Accounting Alerts

- 2024

- 2023

- 2022

- 2021

-

2020

2020

- Extension of Deadline for Submission of Forms/Notices

- Online and Manual Submission of Forms/Notices Pursuant to SEC MC 28-2020

- COVID-19 Accounting Implications for CFOs - Debt Modifications

- Discussion Paper 'Business Combination under Common Control'

- SEC Memorandum Circular No. 32 series of 2020

- SEC Memorandum Circular No. 31 series of 2020

- SEC Memorandum Circular No. 28 series of 2020

- Insights into PFRS 16 - Lease Incentives

- IASB issues Interest Rate Benchmark Reform Phase 2

- IFRIC 23 - Uncertainty Over Income Tax Treatments

- COVID-19 Going Concern Considerations

- Extension of Deadlines and Interim Procedures for the Submission of Printed/Hard Copies of Annual Reports

- IASB Defers the Effective Date of IAS 1 Amendments

- Guidelines on the Electronic Submission of the Annual Report and Audited Financial Statements to BSP

- Filing of Annual Reports During the Temporary Closure of the SEC Main Office until July 26, 2020

- Work Suspension at the SEC Main Office and Extension of Deadlines for Certain Corporations

- Adjustment of Deadlines for Submission of Annual Reports to the SEC and Other Announcements

- Amendments to IFRS 17 and IFRS 4

- Filing of Reports and Other Documents in SEC Main Office during Temporary Closure

- Options for the Submission of Reports, Applications and Other Documents to the SEC During Community Quarantine

-

2019

2019

- SEC Extends Deadline for Annual and Quarterly Reports for...

- Deferral of IFRIC Agenda Decision on Over Time Transfer of Constructed Goods (PAS 23) for Real Estate Industry

- Implementation of IFRS 17, Insurance Contracts

- Amendments to Regulations on Financial Audit of Banks and Non-Bank Financial Institutions

- Navigating the Changes to IFRS 2020

- SEC Memorandum Circular No. 2 - 2020 Filing of Annual Financial Statements and General Information Sheet

- IASB issues Classification of Liabilities as Current or Non-current (Amendments to IAS 1)

- GTI IFRS News Q4 2019

- Insights into PFRS 3: Definition of a Business

- IASB issues Interest Rate Benchmark Reform

- Insights into PFRS 16: Presentation and Disclosure

- Insights into PFRS 16: Lease Payments

- Insurance Commission's Guidelines on Lease Accounting for Insurance and Reinsurance Companies

- GTI IFRS News Q1 2019

- Application Deferral of PIC Q&A 2018-H and 2018-14

- Sustainability Reporting Guidelines for Publicly-Listed Companies

- Insights into PFRS 16: Sale and Leaseback Accounting

- Insights into PFRS 16: Transition Choices

- Use of the New General Information Sheet (GIS) Form

- 2019 Filing of Annual FS and GIS

- Navigating the Changes to IFRS 18

- Insights into PFRS 3: Definition of a Business

- GTI IFRS News Q2 2019

- Rules on Material Related Party Transactions for Publicly-listed Companies

- BOA Repealed Resolutions on FS Compilation Services

- GTI IFRS News Q3 2019

- 2019

- 2018 2018

- 2017

- 2016

- 2015

- 2014

- 2008

- 2007

- 2006

- 2005

SEC MC No. 2-2023: Grant of Amnesty for Non-Filing and Late Filing of GIS and AFS, and Non-Compliance with Memorandum Circular No. 28, S. 2020

This Accounting Alert is issued to circulate Securities and Exchange Commission (SEC or the Commission) Memorandum Circular No 02 (MC/the Circular) series of 2023 dated March 16, 2023.

The Securities and Exchange Commission, in its Memorandum Circular Letter No. 2023-2 dated 16 March 2023, released guidelines in granting of amnesty for non-filing and late filing of GIS and AFS and Non-compliance with SEC MC. No. 28, S. 2020, Schedules for Filing of Annual Financial Statements and General Information Sheet.

