Accounting Alerts

- 2024

- 2023

- 2022

- 2021

-

2020

2020

- Extension of Deadline for Submission of Forms/Notices

- Online and Manual Submission of Forms/Notices Pursuant to SEC MC 28-2020

- COVID-19 Accounting Implications for CFOs - Debt Modifications

- Discussion Paper 'Business Combination under Common Control'

- SEC Memorandum Circular No. 32 series of 2020

- SEC Memorandum Circular No. 31 series of 2020

- SEC Memorandum Circular No. 28 series of 2020

- Insights into PFRS 16 - Lease Incentives

- IASB issues Interest Rate Benchmark Reform Phase 2

- IFRIC 23 - Uncertainty Over Income Tax Treatments

- COVID-19 Going Concern Considerations

- Extension of Deadlines and Interim Procedures for the Submission of Printed/Hard Copies of Annual Reports

- IASB Defers the Effective Date of IAS 1 Amendments

- Guidelines on the Electronic Submission of the Annual Report and Audited Financial Statements to BSP

- Filing of Annual Reports During the Temporary Closure of the SEC Main Office until July 26, 2020

- Work Suspension at the SEC Main Office and Extension of Deadlines for Certain Corporations

- Adjustment of Deadlines for Submission of Annual Reports to the SEC and Other Announcements

- Amendments to IFRS 17 and IFRS 4

- Filing of Reports and Other Documents in SEC Main Office during Temporary Closure

- Options for the Submission of Reports, Applications and Other Documents to the SEC During Community Quarantine

-

2019

2019

- SEC Extends Deadline for Annual and Quarterly Reports for...

- Deferral of IFRIC Agenda Decision on Over Time Transfer of Constructed Goods (PAS 23) for Real Estate Industry

- Implementation of IFRS 17, Insurance Contracts

- Amendments to Regulations on Financial Audit of Banks and Non-Bank Financial Institutions

- Navigating the Changes to IFRS 2020

- SEC Memorandum Circular No. 2 - 2020 Filing of Annual Financial Statements and General Information Sheet

- IASB issues Classification of Liabilities as Current or Non-current (Amendments to IAS 1)

- GTI IFRS News Q4 2019

- Insights into PFRS 3: Definition of a Business

- IASB issues Interest Rate Benchmark Reform

- Insights into PFRS 16: Presentation and Disclosure

- Insights into PFRS 16: Lease Payments

- Insurance Commission's Guidelines on Lease Accounting for Insurance and Reinsurance Companies

