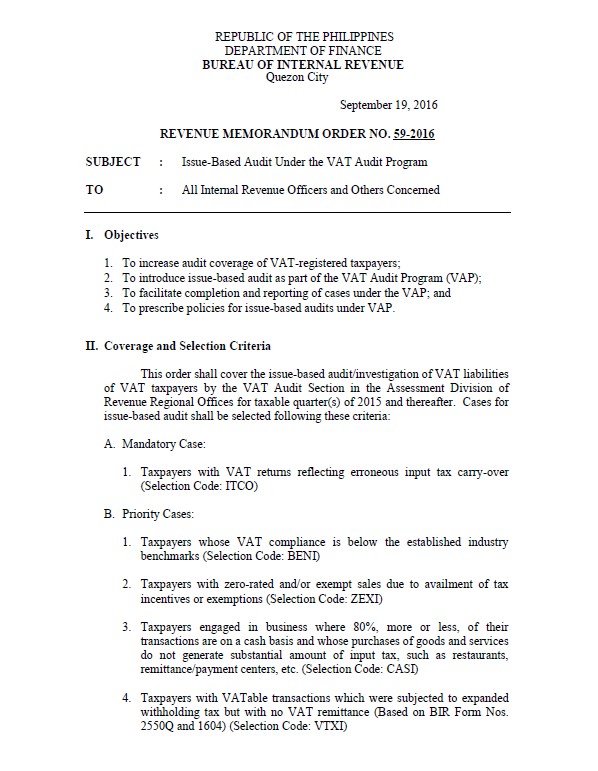

(Revenue Memorandum Order No. 59-2016)

Under the VAT audit program of the BIR for 2015 and thereafter, taxpayers will be selected based on two sets of criteria.

Taxpayers that will be subject to the regular VAT audit will be selected based on the criteria under RMO 20-2012.

On the other hand, taxpayers shall be selected for issue-based VAT audit based on the following criteria under RMO 59-2016:

A. Mandatory Case:

B. Priority Cases:

For the issue-based VAT audit, one eLA shall be issued for each taxable quarter, or for two quarter if recommended by the VAT Audit Section Chief. If taxpayer is also selected for regular audit, the eLA shall exclude the VAT liability. The Audit Information Tax Exemption and Incentives Division (AITEID) at the National Office shall automatically provide the VAT Audit Sections the preprocessed RELIEF data for the selected taxpayers.

The taxpayer shall be given 10 days from receipt of Notice to present the required documents. A reminder letter shall be send before a Subpoena Dices Tecum is issued. No extension shall be allowed.

Revenue officers shall submit their reports within 60 or 90 days from issuance of eLAs covering one or two quarters, respectively. The PAN and FAN will be issued pursuant to existing regulations.

.