Covered Violations

Unless otherwise provided under Section 5 of this Circular, an amnesty on the unassessed (not yet assessed) and/or uncollected fines and penalties by the Commission (already assessed not yet paid) is hereby authorized to be granted to all corporations, including branch offices, representative offices, regional headquarters, and regional operating headquarters of foreign corporation and foundations, for the following violations:

a. Non-filing of GIS for the latest and prior years;

b. Late filing of GIS for the latest and prior years;

c. Non-filing of AFS, including fines for its attachments (i.e., Certificate of Existence of Program/Activity, Non Stock, Non-Profit Organization Forms), for the latest and prior years; and,

d. Late filing of AFS, including fines for its attachments (i.e., Certificate of Existence of Program/Activity, Non Stock, Non-Profit Organization Forms), for the latest and prior years.

In addition to corporations, this shall also cover associations, partnerships, and persons under the jurisdiction and supervision or the Commission, that failed to comply with MC No. 28-2020.

Amnesty Rates

The applicable rates under this Circular will be as follows:

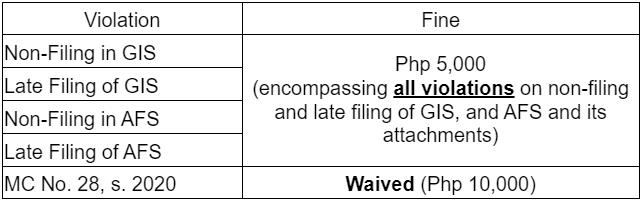

A. Non-Filing and Late Filing of GIS and/or AFS, and MC No. 28 violation:

The foregoing rate will apply, provided that, the applicant corporation or entity will (i) submit the latest reportorial requirements due at the time of application; and (ii) comply with MC No. 28, S.2020 through the MC28 Submission Portal.

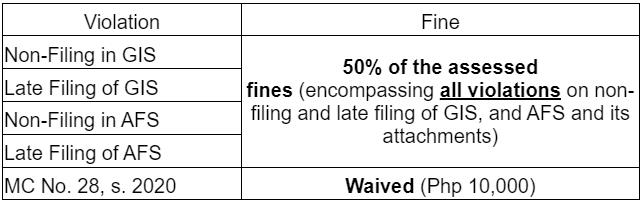

B. Suspended and Revoked Corporations:

The foregoing rate will apply, subject to the payment of filing/petition fee and the appropriate proceedings to be filed with the Company Registration and Monitoring Department (CRMD) and Extension Offices (EOs) and compliance with the requirements under Secfion 3 of this Circular.

Filing of Application and Supporting Documents

On or before 30 April 2023, the duly authorized representative or resident agent of the corporation (“Applicant”) shall file an Online Expression of Interest Form (“EOI”) (see Annex A in the file attached) via the Electronic Filing and Submission Tool (eFAST).

The Applicant must present proof of his or her authority (e.g., Notarized Secretary’s Certificate or Board Resolution, or written Power of Attorney of the resident agent duly filed with the Commission in compliance with Section 128 of Batas Pambansa Big. 68, or Section 145 of the RCC) with the requirements set out under Section 3 of this Circular.

Issuance of Confirmation of Payment

Corporations, which have fully complied with all the conditions set forth in these rules, including the payment of the relevant fines and penalties, shall be issued with all conditions set forth in these rules, including the payment of the relevant fines and penalties, shall be issued with a Confirmation of Payment for Amnesty on Fines and Penalties arising from the non-filing or late filing of the GIS and/or AFS, and non-compliance with MC No. 28. The amnesty granted under this Circular is final and irrevocable, covering the period/s indicated in the said Confirmation

Exceptions

The following entities are excluded from the coverage of the amnesty under this Circular:

a. Corporations whose securities are listed on the Philippine Stock Exchange (“PSE”);

b. Corporations whose securities are registered but not listed on the PSE;

c. Corporations considered as Public Companies;

d. Corporations with intra-corporate dispute;

e. Corporations with disputed GIS; and,

f. Other corporations covered under Sec. 17.2 of RA No. 8799 or the ”Securities Regulation Code".

Validity

Only those which have filed an amnesty application and secured a PAF through the eFast, and paid through the eSPAYSEC or LBP On-Coll Facility until 30 April 2023 shall be eligible for an amnesty under the Circular. Thereafter, the existing scale of fines and penalties issued by the Commision shall be observed.

See attached Memorandum Circular for further details.

.