-

Audit approach overview

Our audit approach will allow our client's accounting personnel to make the maximum contribution to the audit effort without compromising their ongoing responsibilities

-

Annual and short period audit

At P&A Grant Thornton, we provide annual and short period financial statement audit services that go beyond the normal expectations of our clients. We believe strongly that our best work comes from combining outstanding technical expertise, knowledge and ability with exceptional client-focused service.

-

Review engagement

A review involves limited investigation with a narrower scope than an audit, and is undertaken for the purpose of providing limited assurance that the management’s representations are in accordance with identified financial reporting standards. Our professionals recognize that in order to conduct a quality financial statement review, it is important to look beyond the accounting entries to the underlying activities and operations that give rise to them.

-

Other Related Services

We make it a point to keep our clients abreast of the developments and updates relating to the growing complexities in the accounting world. We offer seminars and trainings on audit- and tax-related matters, such as updates on Accounting Standards, new pronouncements and Bureau of Internal Revenue (BIR) issuances, as well as other developments that affect our clients’ businesses.

-

Tax advisory

With our knowledge of tax laws and audit procedures, we help safeguard the substantive and procedural rights of taxpayers and prevent unwarranted assessments.

-

Tax compliance

We aim to minimize the impact of taxation, enabling you to maximize your potential savings and to expand your business.

-

Corporate services

For clients that want to do business in the Philippines, we assist in determining the appropriate and tax-efficient operating business or investment vehicle and structure to address the objectives of the investor, as well as related incorporation issues.

-

Tax education and advocacy

Our advocacy work focuses on clarifying the interpretation of laws and regulations, suggesting measures to increasingly ease tax compliance, and protecting taxpayer’s rights.

-

Business risk services

Our business risk services cover a wide range of solutions that assist you in identifying, addressing and monitoring risks in your business. Such solutions include external quality assessments of your Internal Audit activities' conformance with standards as well as evaluating its readiness for such an external assessment.

-

Business consulting services

Our business consulting services are aimed at addressing concerns in your operations, processes and systems. Using our extensive knowledge of various industries, we can take a close look at your business processes as we create solutions that can help you mitigate risks to meet your objectives, promote efficiency, and beef up controls.

-

Transaction services

Transaction advisory includes all of our services specifically directed at assisting in investment, mergers and acquisitions, and financing transactions between and among businesses, lenders and governments. Such services include, among others, due diligence reviews, project feasibility studies, financial modelling, model audits and valuation.

-

Forensic advisory

Our forensic advisory services include assessing your vulnerability to fraud and identifying fraud risk factors, and recommending practical solutions to eliminate the gaps. We also provide investigative services to detect and quantify fraud and corruption and to trace assets and data that may have been lost in a fraud event.

-

Cyber advisory

Our focus is to help you identify and manage the cyber risks you might be facing within your organization. Our team can provide detailed, actionable insight that incorporates industry best practices and standards to strengthen your cybersecurity position and help you make informed decisions.

-

ProActive Hotline

Providing support in preventing and detecting fraud by creating a safe and secure whistleblowing system to promote integrity and honesty in the organisation.

-

Accounting services

At P&A Grant Thornton, we handle accounting services for several companies from a wide range of industries. Our approach is highly flexible. You may opt to outsource all your accounting functions, or pass on to us choice activities.

-

Staff augmentation services

We offer Staff Augmentation services where our staff, under the direction and supervision of the company’s officers, perform accounting and accounting-related work.

-

Payroll Processing

Payroll processing services are provided by P&A Grant Thornton Outsourcing Inc. More and more companies are beginning to realize the benefits of outsourcing their noncore activities, and the first to be outsourced is usually the payroll function. Payroll is easy to carve out from the rest of the business since it is usually independent of the other activities or functions within the Accounting Department.

-

Our values

Grant Thornton prides itself on being a values-driven organisation and we have more than 38,500 people in over 130 countries who are passionately committed to these values.

