Supplemental Guidelines for the Application of New Frameworks and Standards for Mutual Benefit Associations (MBAs)

Summary

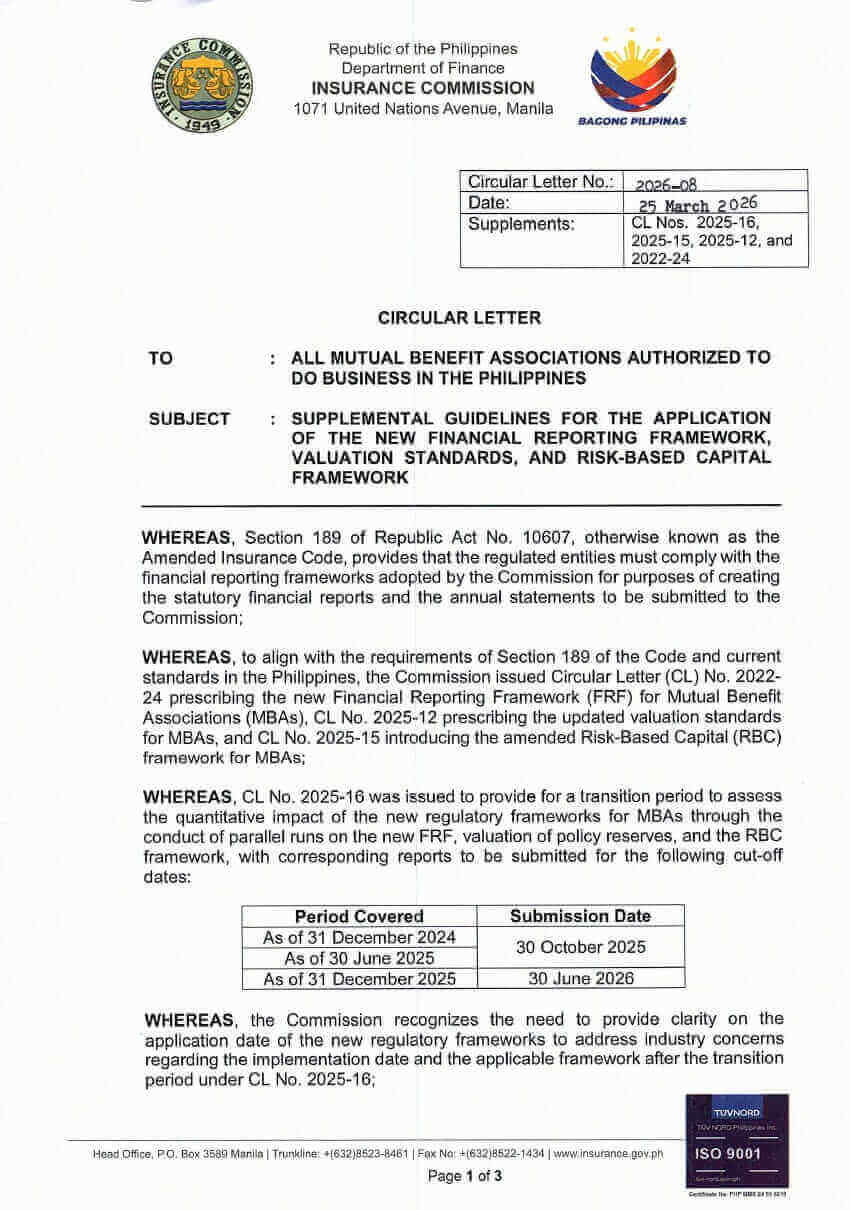

The Insurance Commission (IC) issued Circular Letter (CL) No. 2026‑08 on 25 March 2026, providing supplemental guidelines on the application date, transition accounting, and extended parallel run requirements in relation to the new Financial Reporting Framework (FRF), valuation standards, and Risk‑Based Capital (RBC) framework applicable to Mutual Benefit Associations (MBAs).

