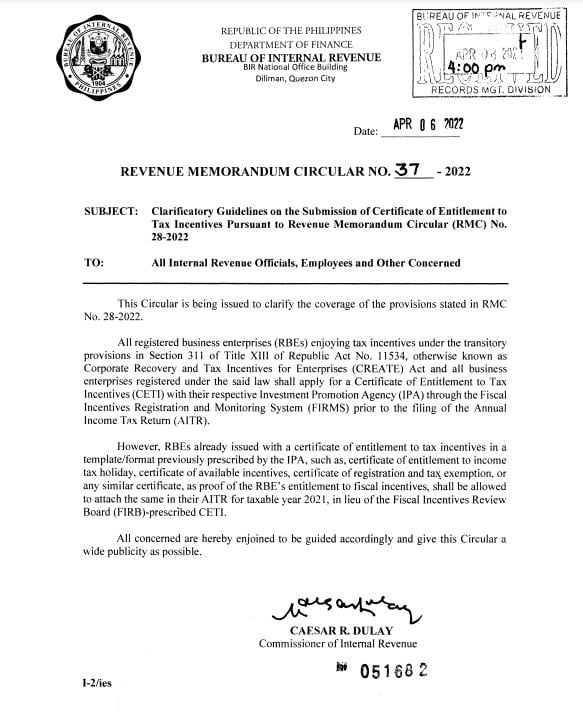

(Revenue Memorandum Circular No. 37-2022 issued on April 06, 2022)

This Tax Alert is issued to inform all concerned on the clarificatory guidelines on the submission of Certificate of Entitlement to Tax Incentives (CETI) as an attachment to the Annual Income Tax Return (AITR) of a Registered Business Enterprise (RBE) to the Bureau of Internal Revenue (BIR).

All RBEs enjoying tax incentives under the transitory period of CREATE Act and those registered under the said law shall apply for a Certificate of Entitlement to Tax Incentives (CETI) with their respective Investment Promotion Agency (IPA) through the Fiscal Incentives Registration and Monitoring System (FIRMS) prior to the filing of the AITR.

However, RBEs already issued with a certificate of entitlement to tax incentives in a template/format previously prescribed by the IPA, as proof of the RBE's entitlement to fiscal incentives, shall be allowed to attach the same in their AITR for taxable year 2021, in lieu of the Fiscal Incentives Review Board (FIRB)-prescribed CETI.

.