-

Global culture

Our people tell us that our global culture is one of the biggest attractions of a career with Grant Thornton.

-

Learning & development

At Grant Thornton we believe learning and development opportunities allow you to perform at your best every day. And when you are at your best, we are the best at serving our clients

-

Global talent mobility

One of the biggest attractions of a career with Grant Thornton is the opportunity to work on cross-border projects all over the world.

-

Diversity

Diversity helps us meet the demands of a changing world. We value the fact that our people come from all walks of life and that this diversity of experience and perspective makes our organisation stronger as a result.

-

In the community

Many Grant Thornton member firms provide a range of inspirational and generous services to the communities they serve.

-

Fresh Graduates

Fresh Graduates

-

Students

Whether you are starting your career as a graduate or school leaver, P&A Grant Thornton can give you a flying start. We are ambitious. Take the fact that we’re the world’s fastest-growing global accountancy organisation. For our people, that means access to a global organisation and the chance to collaborate with more than 40,000 colleagues around the world. And potentially work in different countries and experience other cultures.

-

Experienced hires

P&A Grant Thornton offers something you can't find anywhere else. This is the opportunity to develop your ideas and thinking while having your efforts recognised from day one. We value the skills and knowledge you bring to Grant Thornton as an experienced professional and look forward to supporting you as you grow you career with our organisation.

