(Revenue Memorandum Order No. 8- 2017, April 05, 2017)

This Tax Alert is issued to inform all concerned on the streamlined process of claiming tax treaty relief for nonresident income earners.

BIR has issued these new procedures for claiming tax treaty privileges of nonresident income earners:

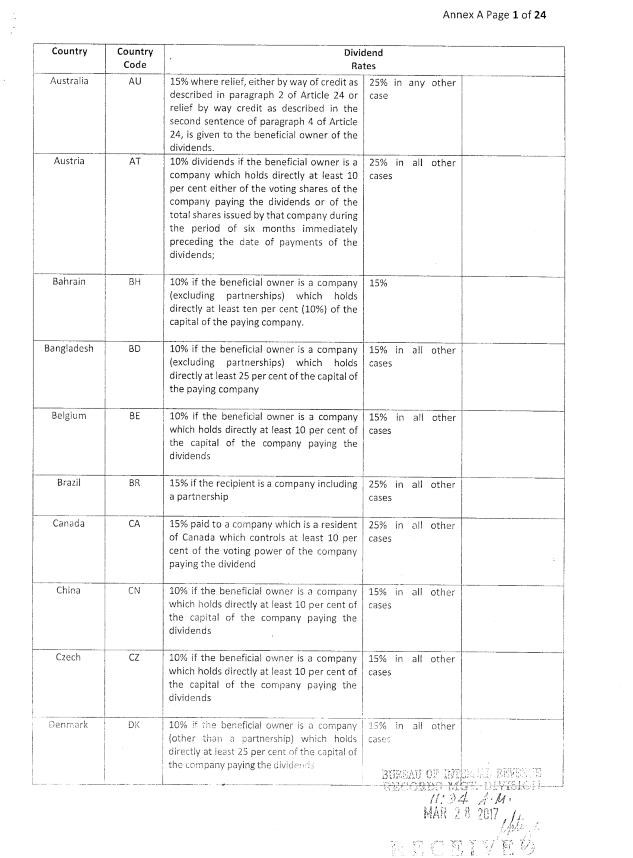

1. Tax Treaty Relief Applications (TTRAs) are no longer required to be filed with the International Tax Affairs Division (ITAD) for dividends, interests and royalties only.

2. The newly created Certificate of Residence for Tax Treaty Relief (CORRT) shall be used in lieu of the 0901 Forms for TTRA. The non-resident income recipient shall submit a duly accomplished CORRT Form to the Philippine income payor/withholding agent before income is paid or credited. Among others, the non-resident income recipient shall have Part I signed by the Competent Authority (Tax Office) of his country of residence certifying that the income recipient is a tax resident of said country. If there is a prescribed certificate of tax residency in the home country, the same shall be attached to the CORRT form in lieu of the signature required in Part I. The authorized representative of the non-resident income recipient shall also sign on both Part I and II of the form.

3. The new form shall be valid for 2 years upon issuance or following the date of validity indicated in the Certificate of Residency, if any, whichever comes earlier.

4. Withholding agents shall apply the reduced treaty rate or exemption upon receipt of the CORRT Form, remit the withholding tax using BIR Form No. 1601-F and file 1604-CF at yearend. For failure to submit the form, regular withholding tax rates shall be applied.

5. The Philippine income payor/withholding agent shall submit an original of the CORRT Form to ITAD and RDO No. 39 within 30 days after payment of withholding taxes due on the interest, dividend or royalties.

6. In case there is another dividend payment within the period of validity of the CORRT, and in case of staggered payments of interest and royalties, the withholding agent only needs to submit an updated Part II within 30 days from payment of the withholding taxes.

7. The CORTT form which shall also serve as proof of residency of the nonresidents shall contain the following information:

|

Part I |

|

|

✓ |

Applicable Tax Treaty |

|

✓ |

Information of Income Recipient/Beneficial Owner (Individual); |

|

✓ |

Information of Income Recipient/Beneficial Owner (Non-Individual); and |

|

✓ |

Certification of Competent Authority or Authorized Tax Office of Country of Residence. |

|

Part II: |

|

|

✓ |

Information of Withholding Agent/Income Payor; |

|

✓ |

Details of Withholding of Tax; |

|

✓ |

Type of Income Earned within the Philippines in Respect to which Relief is claimed; |

|

✓ |

Declaration of Income Recipient/Beneficial Owner; and |

|

✓ |

Declaration of Withholding Agent/ Income Payor. |

8. Transitory provision:

Nonresidents who have filed TTRA prior to this RMO shall be already allowed to use the invoked tax treaty rates.

9. Effectivity:

The RMO shall take effect after 90 days to afford the non-resident income earners time to secure the certification of residency.