Annual Income Tax Return Filing and Payment Guidelines for the Calendar Year 2025

(Revenue Memorandum Circular No. 20-2026 issued on March 16, 2026)

This Tax Alert is issued to inform taxpayers on the prescribed guidelines in the filing of Annual Income Tax Returns (AITR) and payment of corresponding taxes due thereon for the Calendar Year ending December 31, 2025.

Filing and Payment of Tax Return

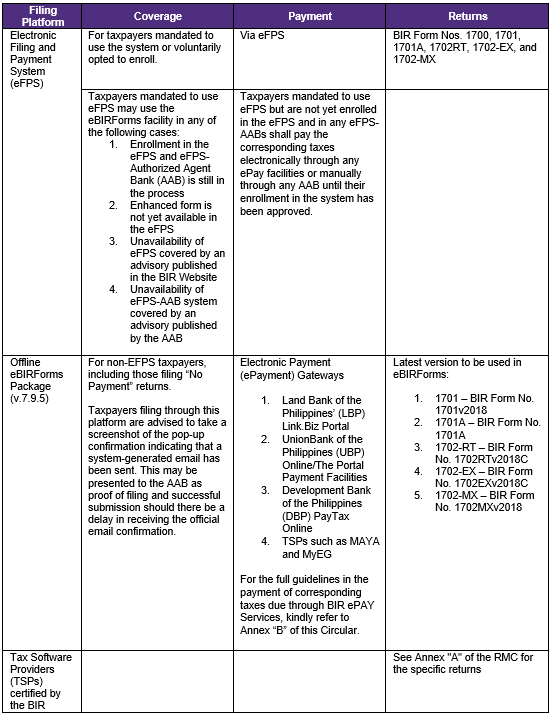

The Bureau of Internal Revenue (“BIR”) reminds all concerned taxpayers of the existing procedures for the electronic filing of tax returns through the following BIR electronic filing platforms:

Manual Filing and Payment

Manual filing shall only be allowed under the following cases:

- When there is a BIR-issued Advisory on the unavailability of the electronic platforms;

- When there is justifiable reason as may be determined by the Commissioner of Internal Revenue (CIR) or his authorized representative; or

- When the tax return is still unavailable on any of the electronic platforms.

Taxpayers may also pay manually through over-the-counter with any AABs under the following cases:

- When the tax return has been electronically filed using the eBIRForms;

- When the enrollment of a mandated eFPS user with the eFPS-AAB is still in process; or

- When the BIR eFPS and/or eFPS-AAB system is unavailable

BIR eLounge facility

BIR eLounge facility can be used by taxpayers requiring assistance in the electronic filing of their tax returns and payment of the corresponding taxes due thereon. Priority will be given to senior citizens or persons with disabilities; employees deriving purely compensation income from 2 or more employers although income has been correctly subjected to withholding tax, but spouse is not entitled to substituted filing; employees qualified for substituted filing but opted to file an ITR; and taxpayers without internet facility, and taxpayers filing their own returns.

Tax practitioners who are filing several returns for their clients may use the eLounge for a maximum of three transactions per day and not exceeding one hour, whichever is shorter.

Revenue personnel shall continue assisting taxpayers already within BIR premises on or before 5:00 PM until the completion of the filing of 2025 AITR and the submission of required attachments through the Electronic Audited Financial Statements (eAFS) system.

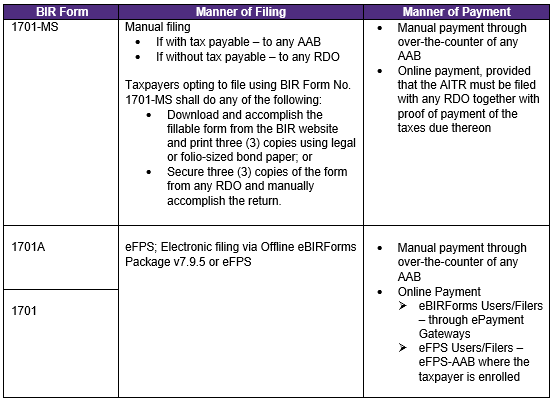

Guidelines in the Filing of BIR Form Nos. 1701-MS, 1701, and 1701A

The BIR, through this Circular and the attached Annex “C”, clarified the applicable filing and payment guidelines for the calendar year 2025, covering the use of BIR Form Nos. 1701-MS, 1701, and 1701A.

