Implementation of the Amendments introduced by EOPT Act on Tax Refunds

(Revenue Regulations 5-2024, April 11, 2024)

This Tax Alert is issued to inform all concerned on the implementation of the amendments introduced by EOPT Act on the risk-based approach in verifying VAT refund claims, liabilities in case of disallowance by the Commission on Audit (COA), refund of unutilized excess income tax credit in case of dissolution or cessation of business, processing of tax refund, and policies for judicial claims.

VAT Refund Claims under Section 112 (A) of the Tax Code

I. The following rules shall be followed to implement the risk-based approach in verifying VAT refund claims of taxpayers introduced by EOPT Act:

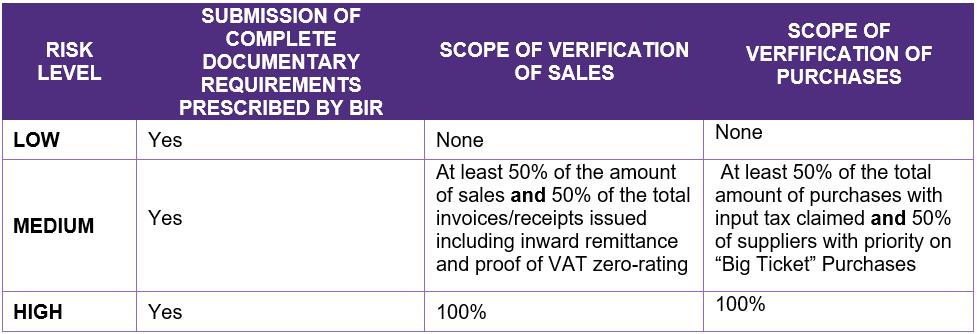

a. Refunds will be classified into low-, medium-, and high-risk claims depending on the amount of VAT refund claim, frequency of VAT refund claims, tax compliance history and other risk factors.

b. The scope of verification in accordance with the identified risks shall be follows:

*Based on initial checking of the documents submitted during check-listing procedures only. This does not include thorough verification of the supporting documents for sales and purchases.

c. Limitations on the classification:

i. Claims filed by first-time claimants shall be automatically considered as high-risk and shall remain as such for the succeeding three (3) VAT refund claims.

ii. In case of full denial of a claim, the succeeding claim filed shall be classified as high-risk.

iii. For medium-risk claims, verification shall be adjusted to 100% if the assigned Revenue Officer found at least 30% disallowance of the amount of VAT refund claim.

iv. Claims classified as low-risk for the three (3) consecutive filing of VAT refund claims shall be subject to mandatory full verification on the fourth (4th) VAT refund claim regardless of the risk classification.

v. VAT credit/refund claims for any unused input tax filed by a VAT-registered person whose registration has been cancelled due to retirement from or cessation of business, or due to changes in or cessation of status shall be classified as high-risk and will require full verification.

vi. Taxpayer-claimants filing on a quarterly basis. The risk classification shall be made for every filing.

Other limitations that may be identified by the Commissioner of Internal Revenue through revenue issuances.

II. Appeal to the Court of Tax Appeals (CTA)

In case of full or partial denial of VAT refund claims, the taxpayer may appeal to the Court of Tax Appeals (CTA) within thirty (30) days from the receipt of the decision denying the claim. However, in case of inaction of the CIR within the 90-day period, the taxpayer has the following options:

a. Appeal to the CTA within the 30-day period after the expiration if the 90 days required by law to process the claim. In such case, the administrative claim for refund shall be considered moot and shall no longer be processed; or

b. Forego the judicial remedy and await the final decision of the Commissioner on the application of VAT refund claim.

III. In case of approval of VAT refund, all documentary requirements will be subject to post-audit by Commission of Audit (COA). In case of disallowance by the COA, only the taxpayer shall be liable for the disallowed amount without prejudice to any administrative liability on the part of any employee of the BIR who may be found to be grossly negligent in the grant of the refund.