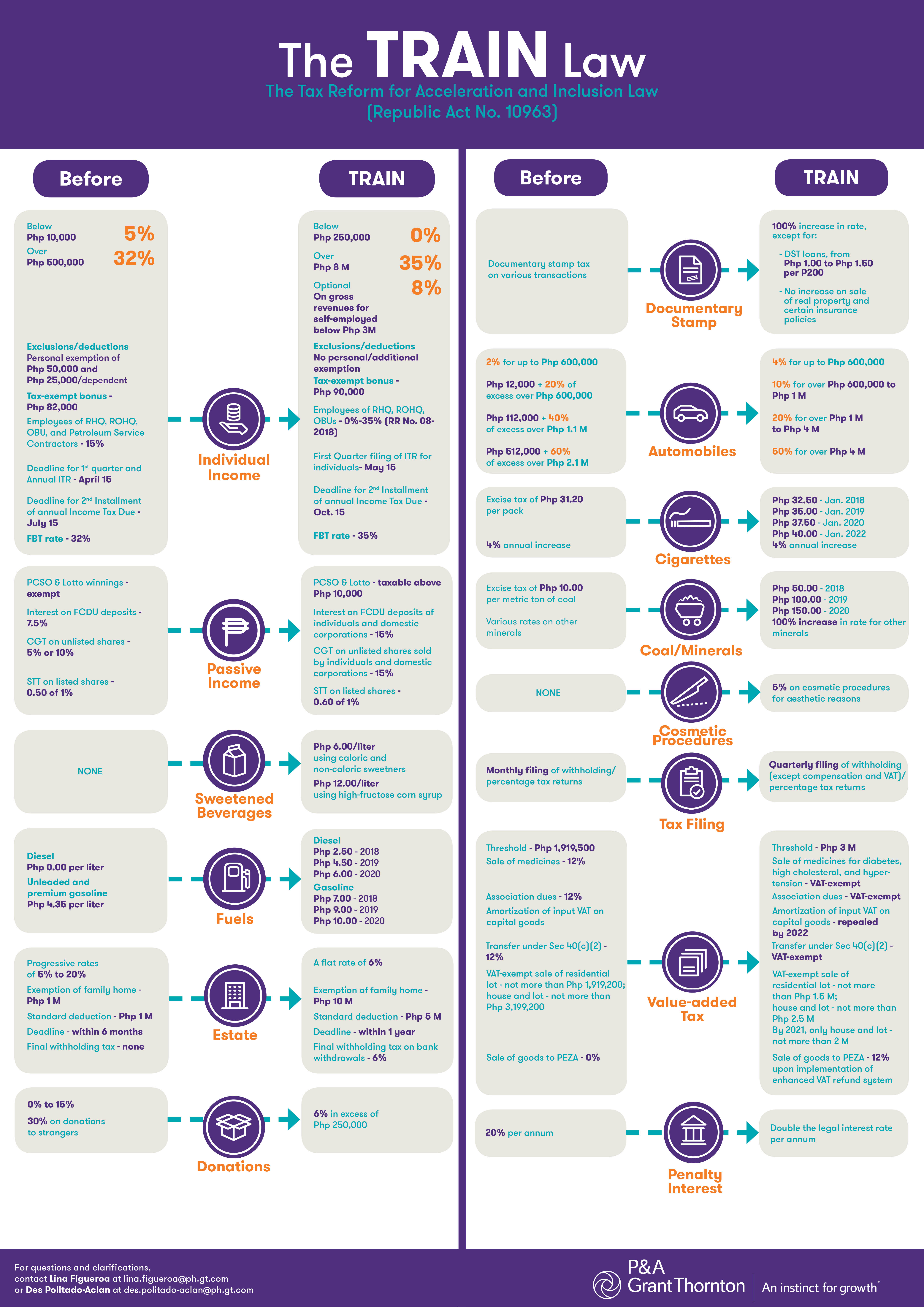

Welcoming 2018 with TRAIN

02 Jan 2018THE TRAIN stayed on track and reached its destination in time to take effect yesterday, Jan. 1, as targeted.

Republic Act (RA) 10963, otherwise known as the Tax Reform for Acceleration and Inclusion (TRAIN) was signed by the President on Dec. 19, 2017, while vetoing certain provisions. As provided in the RA, the new law takes effect on Jan. 1, following its complete publication in the Official Gazette. It was published on Dec. 27.

Hence, on the next payday this January, many employees will take home their salaries in full, without tax deduction. Pursuant to the revised withholding tax table issued by the Bureau of Internal Revenue (BIR) through Revenue Memorandum Circular (RMC) No. 105-2017, there is no withholding for those receiving P685 daily wage; P4,808 weekly wage; P10,417 semi-monthly wages; or P20,833 monthly wage. We must credit the BIR for preparing the Table well in advance even while the legislation has not yet been approved. You can access the withholding tax table through this link.

The Department of Energy (DoE) has likewise issued clarifications that, although the higher petroleum excise taxes take effect on Jan. 1, the higher taxes do not apply to old stocks which have been imported or released from the refineries earlier and excise taxes for which has already been paid at the old rates.

Several provisions of the TRAIN will require further interpretation which should be addressed in the implementing regulations to be issued by the BIR.

Among others, the veto message of the President opted to prioritize fairness and declared that employees of RHOs, ROHQs, OBUs and petroleum service contractors should follow the regular rates applicable to other individuals. However, the remaining provisions after the veto still suggest that employees of existing RHQs, ROHQs, OBUs and petroleum service contractors can continue to enjoy the 15% preferential income tax rate.

The new provisions for VAT zero-rating of services to the Philippine Economic Zone Authority (PEZA) and TIEZA entities were likewise vetoed. However, I note that, even prior to TRAIN and without these new provisions, there is a legal basis for the zero-rating of the services under the PEZA law (RA 7916), which was not repealed.

We will eagerly wait on how the BIR will interpret the Presidential veto on these provisions.

I am sharing the highlights of the TRAIN as prepared by our firm, P&A Grant Thornton. This summary is based on our interpretation of the provisions of the law. Please note that some of these may change, particularly on the gray areas discussed above, depending on the implementing regulations that will be issued by the BIR.

Lina P. Figueroa is a principal with the Tax Advisory and Compliance division of P&A Grant Thornton.

As published in BusinessWorld, dated 02 January 2018