This Tax Alert is issued to inform all concerned on the prescribed VAT treatment of government projects funded by the OECF.

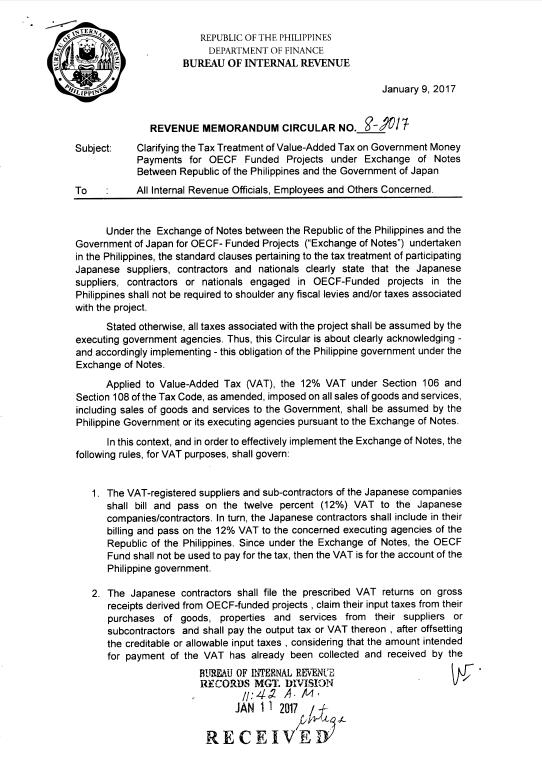

Under the Exchange of Notes between the Philippines and Japan on Overseas Economic Cooperation Fund (OECF)-funded projects, all taxes associated with the project shall be assumed by the executing government agencies. This shall be implemented as follows:

In RMC 45-2015 which was amended, the Japanese contractor does not charge 12% VAT on the government agency. The government agency, on the other hand, remits to BIR, from its own funds, the 5% withholding VAT.

You may access a copy of the RMC at the P&A Grant Thornton website through the link below.