Accounting Alerts

- 2024

- 2023

- 2022

- 2021

-

2020

2020

- Extension of Deadline for Submission of Forms/Notices

- Online and Manual Submission of Forms/Notices Pursuant to SEC MC 28-2020

- COVID-19 Accounting Implications for CFOs - Debt Modifications

- Discussion Paper 'Business Combination under Common Control'

- SEC Memorandum Circular No. 32 series of 2020

- SEC Memorandum Circular No. 31 series of 2020

- SEC Memorandum Circular No. 28 series of 2020

- Insights into PFRS 16 - Lease Incentives

- IASB issues Interest Rate Benchmark Reform Phase 2

- IFRIC 23 - Uncertainty Over Income Tax Treatments

- COVID-19 Going Concern Considerations

- Extension of Deadlines and Interim Procedures for the Submission of Printed/Hard Copies of Annual Reports

- IASB Defers the Effective Date of IAS 1 Amendments

- Guidelines on the Electronic Submission of the Annual Report and Audited Financial Statements to BSP

- Filing of Annual Reports During the Temporary Closure of the SEC Main Office until July 26, 2020

- Work Suspension at the SEC Main Office and Extension of Deadlines for Certain Corporations

- Adjustment of Deadlines for Submission of Annual Reports to the SEC and Other Announcements

- Amendments to IFRS 17 and IFRS 4

- Filing of Reports and Other Documents in SEC Main Office during Temporary Closure

- Options for the Submission of Reports, Applications and Other Documents to the SEC During Community Quarantine

-

2019

2019

- SEC Extends Deadline for Annual and Quarterly Reports for...

- Deferral of IFRIC Agenda Decision on Over Time Transfer of Constructed Goods (PAS 23) for Real Estate Industry

- Implementation of IFRS 17, Insurance Contracts

- Amendments to Regulations on Financial Audit of Banks and Non-Bank Financial Institutions

- Navigating the Changes to IFRS 2020

- SEC Memorandum Circular No. 2 - 2020 Filing of Annual Financial Statements and General Information Sheet

- IASB issues Classification of Liabilities as Current or Non-current (Amendments to IAS 1)

- GTI IFRS News Q4 2019

- Insights into PFRS 3: Definition of a Business

- IASB issues Interest Rate Benchmark Reform

- Insights into PFRS 16: Presentation and Disclosure

- Insights into PFRS 16: Lease Payments

- Insurance Commission's Guidelines on Lease Accounting for Insurance and Reinsurance Companies

- GTI IFRS News Q1 2019

- Application Deferral of PIC Q&A 2018-H and 2018-14

- Sustainability Reporting Guidelines for Publicly-Listed Companies

- Insights into PFRS 16: Sale and Leaseback Accounting

- Insights into PFRS 16: Transition Choices

- Use of the New General Information Sheet (GIS) Form

- 2019 Filing of Annual FS and GIS

- Navigating the Changes to IFRS 18

- Insights into PFRS 3: Definition of a Business

- GTI IFRS News Q2 2019

- Rules on Material Related Party Transactions for Publicly-listed Companies

- BOA Repealed Resolutions on FS Compilation Services

- GTI IFRS News Q3 2019

- 2019

- 2018 2018

- 2017

- 2016

- 2015

- 2014

- 2008

- 2007

- 2006

- 2005

Insights into PAS 36, Impairment of Assets - Identifying Cash-Generating Unit

This Accounting Alert is issued to provide an overview of Philippine Accounting Standards (PAS) 36, Impairment of Assets, to assist preparers of financial statements and those charged with governance of reporting entities in understanding the requirements of PAS 36, and to revisit some areas where confusion has been seen in practice.

Overview

The accounting requirements regarding impairment of tangible and intangible assets are governed by PAS 36, Impairment of Assets. The requirements are not new, however, remain challenging as the guidance is detailed and complex in some areas.

Identifying cash-generating units (CGUs) is a critical step in the impairment review and can have a significant impact on its results. That said, the identification of CGUs requires judgement. The identified CGUs may also change due to changes in an entity’s operations and the way it conducts them.

This Accounting Alert discusses how to identify CGUs and its role in the impairment review.

Cash-Generating Unit

A Cash-Generating Unit (CGU) is the smallest identifiable group of assets that generates cash inflows that are largely independent of the cash inflows from other assets or groups of assets.

Roles of CGU in the Impairment Review

A CGU serves two primary roles in the impairment review. It facilitates the testing of:

- assets for which the recoverable amount cannot be determined individually, and

- goodwill and corporate assets for impairment.

Goodwill and corporate assets, by definition, do not generate cash inflows on their own and therefore, must be allocated to a CGU or groups of CGUs for impairment testing purposes.

Identifying CGUs

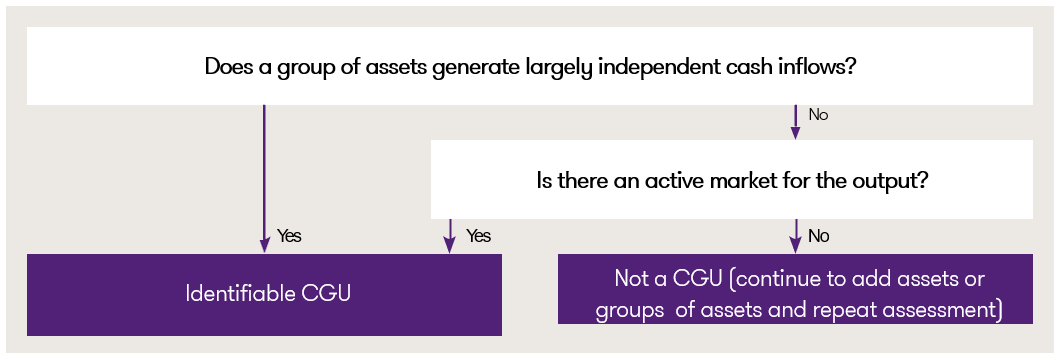

The objective of identifying CGUs is to identify the smallest identifiable group of assets that generates largely independent cash inflows. CGUs are identified at the lowest level to minimize the possibility that impairments of one asset or group will be masked by a high-performing asset. To identify a CGU, an entity asks two questions:

- Does a group of assets generate largely independent cash inflows?

- Is there an active market for the output?

The Accounting Alert also provides practical insights and illustrative examples on how to identify a CGU. It also provides practical insights on changes in the identified CGUs.

See attached Accounting Alert for further details.

.

Insights into PAS 36 - Identifying CGUs