Accounting Alerts

- 2024

- 2023

- 2022

- 2021

-

2020

2020

- Extension of Deadline for Submission of Forms/Notices

- Online and Manual Submission of Forms/Notices Pursuant to SEC MC 28-2020

- COVID-19 Accounting Implications for CFOs - Debt Modifications

- Discussion Paper 'Business Combination under Common Control'

- SEC Memorandum Circular No. 32 series of 2020

- SEC Memorandum Circular No. 31 series of 2020

- SEC Memorandum Circular No. 28 series of 2020

- Insights into PFRS 16 - Lease Incentives

- IASB issues Interest Rate Benchmark Reform Phase 2

- IFRIC 23 - Uncertainty Over Income Tax Treatments

- COVID-19 Going Concern Considerations

- Extension of Deadlines and Interim Procedures for the Submission of Printed/Hard Copies of Annual Reports

- IASB Defers the Effective Date of IAS 1 Amendments

- Guidelines on the Electronic Submission of the Annual Report and Audited Financial Statements to BSP

- Filing of Annual Reports During the Temporary Closure of the SEC Main Office until July 26, 2020

- Work Suspension at the SEC Main Office and Extension of Deadlines for Certain Corporations

- Adjustment of Deadlines for Submission of Annual Reports to the SEC and Other Announcements

- Amendments to IFRS 17 and IFRS 4

- Filing of Reports and Other Documents in SEC Main Office during Temporary Closure

- Options for the Submission of Reports, Applications and Other Documents to the SEC During Community Quarantine

-

2019

2019

- SEC Extends Deadline for Annual and Quarterly Reports for...

- Deferral of IFRIC Agenda Decision on Over Time Transfer of Constructed Goods (PAS 23) for Real Estate Industry

- Implementation of IFRS 17, Insurance Contracts

- Amendments to Regulations on Financial Audit of Banks and Non-Bank Financial Institutions

- Navigating the Changes to IFRS 2020

- SEC Memorandum Circular No. 2 - 2020 Filing of Annual Financial Statements and General Information Sheet

- IASB issues Classification of Liabilities as Current or Non-current (Amendments to IAS 1)

- GTI IFRS News Q4 2019

- Insights into PFRS 3: Definition of a Business

- IASB issues Interest Rate Benchmark Reform

- Insights into PFRS 16: Presentation and Disclosure

- Insights into PFRS 16: Lease Payments

- Insurance Commission's Guidelines on Lease Accounting for Insurance and Reinsurance Companies

- GTI IFRS News Q1 2019

- Application Deferral of PIC Q&A 2018-H and 2018-14

- Sustainability Reporting Guidelines for Publicly-Listed Companies

- Insights into PFRS 16: Sale and Leaseback Accounting

- Insights into PFRS 16: Transition Choices

- Use of the New General Information Sheet (GIS) Form

- 2019 Filing of Annual FS and GIS

- Navigating the Changes to IFRS 18

- Insights into PFRS 3: Definition of a Business

- GTI IFRS News Q2 2019

- Rules on Material Related Party Transactions for Publicly-listed Companies

- BOA Repealed Resolutions on FS Compilation Services

- GTI IFRS News Q3 2019

- 2019

- 2018 2018

- 2017

- 2016

- 2015

- 2014

- 2008

- 2007

- 2006

- 2005

Insurance Commission Circular Letters: Regulatory Reliefs, Online Submission of Reports, and Deferral of IFRS 17 Implementation

This Accounting Alert is issued to summarize recent circular letters (CLs) issued by the Insurance Commission (IC) from May 14 to May 18, 2020.

