2015

.

.

.

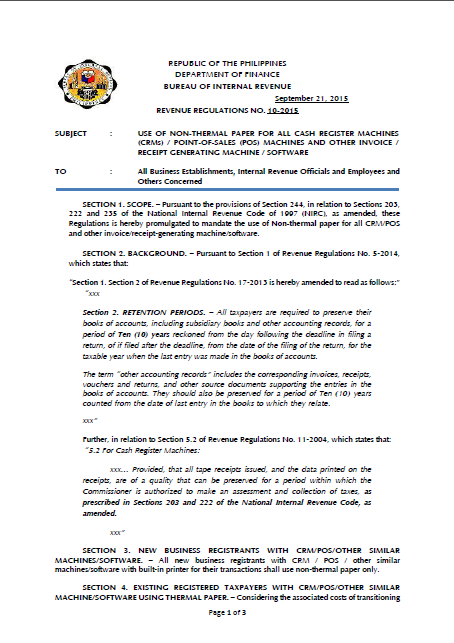

In Revenue Regulations No. 10-2015, the BIR prescribed an expanded list of information to be indicated in the receipts/invoices issued form CRM/POS machines as well as electronic receipts issued from a network or linked to CAS or components. The required information include:

a. a space for the name address, TIN and business style of the buyer/customer;

b. information about the BIR-accredited supplier of CRM/POS machine/software and the BIR Final Permit to Use, at the bottom portion of the receipt; and

c. Senior Citizen/PWD TIN, discount and signature, in case taxpayer is required to provide discounts to SC/PWD.

Clarifications

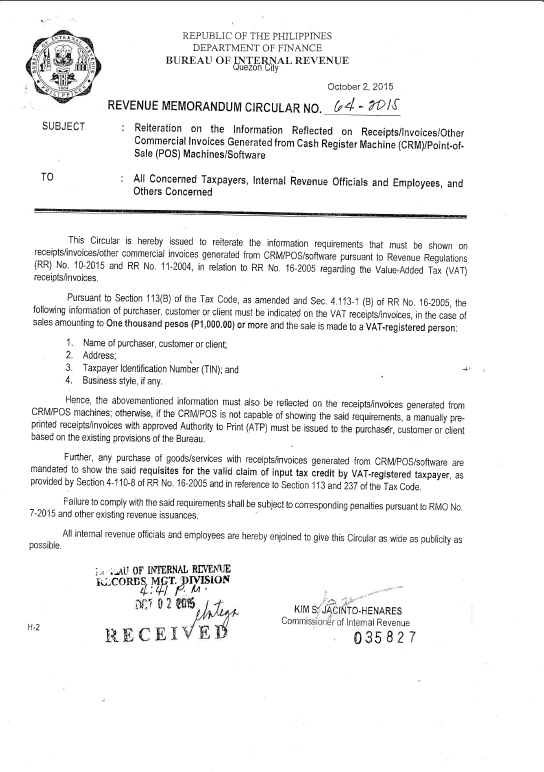

In RMC 64, the BIR reiterated and clarified the following existing rules:

1. Only sales made to VAT-registered persons amounting to at least P1,000 are required to have the name, address, TIN and business style of the buyer/customer indicated in the VAT receipts/invoices. Hence, receipts/invoices issued from CRM/POS machines issued to non-VAT buyers as well as on sales of less than P1,000 to VAT-registered buyers are still not required to indicate the information about the buyer/customer.

2. If the CRM/POS machine is not capable of showing such details about the buyer, a manually pre-printed receipt/invoice with approved Authority to Print (ATP) must be issued to the buyer/customer based on the existing regulations of the Bureau.

3. Receipts/Invoices generated from CRM/POS machines/software are mandated to show the said requisites for the valid claim of input tax credits by the VAT-registered buyer.

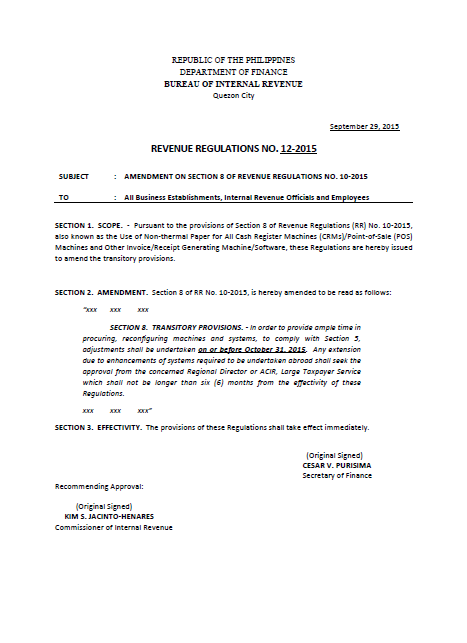

Extended deadline

In order to provide ample time in procuring, reconfiguring machines and systems, the deadline for compliance has been extended to October 31, 2015.

You may access the pertinent RR Nos. 10 and 12- 2015, and RMC No. 64-2015 through the link below.

.

.

.