Accounting Alerts

- 2024

- 2023

- 2022

- 2021

-

2020

2020

- Extension of Deadline for Submission of Forms/Notices

- Online and Manual Submission of Forms/Notices Pursuant to SEC MC 28-2020

- COVID-19 Accounting Implications for CFOs - Debt Modifications

- Discussion Paper 'Business Combination under Common Control'

- SEC Memorandum Circular No. 32 series of 2020

- SEC Memorandum Circular No. 31 series of 2020

- SEC Memorandum Circular No. 28 series of 2020

- Insights into PFRS 16 - Lease Incentives

- IASB issues Interest Rate Benchmark Reform Phase 2

- IFRIC 23 - Uncertainty Over Income Tax Treatments

- COVID-19 Going Concern Considerations

- Extension of Deadlines and Interim Procedures for the Submission of Printed/Hard Copies of Annual Reports

- IASB Defers the Effective Date of IAS 1 Amendments

- Guidelines on the Electronic Submission of the Annual Report and Audited Financial Statements to BSP

- Filing of Annual Reports During the Temporary Closure of the SEC Main Office until July 26, 2020

- Work Suspension at the SEC Main Office and Extension of Deadlines for Certain Corporations

- Adjustment of Deadlines for Submission of Annual Reports to the SEC and Other Announcements

- Amendments to IFRS 17 and IFRS 4

- Filing of Reports and Other Documents in SEC Main Office during Temporary Closure

- Options for the Submission of Reports, Applications and Other Documents to the SEC During Community Quarantine

-

2019

2019

- SEC Extends Deadline for Annual and Quarterly Reports for...

- Deferral of IFRIC Agenda Decision on Over Time Transfer of Constructed Goods (PAS 23) for Real Estate Industry

- Implementation of IFRS 17, Insurance Contracts

- Amendments to Regulations on Financial Audit of Banks and Non-Bank Financial Institutions

- Navigating the Changes to IFRS 2020

- SEC Memorandum Circular No. 2 - 2020 Filing of Annual Financial Statements and General Information Sheet

- IASB issues Classification of Liabilities as Current or Non-current (Amendments to IAS 1)

- GTI IFRS News Q4 2019

- Insights into PFRS 3: Definition of a Business

- IASB issues Interest Rate Benchmark Reform

- Insights into PFRS 16: Presentation and Disclosure

- Insights into PFRS 16: Lease Payments

- Insurance Commission's Guidelines on Lease Accounting for Insurance and Reinsurance Companies

- GTI IFRS News Q1 2019

- Application Deferral of PIC Q&A 2018-H and 2018-14

- Sustainability Reporting Guidelines for Publicly-Listed Companies

- Insights into PFRS 16: Sale and Leaseback Accounting

- Insights into PFRS 16: Transition Choices

- Use of the New General Information Sheet (GIS) Form

- 2019 Filing of Annual FS and GIS

- Navigating the Changes to IFRS 18

- Insights into PFRS 3: Definition of a Business

- GTI IFRS News Q2 2019

- Rules on Material Related Party Transactions for Publicly-listed Companies

- BOA Repealed Resolutions on FS Compilation Services

- GTI IFRS News Q3 2019

- 2019

- 2018 2018

- 2017

- 2016

- 2015

- 2014

- 2008

- 2007

- 2006

- 2005

Revised Rules and Procedures for Prudential Reporting Requirements and On-site Examination/Off-site Verification for Insurance and Reinsurance Brokers

