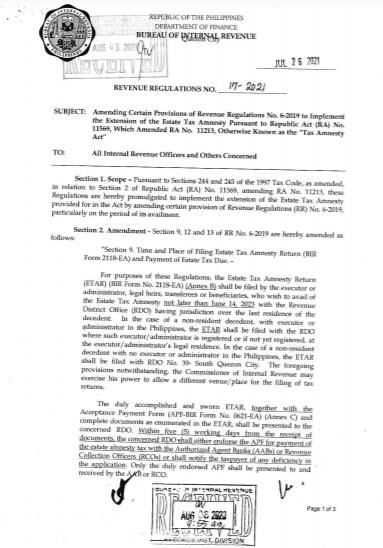

(Revenue Regulations No. 17-2021 issued on August 4, 2021)

This Tax Alert is issued to inform all concerned on the extension of the availment period of Estate Tax Amnesty under Republic Act (RA) No. 11569 and certain amendments/clarifications on the process of availment of estate tax amnesty.

The period of availment of Estate Tax Amnesty is extended until June 14, 2023 pursuant to RA No. 11569, amending RA No. 11213.

Duly accomplished and sworn Estate Tax Amnesty Return (ETAR) and Acceptance Payment Form (APF) with proof of payment, together with the complete documentary requirements, shall be submitted to the RDO in triplicate copies. Failure to submit the same until June 14, 2023 is tantamount to non-availment of the Estate Tax Amnesty.

The following amendments/clarifications to the existing rules on availment of Estate Tax Amnesty are also provided by the BIR:

- Within five (5) working days from receipt of ETAR, APF and other required documents, the concerned RDO shall endorse the APF for payment with the Authorized Agent Banks (AABs) or Revenue Collection Officers (RCOs). Only these duly endorsed APF shall be presented to and received by the AAB or RCO.

- Proof of settlement of the estate, whether judicial or extra-judicial, is not required in filing of the ETAR if it is not yet available at the time of filing. However, no electronic Certificate Authorizing Registration (eCAR) shall be issued unless such proof is presented and submitted to the concerned RDO.

- One eCAR shall be issued per real property until such time that the eCAR system is already capable of generating one (1) eCAR for all properties covered by a single transaction.

- eCAR shall only be issued upon submission of the proof of estate settlement (e.g., Extra-Judicial Settlement of Estate (EJS), Copy of Court Order). If these documents include properties not indicated in the filed ETAR, the particular properties shall be excluded from the eCAR, unless additional estate tax amnesty payment shall be made within the amnesty period. Otherwise, the additional estate tax to be paid for the additional properties indicated in the EJS or Court Order shall be subject to applicable estate tax rate including interests and penalties.

All other existing rules and revenue issuances to implement and clarify the availment of Estate Tax Amnesty under RA No. 11213 shall continue to apply to the period of extension for availment of Estate Tax Amnesty under RA No. 11569.