Accounting Alerts

- 2024

- 2023

- 2022

- 2021

-

2020

2020

- Extension of Deadline for Submission of Forms/Notices

- Online and Manual Submission of Forms/Notices Pursuant to SEC MC 28-2020

- COVID-19 Accounting Implications for CFOs - Debt Modifications

- Discussion Paper 'Business Combination under Common Control'

- SEC Memorandum Circular No. 32 series of 2020

- SEC Memorandum Circular No. 31 series of 2020

- SEC Memorandum Circular No. 28 series of 2020

- Insights into PFRS 16 - Lease Incentives

- IASB issues Interest Rate Benchmark Reform Phase 2

- IFRIC 23 - Uncertainty Over Income Tax Treatments

- COVID-19 Going Concern Considerations

- Extension of Deadlines and Interim Procedures for the Submission of Printed/Hard Copies of Annual Reports

- IASB Defers the Effective Date of IAS 1 Amendments

- Guidelines on the Electronic Submission of the Annual Report and Audited Financial Statements to BSP

- Filing of Annual Reports During the Temporary Closure of the SEC Main Office until July 26, 2020

- Work Suspension at the SEC Main Office and Extension of Deadlines for Certain Corporations

- Adjustment of Deadlines for Submission of Annual Reports to the SEC and Other Announcements

- Amendments to IFRS 17 and IFRS 4

- Filing of Reports and Other Documents in SEC Main Office during Temporary Closure

- Options for the Submission of Reports, Applications and Other Documents to the SEC During Community Quarantine

-

2019

2019

- SEC Extends Deadline for Annual and Quarterly Reports for...

- Deferral of IFRIC Agenda Decision on Over Time Transfer of Constructed Goods (PAS 23) for Real Estate Industry

- Implementation of IFRS 17, Insurance Contracts

- Amendments to Regulations on Financial Audit of Banks and Non-Bank Financial Institutions

- Navigating the Changes to IFRS 2020

- SEC Memorandum Circular No. 2 - 2020 Filing of Annual Financial Statements and General Information Sheet

- IASB issues Classification of Liabilities as Current or Non-current (Amendments to IAS 1)

- GTI IFRS News Q4 2019

- Insights into PFRS 3: Definition of a Business

- IASB issues Interest Rate Benchmark Reform

- Insights into PFRS 16: Presentation and Disclosure

- Insights into PFRS 16: Lease Payments

- Insurance Commission's Guidelines on Lease Accounting for Insurance and Reinsurance Companies

- GTI IFRS News Q1 2019

- Application Deferral of PIC Q&A 2018-H and 2018-14

- Sustainability Reporting Guidelines for Publicly-Listed Companies

- Insights into PFRS 16: Sale and Leaseback Accounting

- Insights into PFRS 16: Transition Choices

- Use of the New General Information Sheet (GIS) Form

- 2019 Filing of Annual FS and GIS

- Navigating the Changes to IFRS 18

- Insights into PFRS 3: Definition of a Business

- GTI IFRS News Q2 2019

- Rules on Material Related Party Transactions for Publicly-listed Companies

- BOA Repealed Resolutions on FS Compilation Services

- GTI IFRS News Q3 2019

- 2019

- 2018 2018

- 2017

- 2016

- 2015

- 2014

- 2008

- 2007

- 2006

- 2005

COVID-19 Accounting Implications for CFOs - Debt Modifications

This Accounting Alert is issued to discuss the requirements of PFRS 9, Financial Instruments, and the judgment involved in determining the impact of COVID-19 in the debt modification.

Background

The COVID-19 global pandemic has resulted in economic consequences that many reporting entities may not have had to previously consider. One of the consequences is their ability to repay loans. In response, some lenders have agreed to changing the borrowing terms or providing waivers or modification to debt covenant arrangements. Any changes to the terms of loan agreements, for example providing any kind of payments holidays on either principal or interest or changes interest rates should be carefully assessed.

Accounting for Debt Modification

Debt restructuring can take various legal forms including:

- an amendment to the terms of a debt instrument (e.g., the amounts and timing of payments of interest and principal) or

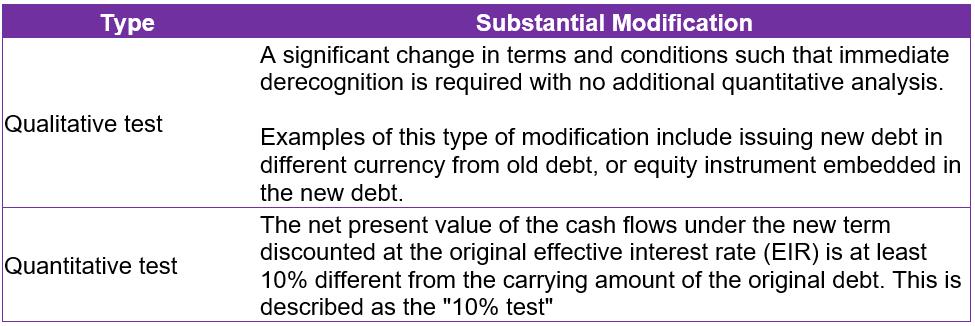

- a notional repayment of existing debt with immediate re-lending of the same or a different amount with the same counterparty. The borrower will usually incur cost in a debt restructuring, and other fees might also be paid or received. The accounting for debt modification depends on whether it considered to be "substantial" or "non-substantial".

There are two tests to check whether the modification is substantial, and these are as follows:

PFRS 9 contains guidance on non-substantial modification and the accounting in such cases. It states that costs or fees incurred are adjusted against the liability and are amortized over the remaining term. That same guidance is silent on other changes in the cash flows.

Fees Paid in a Non-Substantial Modification

In a non-substantial modification, the liability is restated based on the net present value of the revised cash flows discounted at the original EIR. This amount is compared to the previous carrying amount and the difference is recognized in the profit or loss. However, PFRS 9 specifically states in its application guidance, that costs and fees incurred are adjusted against the carrying amount. Such costs or fees therefore have some impact of altering the EIR rather than being recognized in the profit or loss.

Extinguishment Accounting

Extinguishment account involves:

- de-recognition of the existing liability

- recognition of the new or modified liability at its fair value

- recognition of a gain or loss equal to the difference between the carrying amount of the old liability and the fair value of the new one. Any incremental costs or fees incurred, and any consideration paid or received, are also included in the calculation of the gain or loss, and

- calculating the new EIR for the modified liability, that is then used in future periods. This rate would normally equate to the market rate of interest used in the fair value calculation.

The fair value of the modified liability will usually need to be estimated. It cannot be assumed that the fair value equals the book value of the existing liability. The fair value can be estimated based on the expected cash flows of the modified liability, discounted using the interest rate at which the entity could raise debt with similar terms and conditions in the market.

The accounting alert also includes a flowchart that sets out how to assess whether a debt modification is substantial, the role of fees in the 10% test, and examples of accounting for substantial and non-substantial modifications.

See attached Accounting Alert for further details.

.

Accounting Implications for CFOs - Debt Modification