Individual business taxpayers classified as Micro or Small, regardless of the income tax return form indicated in their Certificate of Registration (COR) or BIR Form No. 2303, may file their AITR using any of the prescribed forms, subject to the applicable filing method and mode of payment.

The BIR further clarified the following:

- Taxpayers who have electronically filed using either BIR Form No. 1701 or 1701A and paid the corresponding taxes due are no longer required to manually file BIR Form No. 1701-MS.

- To simplify compliance, micro and small taxpayers who elect electronic filing may accomplish only the minimum required fields, consistent with the information required under BIR Form No. 1701-MS, as outlined in Annex “D” of this Circular. They are likewise not required to update or amend their Certificate of Registration (COR) if it reflects only BIR Form “1701/1701A”.

- Medium and large taxpayers are required to electronically file their AITR using BIR Form No. 1701 or 1701A, as applicable.

Further, wrong venue filing shall not apply to individual business taxpayers classified as Micro and Small under the following circumstances:

- Where BIR Form No. 1701 or 1701A has already been filed electronically through eBIRForms, eFPS, or TSP; and

- Where BIR Form No. 1701-MS has already been manually filed and the corresponding taxes paid.

Submission of Required Attachments to Filed Returns

Taxpayers shall submit only those attachments that are applicable, which may include, among others:

- FRN or TRRC as proof of eFiling in eFPS and eBIRForms, respectively;

- Proof of Payment/Acknowledgement Receipt of Payment;

- Certificate of Independent CPA duly accredited by the BIR;

- Unaudited or Audited Financial Statements (AFS), including Notes to FS;

- Statement of Management Responsibilities (SMR);

- Relevant BIR Certificates such as:

- a. BIR Form No. 2307 – Certificate of Creditable Tax Withheld at Source;

- b. BIR Form No. 1606 – Withholding Tax Remittance Return for Onerous Transfer of Real Property Other Than Capital Asset (including Taxable and Exempt);

- c. BIR Form No. 2304 – Certificate of Income Payments not Subjected to Withholding Tax;

- d. BIR Form No. 2316 – Certificate of Compensation Payment/Tax Withheld;

- System-generated Acknowledgement Receipt of Validation Report of electronically submitted Summary Alphalist of Withholding Taxes (SAWT);

- Duly approved Tax Debit Memo;

- Proof of tax credits

- a. Foreign tax credits;

- b. Prior year’s excess credits;

- c. Other tax credits/payments; and/or

- BIR Form No. 1709 – Information Return on Transactions with Related Party

All required attachments to the AITR, if any, shall be submitted electronically through the eAFS system of the BIR. The Transaction Reference Number (TRN) or Confirmation Receipt generated by the eAFS system shall serve as proof of submission of the attachments to the BIR.

In cases where the eAFS is unavailable, as officially announced by the BIR, taxpayers may manually submit the required attachments to the Revenue District Office (RDO) or office having jurisdiction over the taxpayer.

For eFPS, eBIRForms, and TSP filers, attachments shall be submitted within fifteen (15) days from the deadline of filing the return, or within fifteen (15) days from actual filing in case of late filing, through the eAFS system. The same deadline applies to manual filers of BIR Form No. 1701-MS, with electronic submission via eAFS.

For taxpayers that filed their AFS through eAFS, the system-generated confirmation receipt containing the company name, TIN, taxable year, and uploaded file details shall suffice in lieu of a manually stamped “Received” copy.