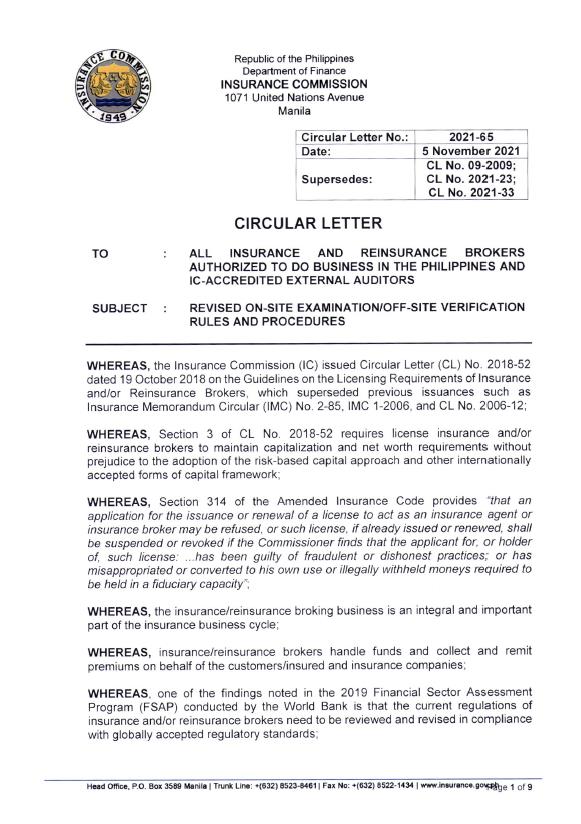

This Accounting Alert is issued to circulate Insurance Commission (IC/Commission) Circular Letter (CL) No. 2021-65 dated November 5, 2021 applicable to IC-accredited insurance and/or reinsurance brokers and its external auditors.

Overview

The IC circular letter No 2021-65, revised on-site examination and off-site verification, covers the revised rules and procedures on the determination of net worth, fiduciary ratio, on-site and off-site examination of insurance and/or reinsurance brokers with valid Certificate of Authority from the lC.

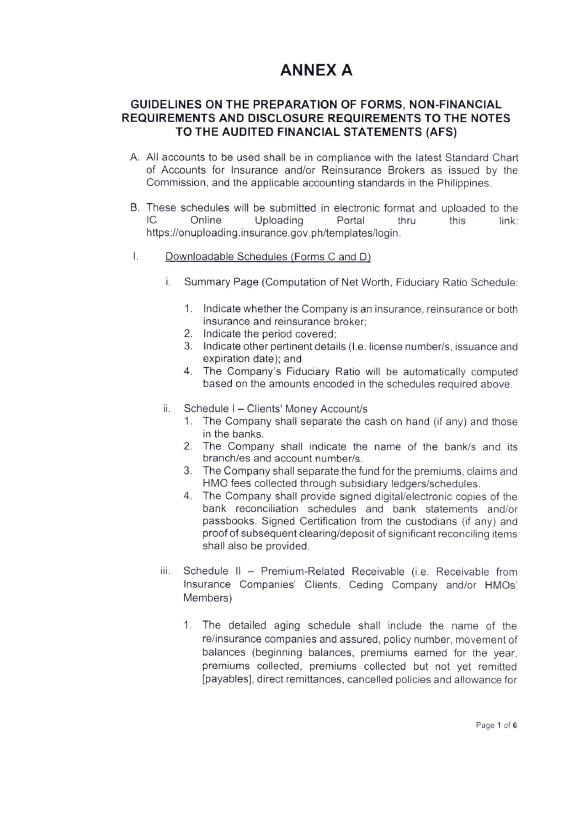

This CL also covers the reports required to be filed by the insurance and/or reinsurance brokers with the lC, and additional disclosures required to be made in the Audited Financial Statements (AFS), as specified in Annex A as attached herewith.

The CL was issued with the following objectives:

- To complement the enforcement of Section 3 of CL No. 2018-52, "Guidelines on the Licensing Requirements of the lnsurance and/or Reinsurance Brokers";

- To exercise the authority and power of the lC to refuse renewal, suspend or revoke the license of any insurance and/or reinsurance brokers in accordance with the Section 314 of the Amended lnsurance Code; and,

- To provide guidance on the preparer and lC-accredited external auditor on the assets or liabilities to be recognized for the purpose of prudential reporting to the IC.

