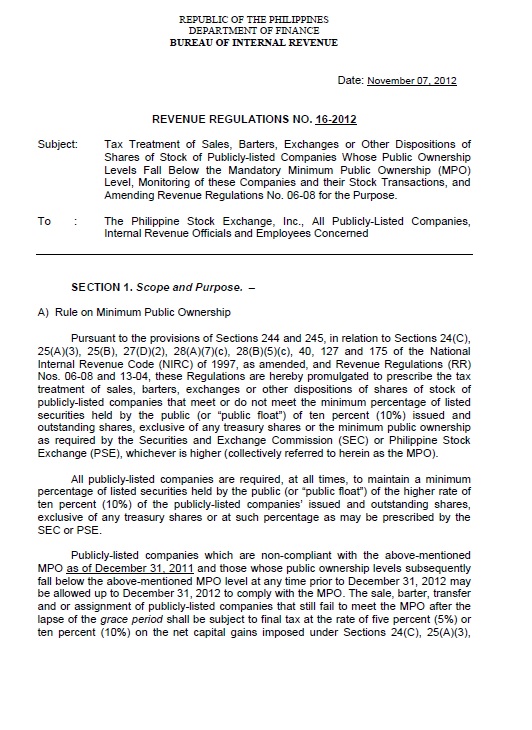

All publicly-listed companies must have at least 10% public float or the minimum public ownership (MPO) as required by the Securities and Exchange Commission or Philippine Stock Exchange, whichever is higher, to enjoy the preferential tax rate of one half of one percent tax on gross selling price on sale of stocks listed and traded through the local stock exchange under Section 127(A) of the Tax Code.

Publicly-listed companies which are non-compliant with the above percentages may be allowed up to December 31, 2012 to comply with the MPO.

Transactions up to December 31, 2012 of publicly-listed companies which fail to meet the MPO shall be subject to ½ of 1% tax on gross selling price under Section 127(A) of the Tax Code while transactions made after December 31, 2012 shall be subject to a final tax of 5% or 10% on the net capital gains imposed on sales of shares of stocks not traded in the local stock exchange. The transfer of shares of stocks of non-compliant publicly-listed companies on their transactions after December 31, 2012 shall be subject to DST imposed under Section 175 of the Tax Code.

No sale, exchange, or transfer of shares of stock shall be registered in the books of the corporation unless the receipts of payment of the taxes and the Certificate Authorizing Registration (CAR) and/or Tax Clearance Certificate are filed with, and recorded by the stock transfer agent or secretary of the corporation.

Please see attached copy of RR 16-2012.