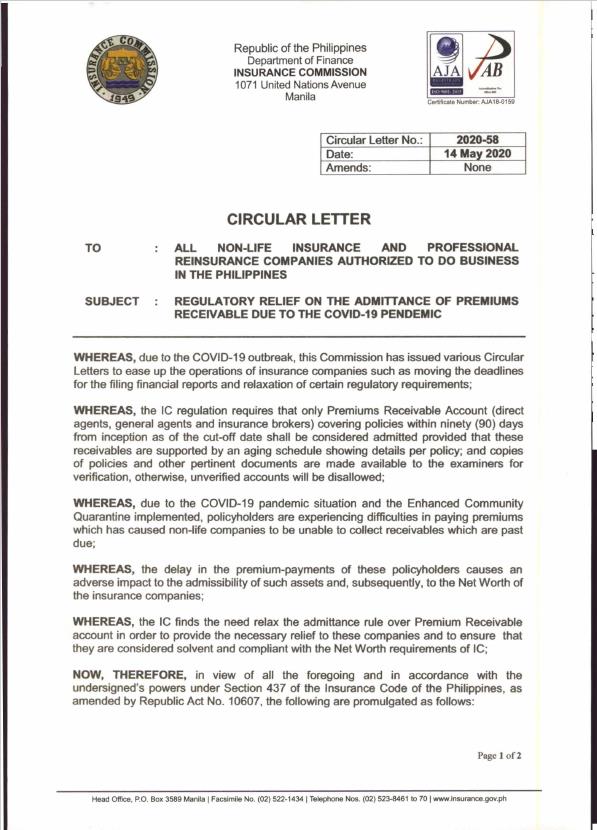

CL No. 2020-58: Regulatory Relief on the Admittance of Premiums Receivable due to the COVID-19 Pandemic

Covered entities: All non-life insurance and professional reinsurance companies

Effectivity: Applied to annual and quarterly financial reports for the year 2020, unless extended or changed as deemed necessary by the IC.

The IC issued CL No. 2020-58 on May 14, 2020 to relax the admittance rule over premium receivables in view of the delays in collection of premiums from policyholders due to the COVID-19 pandemic. The basis for admitting Premium Receivable account (direct agents, general agents and insurance brokers) for all non-life insurance and professional reinsurance companies shall be adjusted from 90 days to 180 days from the date of issuance of the policies.

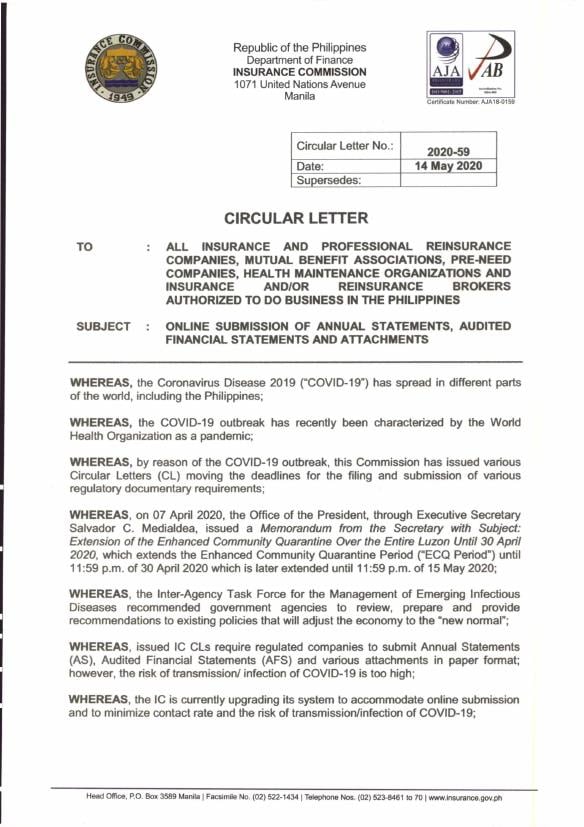

CL No. 2020-59: Online Submission of Annual Statements (AS), Audited Financial Statements (AFS) and Attachments

Covered entities: All insurance and professional reinsurance companies, mutual benefit associations, pre-need companies, health maintenance organizations and insurance and/or reinsurance brokers

Effectivity: Shall take effect immediately

The IC issued CL No. 2020-59 on May 14, 2020 requiring all regulated companies to submit their AS, AFS and attachments for the reporting periods starting 2019 onwards through electronic means. These companies are also advised to send the said documents in a compressed and password-protected file. Notwithstanding this new requirement, the IC may also require a company to submit and likewise, examine the original hard copy of the electronically submitted documents. The IC has released updated checklists together with the CL for guidance of each of the regulated entities.