Prudential Financial Requirements

All insurance and/or reinsurance brokers with valid Certificate of Authority from the lC shall, at all times, comply with the following:

1. Net Worth Requirement

As provided under Section 3 of CL No. 2018-52, licensed insurance and/or reinsurance brokers are required to maintain the following net worth requirements:

The balances as reported in the AFS, as audited by an lC-accredited external auditor, shall be the basis for the net worth computation, provided that, the other prudential requirements and disclosures are complied with (i.e., clients' money/fiduciary accounts).

2. Surety Bond and Errors and Omissions Policy

The requirements on the submission of surety bond and errors and omission policy shall be in accordance with the provisions of Sections 6 and 7 of lC CL No. 2018-52 and/or equivalent future issuances.

3. Keeping Separate Clients' Money Account

Section 315 of the Amended lnsurance Code requires every license insurance and/or reinsurance broker to ensure faithful performance of its fiduciary responsibilities on behalf of its clients and partner insurance and/or reinsurance companies. Thus, an insurance and/or reinsurance broker is required to keep client monies in a client account separate from its own monies. lt is not allowed to use client monies for any purpose other than for the purposes of the client.

4. Fiduciary Ratio Requirement

ln addition to the net worth requirement above, an insurance and/or reinsurance broker with a credit aqreement with an insurance/reinsurance company or broker shall comply with the Fiduciary Ratio Requirement set by the lC.

Fiduciary ratio is computed by dividing the total fiduciary assets, either cash or receivables being held by an insurance and/or reinsurance broker, over the total fiduciary liabilities. The formula is as follows:

The fiduciary ratio to be maintained shall be 1:1. Amounts to be used is gross of the commissions, allowances for impairment, taxes, fees and other charges.

5. Keeping Proper Books of Accounts.

All licensed insurance and/or Insurance brokers should strictly adhere to the requirements of CL No. 2018-17 or any equivalent future issuance in preparation of their statutory and prudential submission to the lC.

Submission of Annual AFS and Reports by the Auditor in Compliance with the Requirements Above

At a minimum, all licensed insurance and/or reinsurance brokers shall submit the following on or before May 31 after the close of the calendar year:

- AFS;

- Schedule of Clients' Money Accounts;

- Schedule of Premium-related Accounts and its reconciliation;

- Schedule of Fiduciary Computation; and,

- Other requirements deemed necessary by the lC.

Guidelines in the preparation of the schedule and complete set of requirements are found in Annex "A" as attached herewith.

On-site Examination/Off-site Verification

- The lC shall conduct regular off-site verification or monitoring. On-site examination, on the other hand, shall be conducted at least once every five (5) years and as deemed necessary, based on the previous risk ranking of the company. On-site examination and off-site verification include supervisory reporting, review, and analysis of conduct of business (such as but not limited to complaints, arrangements with (re)insurance companies and brokers and disclosure of information). The lC may specify information to be provided for onsite examination and off-site verification purposes, including information to be reported routinely or on an ad hoc basis. Supervisory reporting requirements may include but are not limited to the abovementioned reports and those enumerated in Annex A.

- The lC examiners may coordinate with other lC divisions whether information provided is sufficient to cover all areas of the supervisory reporting and review.

- The insurance and/or reinsurance broker shall supply any document or information that is requested by the lC.

- The lC may provide an exception to certain requirements upon the lnsurance Commissioner's approval of the insurance and/or reinsurance broker's formal written request.

Transitory Provisions

All lnsurance and/or Reinsurance Brokers with valid Certificate of Authority are required to adopt the requirements of this CL in the preparation of their 2022 financial statements and submissions to the lC on May 31, 2023.

The CL also discussed provisions on Broker's classification, regulatory and supervisory enforcement, and review provision.

See attached Circular Letter and Annex A for further details.

.

Insurance Commission CL No. 2021-65

.