Taxes are integral part of nation-building. Its pivotal role is to spur the nation towards progress and enable the government to deliver essential public services to its citizens. When we, as citizens, understand how critical our tax contributions are to the country’s growth, paying taxes becomes more than just compliance or mandatory practice.

The signing of Republic Act No. 11967, commonly known as the Ease of Paying Taxes (EOPT) Act, into law on January 5, 2024, serves not only to modernize the current tax administration but also to update the taxation system. It also provides a more comprehensive and streamlined process aimed at encouraging more taxpayers to pay taxes on time and foster compliance. The law will be effective on 22 January 2024.

Despite having no major tax reforms signed into law in 2023, Congress was able to approve RA 11956, or the Extension of Estate Tax Amnesty. The law extended the estate tax amnesty for another two years, or until June 14, 2025. It also extended the coverage to include estate taxes which accrued as of May 31, 2022. The amnesty rate remains at 6% based on the decedent's net estate. This extension gives much needed additional time to heirs in preparing the required documents and finally settling the estate of their relatives.

Present tax reforms and initiatives are focused on improving the nation's tax-to-gross domestic product (GDP) ratio. This year, BIR has set a collection target of Php 3.046 trillion, a 15 percent increase from last year’s target.

The salient changes introduced by the EOPT Act are as follows:

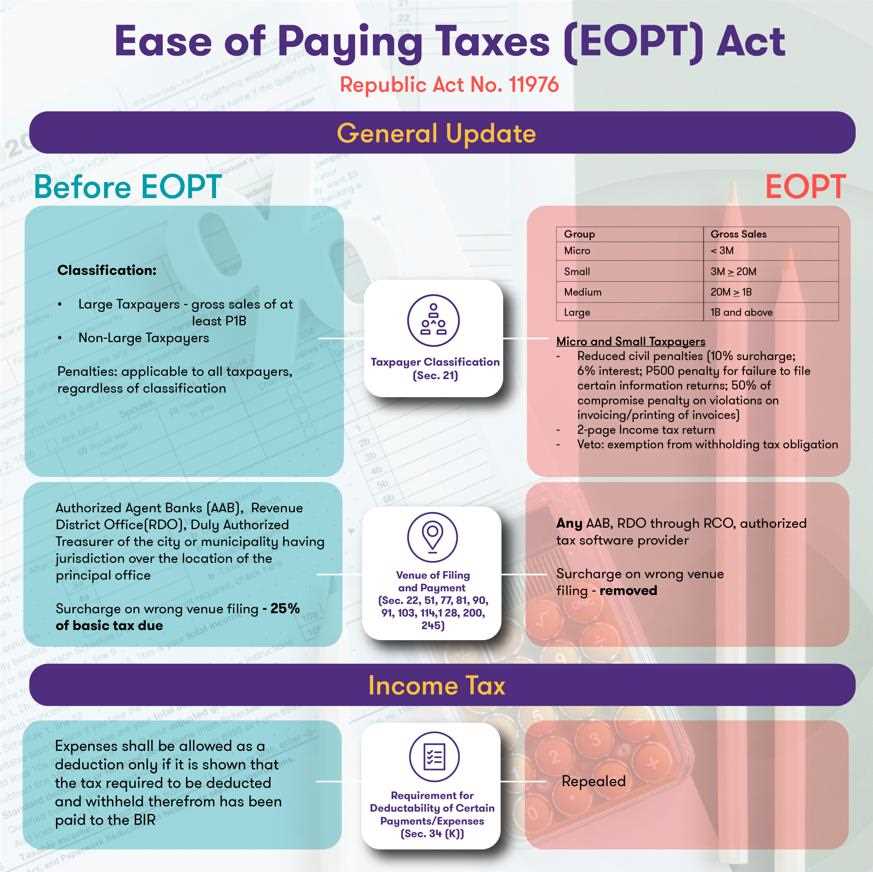

- Taxpayers are now divided into four groups: Micro (under P3 million), Small (between P3 and 20 million), Medium (between P20 million and P1 billion), and Large (over P1 billion). To address the potential understatement of tax obligations that could impact the government's financial flows, the President vetoed Section 8 of the Act, which exempts micro-taxpayers from withholding creditable income tax.