- GTI IFRS News Q1 2019

- Application Deferral of PIC Q&A 2018-H and 2018-14

- Sustainability Reporting Guidelines for Publicly-Listed Companies

- Insights into PFRS 16: Sale and Leaseback Accounting

- Insights into PFRS 16: Transition Choices

- Use of the New General Information Sheet (GIS) Form

- 2019 Filing of Annual FS and GIS

- Navigating the Changes to IFRS 18

- Insights into PFRS 3: Definition of a Business

- GTI IFRS News Q2 2019

- Rules on Material Related Party Transactions for Publicly-listed Companies

- BOA Repealed Resolutions on FS Compilation Services

- GTI IFRS News Q3 2019

- 2019

- 2018 2018

- 2017

- 2016

- 2015

- 2014

- 2008

- 2007

- 2006

- 2005

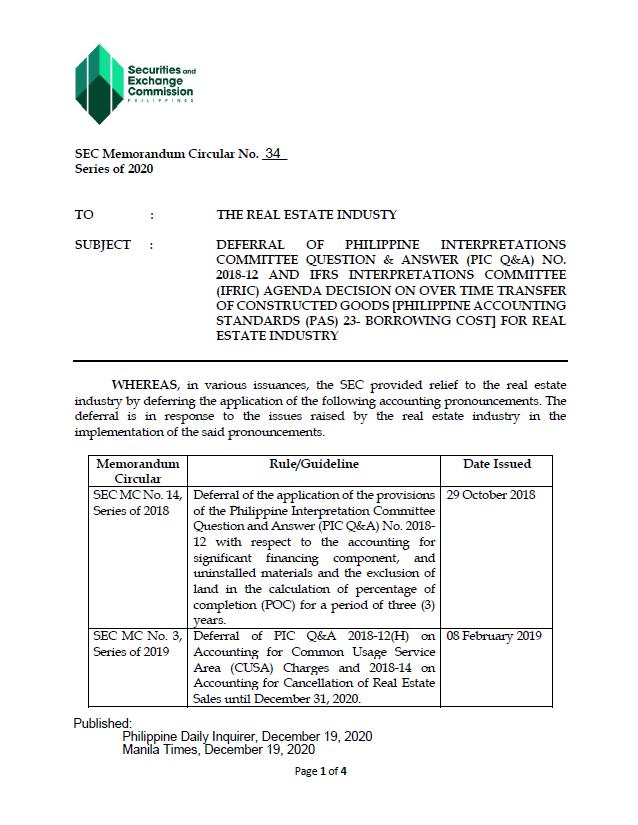

SEC Memorandum Circular No. 34 series of 2020

This Accounting Alert is issued to circulate Securities and Exchange Commission (SEC/Commission) Memorandum Circular (MC) No. 34-2020 dated December 15, 2020 on the deferral of certain unresolved provisions of Philippine Interpretations Committee Question & Answer (PIC Q&A) No. 2018-12 and IFRS Interpretations Committee (IFRIC) Agenda Decision on Over Time Transfer of Constructed Goods for Real Estate Industry.

Overview

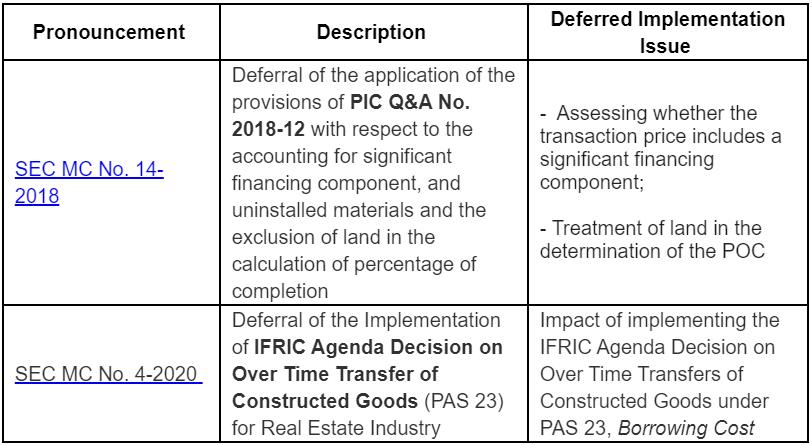

The Commission en banc, on its meeting held on December 15, 2020, decided to provide relief to the real estate industry by further deferring the application of the following unresolved implementation issues of PIC Q&A No. 2018-12 and IFRIC Agenda Decision on Over Time Transfer of Constructed Goods, for another period of three years or until 2023:

The deferral is in response to the request of the real estate industry for an additional period of deferral to afford the industry reasonable time to further evaluate the impact of several remaining items in the implementation of the above pronouncements.

Option Not to Avail

A real estate company may opt not to avail of any of the relief provided above and, therefore, will comply in full with the requirements of PIC Q&A 2018-12 and IFRIC Agenda Decision in respect of the relief not availed of.

Disclosure Requirements in the Financial Statements

The above regulatory relief, once adopted and recorded for financial reporting purposes, is not considered in accordance with Philippine Financial Reporting Standards (PFRS). Thus, real estate companies which opt to avail of the deferral shall specify in the Basis of Preparation of the Financial Statements section of the financial statements the following:

- the relief availed of; and,

- the indication that the financial statements are prepared in accordance with PFRS, as modified by the application of the availed financial reporting reliefs.

For consistency of presentation, real estate companies should comply with the following prescribed wordings:

“The accompanying financial statements have been prepared in accordance with Philippine Financial Reporting Standards, as modified by the application of the following financial reporting reliefs issued and approved by the Securities and Exchange Commission in response to the COVID-19 pandemic: (enumerate reliefs availed of).”

Real estate companies, which opted for the deferral, shall also be required to disclose in the notes to the financial statements:

- the accounting policies applied;

- a discussion of the deferral of the subject implementation issues in the PIC Q&A; and,

- a qualitative discussion of the impact in the financial statements had the concerned application guidelines been adopted.

Should any of the deferral options result in an accounting policy change, such accounting change will have to be accounted for under PAS 8, Accounting Policies, Changes in Accounting Estimates and Errors, i.e., retrospectively, together with the corresponding required quantitative disclosures.

Effects on the Independent Auditor's Opinion

The external auditor shall reflect in the opinion paragraph that the financial statements are prepared in accordance with PFRS, as modified by the application of the above financial reporting reliefs issued and approved by the SEC. In addition, the external auditor shall include an Emphasis of Matter paragraph in the auditor’s report to draw attention to the basis of accounting that has been used in the preparation of the financial statements.

See attached Accounting Alert for further details.

.

SEC Memorandum Circular No. 34 series of 2020