.

.

.

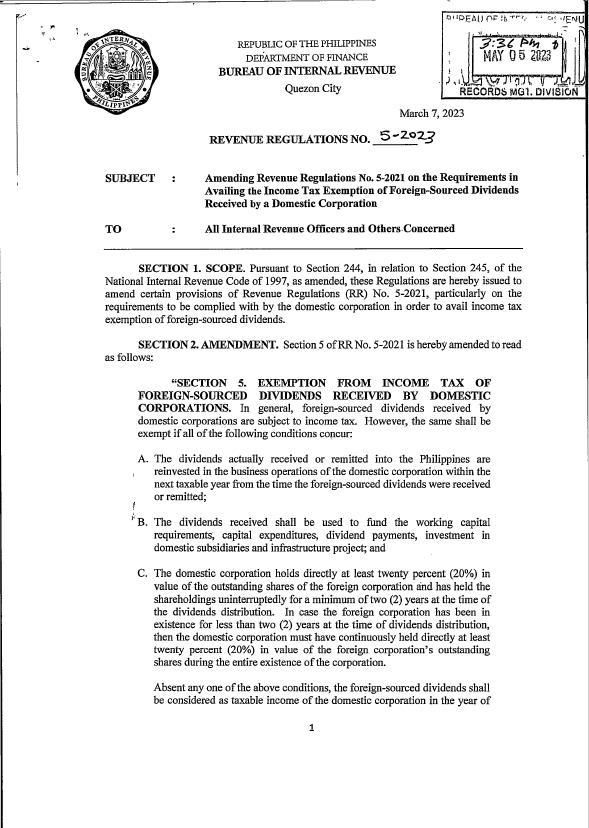

(Revenue Regulations No. 5-2023, issued on May 5, 2023)

This Tax Alert is issued to inform all concerned on the updated requirements to avail of the income tax exemption of foreign dividends received by domestic corporations.

Foreign-sourced dividends received by domestic corporations are generally subject to income tax. However, it may be exempt from income tax if all the conditions provided under Revenue Regulations (RR) No. 5-2021 are met.

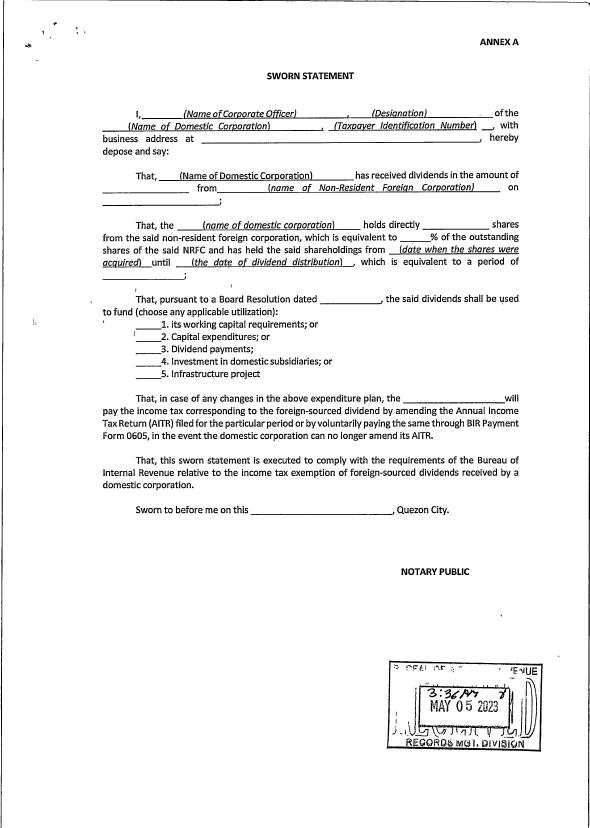

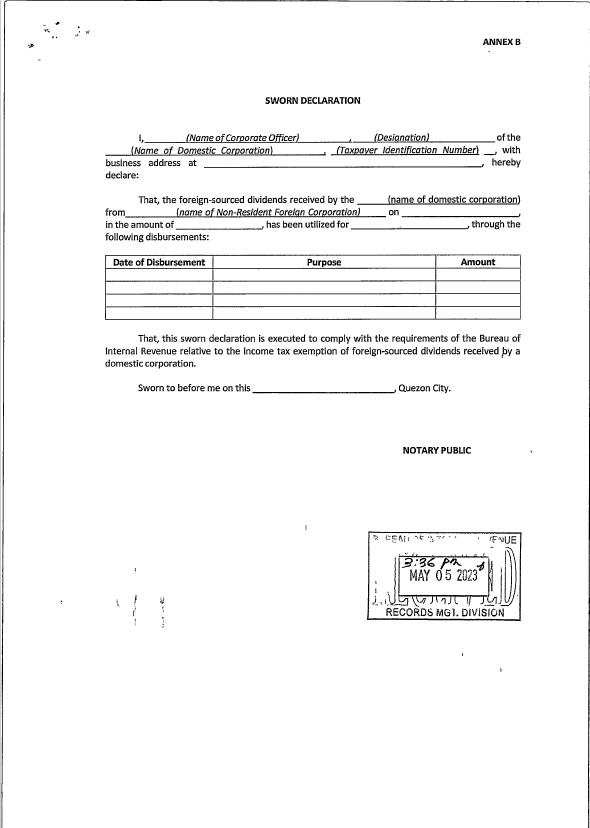

RR No. 05-2023 provides the following updated documentary requirements to comply with to avail exemption from income tax:

Domestic corporations may already avail of the income tax exemption upon compliance with the abovementioned requirements. However, in case of partial or non-utilization of the foreign-sourced dividends, the domestic corporation is required to amend its AITR for the particular period and pay the corresponding tax due thereon, including surcharge, interest and compromise penalties.

In case the amendment of the return is already prohibited since the taxpayer is already under audit, the income tax due shall be paid using payment form BIR Form No. 0605.

.

.

.