- Payment of the annual registration fee of Php 500 is no longer required. Existing certificates of registration, which include the registration fee, remain valid but can be replaced or updated at the Revenue District Office (RDO) where the business is registered on or before December 31, 2024.

- The fixed venue for payment of taxes was removed. Taxpayers can now file and pay anywhere, either electronically or manually, with any authorized agent bank, Revenue District Office through the Revenue Collection Officer, or authorized tax software provider. Consequently, surcharges for paying at the wrong venue were removed.

- The existing “whichever comes first” rule for withholding taxes no longer applies. The rules for withholding taxes were simplified. Thus, withholding taxes is now required at the time the income becomes payable.

- Section 34 (K) of the Tax Code, which requires withholding of taxes for deductibility of expenses from gross income, was repealed, eliminating disallowing of expenses due to non-withholding.

- The uniform basis for Value Added Tax (VAT) was adopted. VAT for both sale of goods and sale of services is now based on GROSS SALES. VAT invoices have become the only supporting document for declaring output taxes and claiming input taxes. In doing so, the accrual basis for income tax and VAT purposes is aligned, eliminating huge discrepancies between gross sales declared in the ITR and VAT returns. However, for service providers, this change may impact taxpayers' cash flows, so better planning is needed.

- VAT refund claims are classified as high-risk, medium-risk, or low-risk, with medium- to high-risk claims undergoing audit and verification. Taxpayers can appeal the decision of the BIR to the Court of Tax Appeals within 30 days from receipt of denial or after the 90-day period.

- For refund claims arising from erroneous or illegal tax collection, the BIR must act within 180 days from submission of complete documents. The timing of filing the appeal to the Court of Tax Appeals has been changed. Taxpayers may appeal to the CTA within 30 days of receipt of denial or lapse of 180-day period.

- Mandatory issuance of invoice for each sale of goods and services was raised from P100 to P500.

The BIR is given 90 calendar days from the effectivity of the law to issue the implementing rules and regulations. Taxpayers are given six (6) months from the effectivity of the implementing rules and regulations to comply with the amendments on VAT and other percentage taxes.

Pending tax reforms for 2024

The remaining tax reform packages as initially identified under the Duterte administration have remained pending with the Senate to date. These are the Passive Income and Financial Intermediary Taxation Bill and the Real Property Valuation Reform Bill. In addition, there are still several tax bills that are pending in the Philippine Senate, namely:

- Digital Services Tax Bill imposes a 12% VAT on transactions of digital services providers such as online auction hosts, subscription-based services, e-learning and marketing services.

- Enhancing the Fiscal Regime for the Mining Industry seeks to limit interest expense deduction of metallic mining contractors, imposes a royalty rate on large-scale metallic mining operations within mineral reservations equivalent to 4% of gross output, imposes a margin-based royalty on income from operations outside mineral reservations equivalent to 1%-5%, and imposes a royalty rate for small-scale operations equivalent to 1/10th of 1% of gross output.

- Create More seeks to address uncertainty over the implementation of VAT and tax administration provisions of the CREATE Act. It mandates the simplified VAT refund system, clarifies VAT regime for registered business enterprises, defines the power of the President to grant incentives, allows BPOS to undertake work-from-home schemes, etc.

The new year greets us taxpayers with a new law simplifying payment of taxes and compliance requirements. Reforms aimed at making tax rules easy to understand and comply with are needed to encourage taxpayers to pay their taxes. Complicated rules distract taxpayers from focusing their efforts on compliance. Continuous collaboration between tax administrators and taxpayers is crucial to effectively implementing the new law. As we start the year with a new law, let us all strive to be tax compliant and pay our taxes properly.

As published in The Manila Times, dated 17 January 2024