(Revenue Memorandum Order No. 64-2016, November 15, 2016)

This Tax Alert is issued to inform all concerned on the latest amendments in the policies and procedures to implement the BIR audit program.

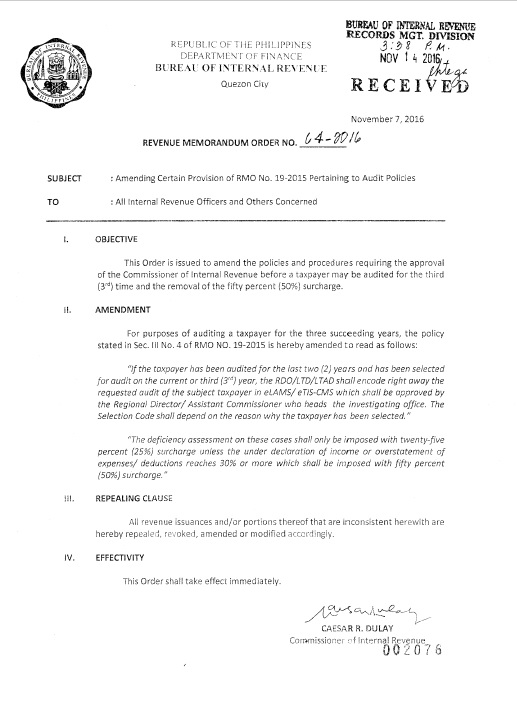

Under RMO 19-2015, if a taxpayer has been selected for audit for the third consecutive year, the RDO/LTD/LTAD has to submit a written justification to the Commissioner, unless it has been established that the taxpayer has underdeclartion/overdeclaration of income/expense by at least 30%. The deficiency assessment shall be subject to 50% surcharge.

Under RMO 64-2016, the surcharge for deficiency assessment is lowered to 25%. The 50% surcharge shall apply only if there is underdeclaration of income or overstatement of expenses/deductions reaching 30%.The RDO/LTD/LTAD can now directly encode the requested audit in eLAMS/eTIS-CMS to be approved by the regional director/assistant commissioner (previously, by the Commissioner).

Selection code shall depend on the reason by the taxpayer has been selected.

.