Another year is dawning, and the countdown has begun. As the days go by and we take the first step in faith towards the new year, we hope everyone can reflect and truly say that it was indeed a year of intense growth. Since I am a believer that the new year is neither an end nor a beginning but a going-on, I wish to take everyone back and recall the previous Let’s Talk Transfer Pricing (TP) articles that were published throughout the year so we may welcome 2023 with proper guidance.

To name a few, we started 2022 with our first article entitled “Are your related party transactions at arm's length?” followed by other monthly installments such as “Transfer pricing policies are a must-have", “How FAR are you in transfer pricing documentation?”, “Fundamentals of entity characterization in TPD”, “What’s #TRENDING? Understanding and documenting industry analysis”, and most recently “Understanding transfer pricing methodologies”.

Before 2022 ends, our last Let’s Talk TP article of the year is about the concept of profit level indicator (PLI) in transfer pricing documentation (TPD) as discussed in Revenue Regulations (RR) No. 2-2013 and Revenue Audit Memorandum Order (RAMO) No. 1-2019.

What is PLI?

PLI is the ratio of net profit to an appropriate base (e.g., sales, costs incurred, assets employed). It measures the relationship between the net profits and the appropriate base.

Examples of PLI are return on sales (gross margin or operating margin), return on costs, and return on capital.

Where is PLI used in TPD?

The discussion and selection of an appropriate PLI is presented in the “Application of the transfer pricing method” or “Benchmarking” section of the TPD.

In applying the transfer pricing method, consideration must be given to the choice of PLI. The use of an appropriate PLI ensures better accuracy in the determination of the arm’s length price of a related party transaction.

The Resale Price Method (RPM), Cost Plus Method (CPM) and Transactional Net Margin Method (TNMM) are the transfer pricing methods that use PLI to determine whether the related party transaction involved is carried out at arm’s length.

How do we select an appropriate PLI?

The selection of an appropriate PLI depends on the facts and circumstances of the related party transaction involved. Factors to consider include but are not limited to: (1) characterization of business; (2) availability of comparable data; and (3) the extent to which the PLI is likely to produce a reliable measure of arm’s length profit.

In determining the numerator and denominator of the PLI, taxpayers should bear the following principles in mind: (a) only those items that are directly or indirectly related to the related party transaction involved and are of an operating nature should be considered; and (b) items that are not similar to the independent party transaction being compared should be excluded.

Further, the determination of the denominator used in PLI is done by considering the company's profit drivers and their independence from the denominator that is used. Other factors that need to be considered in selecting the PLI are the type of business and the availability of data.

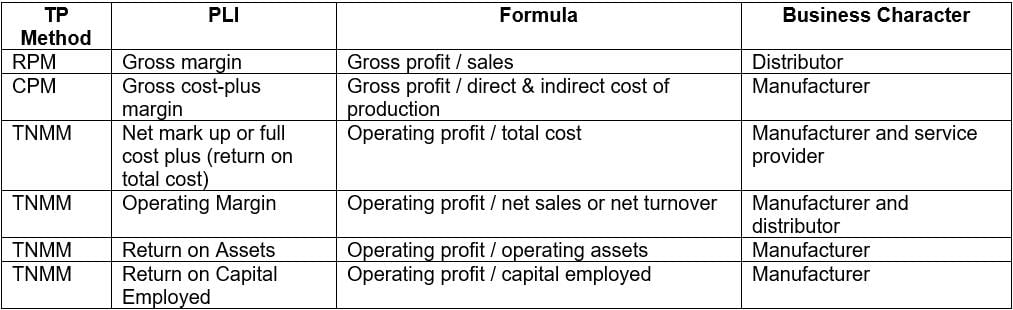

What are the generally used PLIs?

While PLI differs from case to case depending on the characterization of the business, among others, presented below are the generally used PLIs.

![]()

Business characterization is important because by determining the accurate characteristics of the entity’s business, the expected level of price or return by the entity can be known and the selection of reliable comparable can be made.

How is PLI applied?

A benchmarking study or comparable analysis is conducted to find comparable independent transactions or companies to verify the arm's length nature of the related party transactions under evaluation.

a. Search for comparable

In searching for comparable independent transactions or companies, commercial databases are advisable to generate reliable comparable. The data obtained from the commercial database only constitutes candidate comparable. The candidate comparable must undergo manual selection process (i.e., General and Financial Review) mentioned in RAMO No. 1-2019 to be able to produce the list of final comparable.

b. Use of multiple year data

Then, the chosen appropriate PLI of the final comparable is computed. Multiple-year data or PLI (usually 3 years) rather than single-year data improves the reliability of the analysis. The inclusion of numerous years of data makes it easier to pinpoint variables that may have influenced or should have influenced transfer prices, like long-term arrangements and business or product life cycles which may also need to be considered when determining comparability. Further, the use of multiple year data would help neutralize the impact of extreme data points, like abnormally high profits or abnormal losses, while at the same time ensuring that the arm’s length range/ price is representative of the data points identified.

c. Use of interquartile range

In some cases, it will be possible to apply the arm's length principle to arrive at a single figure of PLI that is the most reliable to establish whether the conditions of a transaction are at arm's length. However, because transfer pricing is not an exact science, there will be many occasions when the application of the most appropriate method produces a range of figures all of which are equally reliable. This is often the case in practice where the comparable is extracted from a commercial database. In such cases, if the range includes many observations, statistical tools that account for central tendency to narrow the range (e.g., the interquartile range or other percentiles) might help enhance the analysis's reliability.

d. Benchmarking

The PLI of the tested party or related party transaction involved is compared with the interquartile range of PLIs of the comparable.

If the PLI of the tested party is within the arm’s length range, the related party transaction is carried out at arm’s length basis hence, there would be no adjustment to be made by the tax authority in case of audit.

However, if the PLI of the tested party falls outside the arm's length range, the tested party must be able to present justifiable commercial reasons that the conditions of the related party transaction satisfy the arm's length principle. But if the tested party is unable to establish this fact, the related party transaction is not carried at arm’s length basis hence, the tax authority would make adjustments and determine the point within the arm's length range to which it will adjust the conditions of the related party transaction.

Takeaway

Much like how life is about the choices we make and how the direction of our lives comes down to the choices we take, the use of an appropriate PLI grants taxpayers relief from questioning by tax authorities. Good life choices help us build healthy relationships and reliable PLI ensures better accuracy in the determination of the arm’s length price of a controlled transaction. As we welcome the new year, may we all start doing our best to make decisions that matter, both in life and in choosing the appropriate PLI.

Happy new year and we hope everyone makes the conscious choice of staying tuned in for next month’s Let’s Talk TP article as we walk you through the remaining concepts of transfer pricing.

Let's Talk TP is an offshoot of Let’s Talk Tax, a weekly newspaper column of P&A Grant Thornton that aims to keep the public informed of various developments in taxation. This article is not intended to be a substitute for competent professional advice.

As published in BusinessWorld, dated 27 December 2022