PFRS 20 - the new rate regulation standard

Executive summary

On May 27, 2026, the International Accounting Standards Board (IASB) issued a new standard on accounting for companies subject to rate regulation entitled IFRS 20 ‘Regulatory Assets and Regulatory Liabilities’ (the Standard). Once adopted locally, this will be known as PFRS 20. This Standard replaces PFRS 14 ‘Regulatory Deferral Accounts’ and will impact entities that provide goods and/or services that are subject to specific types of rate regulation. The Standard includes new recognition and measurement requirements, as well as presentation and disclosures to enable users of the financial statements to understand how differences in timing due to rate regulations impact the performance of an entity. PFRS 20 is effective for annual reporting periods beginning on or after 1 January 2029, with early application permitted.

Background

Reporting entities operating in specific industries which provide vital services such as water, gas and electricity are often subject to regulations which determine how much they are allowed to charge their customers. These arrangements are governed by regulatory agreements. This Standard applies to entities that are subject to regulatory agreements that determine the compensation that the entity is entitled to charge for regulatory goods and services, and when the entity is allowed to change that compensation through regulated rates.

In certain circumstances, such agreements give rise to so called differences in timing, where the revenue recognized in a period when applying PFRS 15 ‘Revenue from Contracts with Customers’ does not match the compensation to which an entity is entitled. It is these situations that PFRS 20 aims to address with the requirements summarized below.

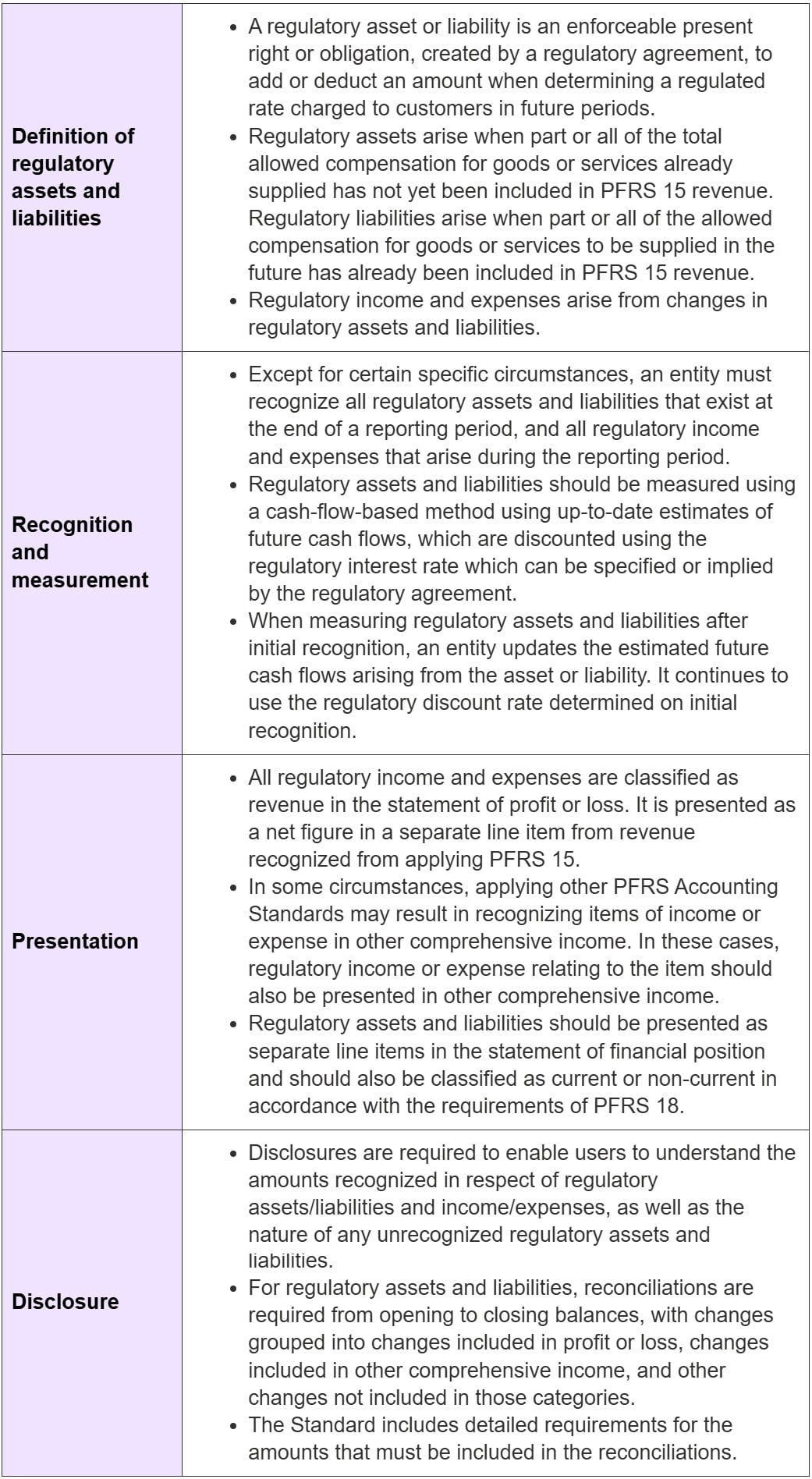

Summary of new requirements

PFRS 20 is a standard which supplements the information provided by applying other PFRS Accounting Standards such as PFRS 15. An entity is required to apply other PFRS Accounting Standards to account for rights and obligations created by regulatory agreements before applying PFRS 20. PFRS 20 key requirements are summarized below.

To read the full Standard, and access other supporting material prepared by the IASB, please refer to the IASB’s announcement by clicking here.

Effective date and transition

PFRS 20 is effective for annual reporting periods beginning on or after 1 January 2029, with early application permitted.