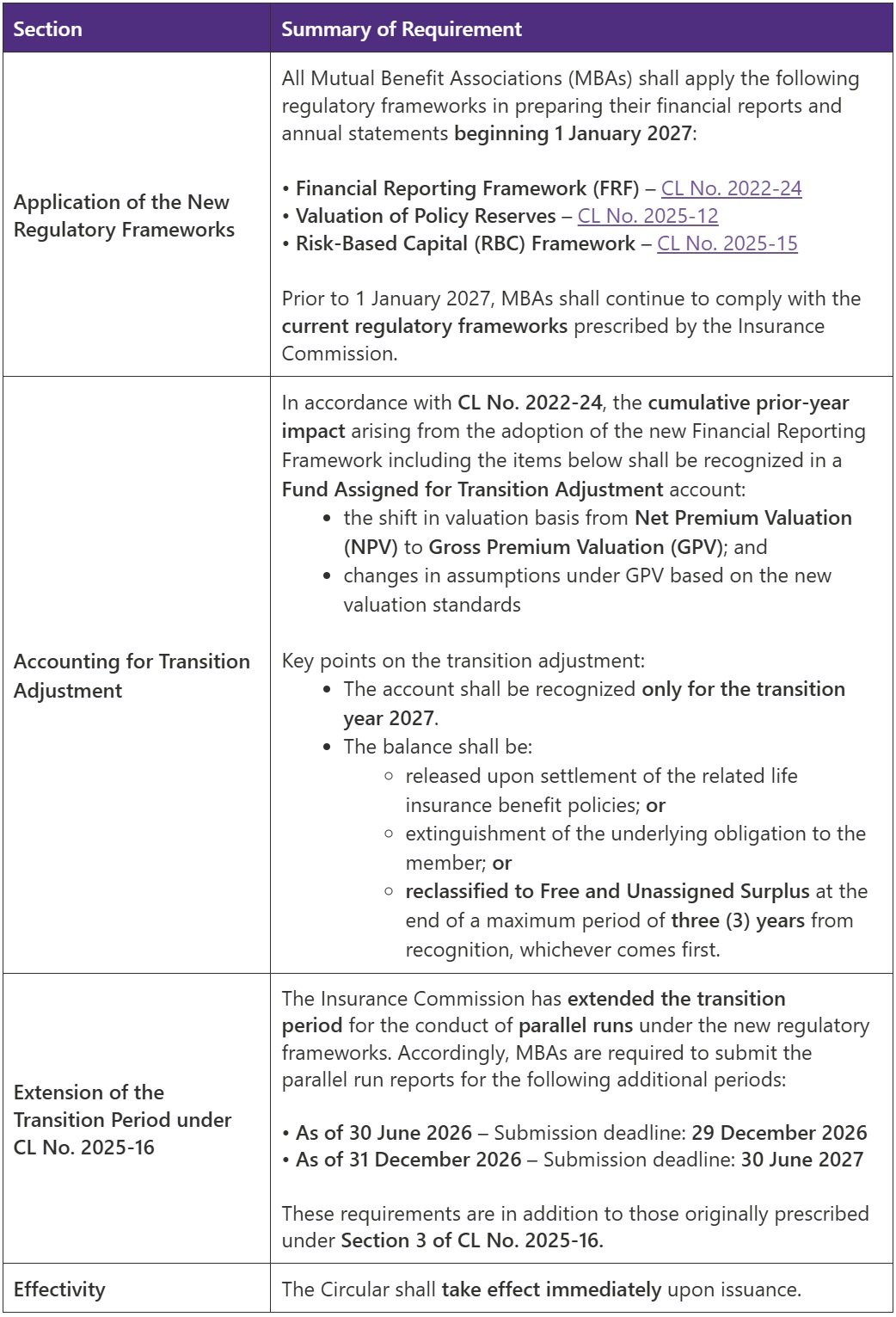

The Circular clarifies industry concerns arising from the transition provisions under CL No. 2025‑16 and prescribes the mandatory application date of 1 January 2027, including the accounting treatment of transition adjustments and an extension of the parallel run period under the new regulatory frameworks.

Key Provisions

Recommended Action Points for Mutual Benefit Associations

- Confirm readiness for full adoption of the new FRF, valuation standards, and RBC framework by 1 January 2027.

- Ensure proper tracking and documentation of transition adjustments for recognition in the 2027 transition year.

- Update systems and reporting timelines to comply with the extended parallel run submission requirements.

- Coordinate with actuaries and finance teams to align valuation methodologies and RBC computations under the new framework.

References

This Accounting Alert provides only a high‑level overview of the regulatory updates. For complete and authoritative guidance, readers are encouraged to review the full Circular Letter issued by the Insurance Commission below:

Circular Letter No. 2026-08 | Supplemental Guidelines for the Application of the New Financial Reporting Framework, Valuation Standards, and Risk-Based Capital Framework

To explore additional Insurance Commission Circulars referenced in this alert or to access related regulatory issuances, you may also visit www.insurance.gov.ph for more comprehensive guidance.