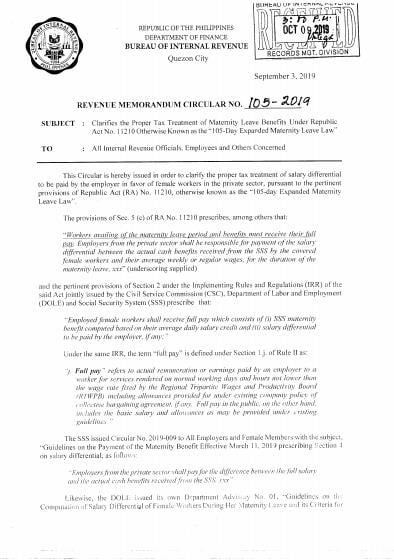

(Revenue Memorandum Circular No. 105-2019)

This Tax Alert is issued to inform all concerned on the clarification on the proper tax treatment of maternity leave benefits, particularly the salary differential paid by the employer, under Republic Act No. 11210 or the 105-Day Expanded Maternity Leave Law.

Pursuant to Section 5 (c) of Republic Act (RA) No. 11210 and its Implementing Rules and Regulations (IRR), employed female workers availing of the maternity leave benefits shall receive their full pay for the duration of the maternity leave which consists of (1) the Social Security System (SSS) maternity benefit computed based on the average daily salary credit and (2) salary differential to be paid by the employer.

With these new provisions in the law, the Bureau of Internal Revenue (BIR) interpreted that the salary differential is now considered as benefit under the Social Security Law. Based on the provisions of RA No. 11210 and its IRR, the previous 100% of the average daily salary credit was expanded to a full pay, which now includes the salary differential as its component.

Therefore, the payment of the expanded maternity benefit which includes the SSS maternity benefit and the salary differential is not subject to withholding tax on compensation pursuant to Section 2.78.1(B)(1)(e) of Revenue Regulations (RR) No. 02-98, as amended, which provides that the payments of benefits made under Social Security Act of 1954 shall be exempt from withholding tax.

.