly filing and paying of VAT favorably affects taxpayers in two ways. First, it impacts taxpayers’ cash flow as they will be able to hold on to their cash for the first two months of each quarter. This will allow them to use the funds in the meantime and hopefully, reduce short term borrowing. Second, it simplifies their VAT compliance requirements. This move of the government further strengthens ease of doing business in the Philippines and allows taxpayers to devote more time to their core businesses.

Despite the favorable provision of removing the monthly filing ang payment of VAT return, the taxpayers should not be complacent when it comes to the preparation of the quarterly VAT returns. It is still recommended to prepare the schedules and computation monthly to avoid spending too much time processing and filing three months’ worth of transactions all at once.

Taxpayers should also keenly follow the discussions related to the Ease of Paying Taxes bill which is now pending in the Senate. The bill proposes new rules aimed at further simplifying VAT rules and making paying taxes less burdensome for taxpayers.

Let's Talk Tax is a weekly newspaper column of P&A Grant Thornton that aims to keep the public informed of various developments in taxation. This article is not intended to be a substitute for competent professional advice.

As published in BusinessWorld, dated 07 February 2023