Refund of Unutilized Excess Income Tax Credit under Section 76 (C) of the Tax Code

I. Regular Claims of taxpayers of “going-concern” status

a. Requisites for refund:

i. The filing of claim for Tax Credit Certificate (TCC)/refund must be made within two (2) years from the date of filing of the AITR.

ii. Income upon which the taxes were withheld must be included as part of the gross income declared in the income tax return of the recipient.

iii. Fact of withholding is established by a copy of the withholding tax certificate showing the amount of income payment and the amount of tax withheld. The taxpayer-claimant must be clearly identified as the payee in the withholding tax certificate.

b. In case the taxpayer is entitled to a tax credit or refund of the excess income taxes paid during the year, the excess amount shown on its final adjustment return may be carried over and credited against the estimated quarterly income tax liabilities for the taxable quarters of the succeeding taxable years. Once the option to carry-over and apply the said excess income taxes paid against the income tax due for the taxable quarters of the succeeding taxable years has been made, such option shall be considered irrevocable for that taxable period and no application for cash refund or issuance of a tax credit certificate (TCC) shall be allowed therefor.

c. In case the taxpayer chose the option to be issued TCC or refund but carried forward the said amount sought to be refunded/issued TCC in the AITR filed for the succeeding year, this shall be a ground for denial of the claim for tax credit or refund. However, the carried over amount may be allowed as credit against future income tax liabilities of the taxpayer-claimant.

d. From the submission of complete documents, the BIR has 180 days to process and decide on the refund of the excess income tax credit.

II. Claims in case of Dissolution or Cessation of Business

a. As an exception to the irrevocability rule, the taxpayers who chose the option to "carry-over" may claim a refund provided that they have permanently ceased operations as also contemplated under Section 76 (C) of the Tax Code.

b. As an exception to the above 180-day period, the BIR shall decide on the application and refund the excess taxes within two (2) years from the date of the dissolution or cessation of business.

c. The 2-year period to decide and refund the excess taxes shall commence from the submission of the "Application for Registration Information Update/Correction/Cancellation" (BIR Form No. 1905) together with the complete documentary requirements set by the BIR for the closure of business and the refund of excess income taxes due to cessation or dissolution of business under Section 76 of the Tax Code.

d. The approved refund, if any, shall be released only after completion of the mandatory audit of all internal revenue tax liabilities covering the immediately preceding year and the short period return and full settlement of all tax liabilities relative to cessation or dissolution of the business and any existing tax liabilities prior to the cessation or dissolution of the business.

Refund of erroneously received or collected taxes or penalty under Sections 204 (C) and 229 of the Tax Code

I. Requisites for the claims of tax credit/refund of erroneously received or collected taxes or penalty:

a. The tax credit/refund claim pertains to erroneously or illegally received or collected taxes or penalties imposed without authority.

b. Filing of the claim must be done within two (2) years after payment of the tax or penalty.

c. The erroneously or illegally received or collected taxes must be supported with a copy of the duly filed tax return with the corresponding payment remitted to the BIR.

II. The return filed showing an overpayment shall be considered as a written claim for credit/refund. From the time of submission of complete documents, the BIR has 180 days to process and decide the tax refund. The 180 days shall be from the date of submission of complete documents in support of the application as prescribed by the BIR up to the payment of the approved refund or receipt of the TCC.

III. In case of full or partial denial of the refund claims, the taxpayer may appeal to the Court of Tax Appeals (CTA) within thirty (30) days from the receipt of the decision denying the claim. However, in case of inaction of the CIR within the 180-day period, the taxpayer has the following options:

a. Appeal to the CTA within the 30-day period after the expiration if the 180 days required by law to process the claim. In such case, the administrative claim for refund shall be considered moot and shall no longer be processed; or

b. Forego the judicial remedy and await the final decision of the Commissioner on the application of refund claim.

Effectivity

RR No. 5-2024 shall cover tax credit/refund claims that are filed beginning July 1, 2024 onwards.