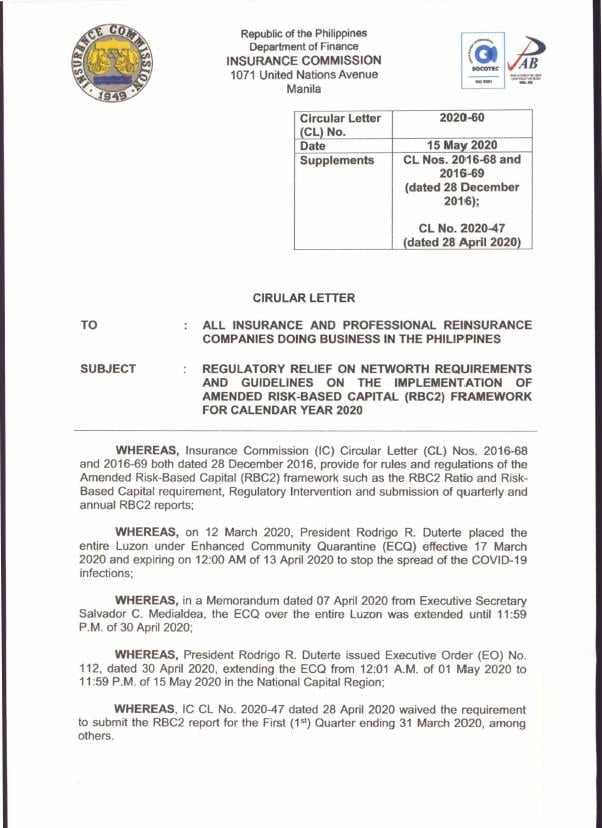

CL No. 2020-60: Regulatory Relief on Networth Requirements and Guidelines on the Implementation of Amended Risk-based Capital (RBC2) Framework for Calendar Year 2020

Covered entities: All insurance and professional reinsurance companies

Effectivity: Shall take effect immediately

The IC, through CL No. 2020-60 issued on May 15, 2020, promulgated the following guidelines:

1. All insurance companies already compliant with the networth requirements as of December 31, 2019 under Section 194 of the Amended Insurance Code before the declaration of ECQ and adversely affected by the crisis are:

a. relieved from the quarterly compliance of the networth requirements of P900,000,000; and,

b. required to comply with the CL 2016-68 (Amended Risk-based Capital Framework) and revised regulatory intervention (RBC ratio)

2. All insurance companies which are not compliant before the declaration of the ECQ are required to make fulfill their respective commitments to the IC to put up additional funds to cover the networth deficiency before availing the relief as discussed in (1) above.

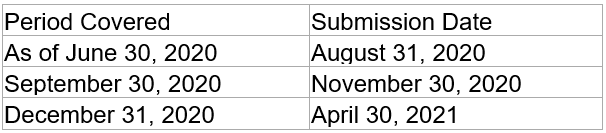

3. Submission of 2020 RBC2 reports for the following periods shall be required.

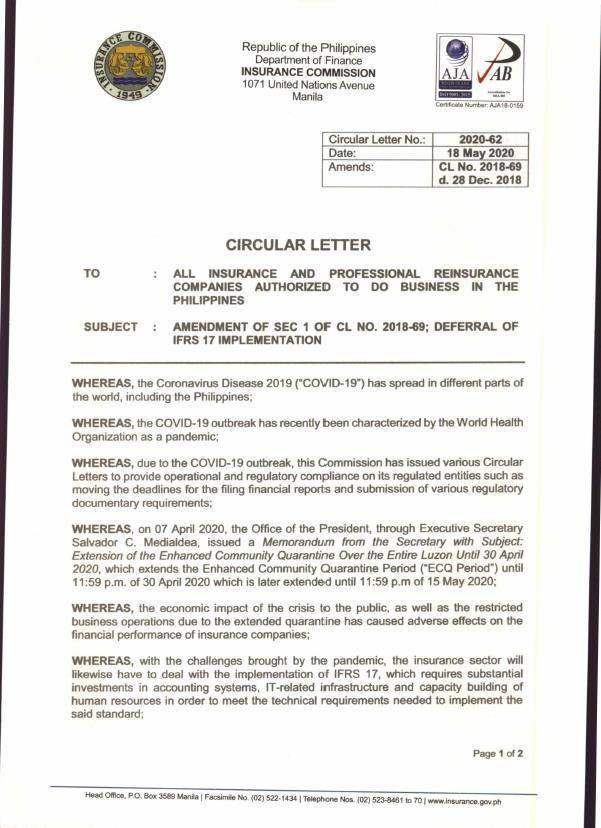

CL No. 2020-62: Deferral of IFRS 17 Implementation

Covered entities: All insurance and professional reinsurance companies

Effectivity: Shall take effect immediately

On March 17, 2020, the International Accounting Standards Board (IASB) has decided to further defer the effective date of IFRS 17, Insurance Contracts to annual reporting periods beginning on or after January 1, 2023. In view of this, the IC, through CL No. 2020-62 issued on May 18, 2020, amended provisions under Section 1 of CL No. 2018-69, Deferral of Implementation of IFRS 17 - Insurance Contracts and deferred the implementation of IFRS 17 for life and non-life insurance industries by two (2) years after its effective date as decided by the IASB.

See attached Circular Letters for further details.