(Revenue Memorandum Circular No. 80-2023, August 9, 2023)

This Tax Alert is issued to inform all concerned on the clarifications on the provisions of Revenue Regulations (RR) No. 3-2023 and certain issues and concerns pertaining to transactions with other entities granted with VAT zero-rate incentives on local purchases under special laws and international agreements.

A. Registered Export Enterprises (REEs)

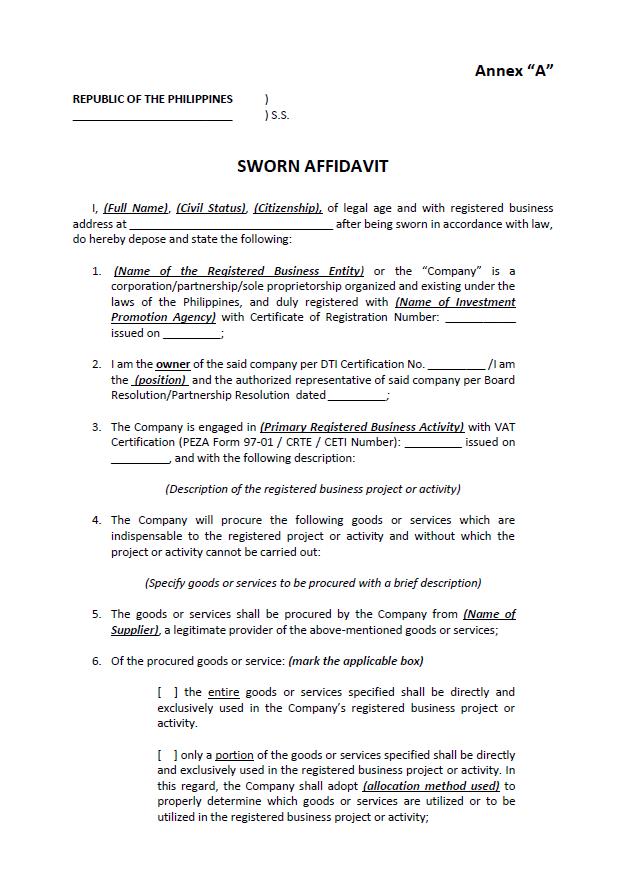

Upon the effectivity of RR No. 3-2023 last April 28, 2023, local supplier of goods and/or services of REEs shall no longer be required to apply for approval of VAT zero-rate with the BIR. Instead, the VAT Zero-Rate Certification issued by the concerned Investment Promotion Agency (IPA) shall be the basis for the VAT zero-rating. The goods and/or services directly and exclusively attributable to the registered project or activity of the REE should be enumerated in Section III, Annex "A" of the prescribed Template for VAT Zero-Rate Certification per RMC No. 36-2022. The said goods and/or services must likewise be declared in the REE's sworn undertaking.

The following documents must be provided by the REE-buyers to its local suppliers for the latter's documentation in case of post-audit by the BIR:

For applications for VAT zero-rating which are pending approval as of the effectivity date of RR No. 3-2023, the transactions covered by the application shall be accorded VAT zero-rating treatment from the date of filing of such application subject to the conduct of post audit by the BIR that the services are indeed directly and exclusively used by the REE in its registered project or activity.

If the transaction was entitled to VAT zero-rating, i.e., the goods and/or services sold were directly and exclusively used in the registered project or activity, and the REE is duly endorsed by the concerned IPA, but the seller failed to secure an approved Application or failed to file an application for VAT Zero-Rate prior to the effectivity of RMC 3-2023, such sale shall be subject to twelve percent (12%) VAT. Likewise, if there was already a prior determination by the BIR that the transaction is not qualified for VAT zero-rate, it will also be subject to 12% VAT.

The VAT-registered REE enjoying 5% Gross Income Tax (GIT) or Special Corporate Income Tax (SCIT) may claim the corresponding input VAT from the said purchase, as either deduction against future output VAT liability after the incentive period or may be claimed as VAT refund under Section 112 (B) of the National Internal Revenue Code of 1997, as amended (Tax Code).

In case of post audit by the BIR, the following must be considered in the evaluation of transaction subject for VAT zero-rate:

B. Enterprises granted VAT Zero-rate incentives under Special Laws or International Agreements

Local suppliers of goods and/or services of other entities granted with VAT zero-rate incentives under special laws and international agreements shall also no longer apply for approval of VAT zero-rate with the BIR. Rather, it will need to secure the following documentary requirements from the buyer:

A. For the Supplier of RE Developer

B. For the Supplier of Other Entities under Special Law and International Agreements

In case of post audit by the BIR, the following must be considered in the evaluation of transaction subject for VAT zero-rate: