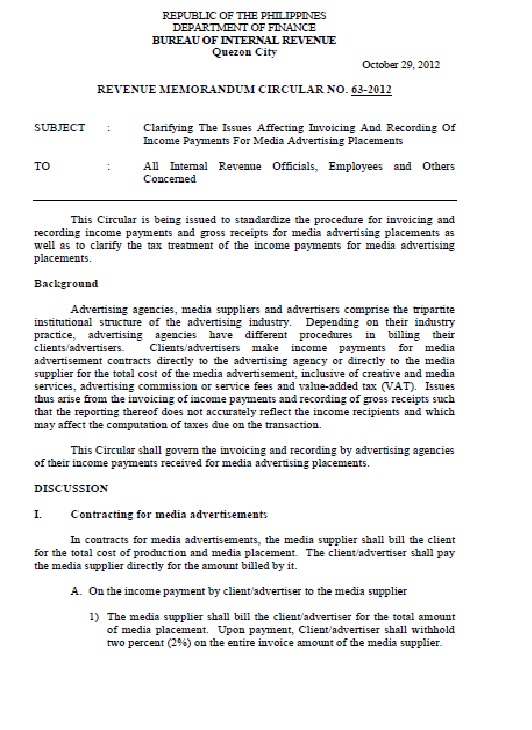

The following procedures should be observed in the invoicing and recording of income payments and gross receipts from media advertising placement involving the advertising agencies, media suppliers and advertisers.

a. Payments to the media supplier for advertising placement – The media supplier shall bill the advertiser for the total cost of media placement. The advertiser shall directly pay the media supplier the amount billed minus the 2% creditable withholding tax, and issue the Certificate of Creditable Tax Withheld as Source (BIR form 2307) in the name of the media supplier. The media supplier, on the other hand, shall issue a VAT official receipt for the full amount and report the same for income tax purposes.

b. Commission/service fee of advertising agency from media suppliers - The advertising agency shall bill the media supplier for its commission/service fee. Upon payment, the media supplier shall withhold the 2% creditable withholding tax from the commission/service fee, and issue the Certificate of Creditable Tax Withheld as Source (BIR form 2307) in the name of the advertising agency. The advertising agency, on the other hand, shall issue a VAT official receipt indicating the 12% VAT on the said commission/service fee.

Illustrative accounting entries in the books of accounts of the advertisers, media entity and advertising agency are provided in RMC 63-2012.

Please see attached copy of RMC 63-2012 below.

.