Accounting Alerts

- 2024

- 2023

- 2022

- 2021

-

2020

2020

- Extension of Deadline for Submission of Forms/Notices

- Online and Manual Submission of Forms/Notices Pursuant to SEC MC 28-2020

- COVID-19 Accounting Implications for CFOs - Debt Modifications

- Discussion Paper 'Business Combination under Common Control'

- SEC Memorandum Circular No. 32 series of 2020

- SEC Memorandum Circular No. 31 series of 2020

- SEC Memorandum Circular No. 28 series of 2020

- Insights into PFRS 16 - Lease Incentives

- IASB issues Interest Rate Benchmark Reform Phase 2

- IFRIC 23 - Uncertainty Over Income Tax Treatments

- COVID-19 Going Concern Considerations

- Extension of Deadlines and Interim Procedures for the Submission of Printed/Hard Copies of Annual Reports

- IASB Defers the Effective Date of IAS 1 Amendments

- Guidelines on the Electronic Submission of the Annual Report and Audited Financial Statements to BSP

- Filing of Annual Reports During the Temporary Closure of the SEC Main Office until July 26, 2020

- Work Suspension at the SEC Main Office and Extension of Deadlines for Certain Corporations

- Adjustment of Deadlines for Submission of Annual Reports to the SEC and Other Announcements

- Amendments to IFRS 17 and IFRS 4

- Filing of Reports and Other Documents in SEC Main Office during Temporary Closure

- Options for the Submission of Reports, Applications and Other Documents to the SEC During Community Quarantine

-

2019

2019

- SEC Extends Deadline for Annual and Quarterly Reports for...

- Deferral of IFRIC Agenda Decision on Over Time Transfer of Constructed Goods (PAS 23) for Real Estate Industry

- Implementation of IFRS 17, Insurance Contracts

- Amendments to Regulations on Financial Audit of Banks and Non-Bank Financial Institutions

- Navigating the Changes to IFRS 2020

- SEC Memorandum Circular No. 2 - 2020 Filing of Annual Financial Statements and General Information Sheet

- IASB issues Classification of Liabilities as Current or Non-current (Amendments to IAS 1)

- GTI IFRS News Q4 2019

- Insights into PFRS 3: Definition of a Business

- IASB issues Interest Rate Benchmark Reform

- Insights into PFRS 16: Presentation and Disclosure

- Insights into PFRS 16: Lease Payments

- Insurance Commission's Guidelines on Lease Accounting for Insurance and Reinsurance Companies

- GTI IFRS News Q1 2019

- Application Deferral of PIC Q&A 2018-H and 2018-14

- Sustainability Reporting Guidelines for Publicly-Listed Companies

- Insights into PFRS 16: Sale and Leaseback Accounting

- Insights into PFRS 16: Transition Choices

- Use of the New General Information Sheet (GIS) Form

- 2019 Filing of Annual FS and GIS

- Navigating the Changes to IFRS 18

- Insights into PFRS 3: Definition of a Business

- GTI IFRS News Q2 2019

- Rules on Material Related Party Transactions for Publicly-listed Companies

- BOA Repealed Resolutions on FS Compilation Services

- GTI IFRS News Q3 2019

- 2019

- 2018 2018

- 2017

- 2016

- 2015

- 2014

- 2008

- 2007

- 2006

- 2005

Amendments on the 2015 Implementing Rules and Regulations of the Securities Regulation Code and SEC Memorandum Circular No. 16, Series of 2004 Relative to the Settlement Cycle from T+3 to T+2

This Accounting Alert is issued to circulate Securities and Exchange Commission (SEC) Memorandum Circular (MC) No. 11-2023 dated August 11, 2023, Amendments on the 2015 Implementing Rules and Regulations of the Securities Regulation Code (The "2015 SRC Rules") and SEC Memorandum Circular No. 16, Series of 2004 Relative to the Settlement Cycle from T+3 to T+2.

Executive Summary

On August 8, 2023, the Commission En Bank resolved to approve the following amendments to the "2015 SRC Rules" and SEC Memorandum Circular (MC) No. 16, series of 2004, relative to the settlement cycle from T+3 to T+2 for Broker Dealers. These amendments shall apply to transactions to be executed starting August 24, 2023.

The Amendments

I. 2015 SRC Rules

Section 1. SRC Rule 49.1.1.5.3 is hereby amended the following:

Computation of Net Liquid Capital (NLC):

In computing NLC, the Equity Eligible for NLC of a Broker Dealer is adjusted by the following, provided, however, that in determining net worth, all long and all short securities position shall be marked to their market value:

a. Adding unrealized profits (or deducting unrealized losses) in the accounts of the Broker Dealer.

b. Deducting fixed assets and assets which cannot be readily converted into cash (less any indebtedness excluded in accordance with SRC Rule 49.1.1.5.2.4 of the Definition of the term Aggregate Indebtedness) including, among other things:

i. Real estate, furniture and fixtures, exchange memberships/trading rights, prepaid rent, insurance and other expenses, goodwill, organization expenses; and,

ii. All unsecured advances and loans, deficits in customers' and non- customers' unsecured and partly secured notes, deficits in special omnibus accounts or similar accounts carried on behalf of another Broker Dealer, after application of calls for margin, marks to the market or other required deposits that are outstanding two (2) business days or less, deficits in customers' and non- customers’ unsecured and partly secured accounts after application of calls for margin, marks to the market or other required deposits that are outstanding two (2) business days or less, except deficits in cash accounts for which not more than one extension respecting a specified securities transaction has been requested and granted, the market value of stock loaned in excess of the value of any collateral received therefore, and any collateral deficiencies in secured demand notes in conformity with SRC Rule 49.1.2.

Section 2. SRC Rule 50 is hereby amended as follow:

Purchases by a customer in a cash account shall be paid in full within two (2) business days after the trade date.

Section 3. SRC Rule 52 is hereby amended as follows:

a. Monthly Aging of Customers' Receivables

The aging schedule shall indicate the monetary and securities collateral values of the customers' receivable as of end of month, broken down as follows:

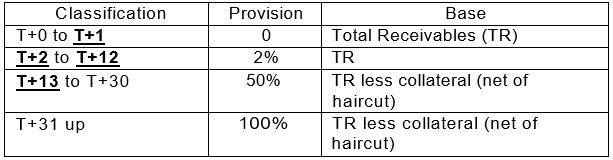

b. Every Broker Dealer shall appropriate Allowance for Doubtful Accounts (ADA) using and in accordance with the following schedule:

The ADA is computed by getting, for each doubtful account, an amount equivalent to the provision (see table (b) above) of the amount outstanding, net of collateral (net of haircut). The basis for the computation would be the individual accounts.

II. SEC MEMORANDUM CIRCULAR NO. 16 SERIES OF 2004

The following sections were also amended under SEC MC 2023-11. Please refer to the attached circular for the details and respective discussion of each section.

Section 4. Subsection III Computation of NLC

Section 5. Schedule for Part 4 Schedule for Specific and General Provisioning for Overdue Accounts

Section 6. Schedule B.2 Counterparty Risk Requirement Counterparty Risk Factors for Unsettled Agency Trades, SRC Rule 49 (H), Subsection VI

Section 7. Schedule B.3 Counterparty Risk Requirement Counterparty Risk Factors for Unsettled Principal Trades, SRC Rule 49 (H), Subsection VI

Section 8. Schedule B.4 Counterparty Risk Factors for Debts/Loans, Contra Loss, And Other Debts Due, SRC Rule 49 (H), Subsection

See attached Memorandum Circular for further details.

.